Three small-caps generating income

Clime Investment Management

Clime Investment Management

Investors can be drawn to small-caps because the segment often houses companies with unappreciated growth prospects. The challenge of course is to avoid the numerous failures and investment speculation from creeping into portfolios.

To better participate in this market and provide more choice, our funds partner Clime Investment Management launched the Clime Smaller Companies Fund in May this of year. For StockInValue members this translates to more frequent and dedicated coverage of small-caps.

Although capital returns are typically the focus at this end of the market, strong and consistent income remains a key objective for us. This report updates on three growing smaller companies that also provide healthy income returns, including Rural Funds Group (RFF), a REIT that owns prime Australian agricultural assets, HFA, parent of US-based fund of hedge funds manager Lighthouse, and Jumbo Interactive, an online retailer Australian lotteries. This diverse trio offers a blended yield of 6.8%, while each have strong respective balance sheets to support future growth.

Jumbo Interactive (JIN)

Note JIN went ex-dividend ($0.15 special) on Monday 24 July

After JIN's strong share price gains over the last 18 months (~200%) there could be some investors taking profits at this stage. Obviously big rallies inevitably exhaust value discounts and we’re conscious of this. However we think it’s a case of shares rapidly catching up to value as opposed to pure momentum. The stock remains interesting for the following reasons:

JIN occupies a very narrow channel in lottery ticket e-tailing, which faces potentially years of structural growth. About $4 billion of Tatts Lotto tickets are sold in Australia each year, with 13% sold online. The online share has doubled since 2012, and in some European countries such as Norway the online share is as high as 30%. There’s a saying, “a rising tide lifts all boats”, but another one is “competition is for losers”. Only two players in Australia are soaking up structural demand for online lottery tickets, JIN and Tatts, so we have high conviction in JIN’s growth prospects.

With lower future costs resulting from JIN’s international business exits and plateauing capex, JIN’s strong revenue growth should produce around $10 million per annum in free cash flow in the next couple of years. Deducting JIN’s $30 million cash from its $138 million market cap, shares are trading on a forward multiple 11.4 times (on an ex-cash basis). For context, the market’s average price earnings ratio is about 15 times. JIN is no longer extremely cheap but it’s certainly not expensive.

The company has recently positioned itself as the online partner to Australia’s charity lotteries, a $1 billion industry that still uses rudimentary technology. JIN’s platform can handle marketing and distribution on behalf of charities, saving them costs, while maintaining JIN's own healthy margins. The charities business launched in mid-2015 and is still new, but it could contribute materially to revenues in the future. It appears to be a free option at JIN’s current share price.

All of this begs the question, why was the business trading at such a large discount in the past? Two reasons, in our view, are (1) JIN’s short-term state based licenses gave the impression that JIN was vulnerable to Tatts suddenly ending the relationship, and (2) JIN's venture into Europe and Mexico failed to generate revenues and resulted in significant sunk costs.

In May Tatts JIN announced a new agreement with Tatts, with all short-term state-based reseller arrangements extended for five years, conditional on any competitor’s stake in JIN being limited to 10 per cent. Tatts itself took a 15 per cent stake in the company via the issue of new shares, and a Tatts representative was invited to join JIN’s board.

JIN’s failure internationally reflects the difficulty in establishing a database. The flip-side is that its domestic database of 2 million qualified leads (including credit card details and 18+ age verification) is very valuable indeed. This was the basis for international lottery wagering provider Lottoland’s brief appearance on JIN’s register this year.

In its May 30 guidance JIN announced it will adopt an 85% payout ratio. On our numbers this translates to a fully franked yield of 5% (equivalent to a grossed up yield of 7%).

HFA

HFA’s controlled entity Lighthouse Partners is a Fund of Hedge Funds (FoHF) with a difference. One of the key issues in this area is “style drift”, which is when a hedge fund deviates from its mandate and invests outside its area of expertise.

Lighthouse manages multi-strategy and strategy-focused funds via its proprietary ‘managed accounts’ program, which distinguishes Lighthouse from traditional FoHFs. Lighthouse collects real-time data on portfolios to track managers and assess adherence to mandates, providing more transparency, protection and stronger investment governance. This has contributed to Lighthouse’s long term record of stable returns at very low volatility, its key attraction.

HFA had a dormant couple of years between 2012 and 2014 as the company concentrated on paying down debts to strengthen its balance sheet. It now has a strong, A$30 million net cash position from which it can fund dividends or growth investments. The share price has responded in-kind, but even now at $2.43 it trades on attractive 10% forward yield.

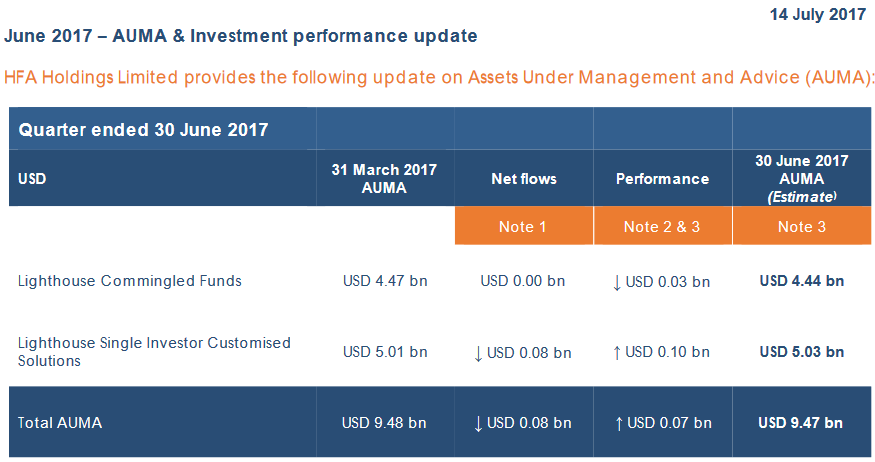

In last week’s June quarter update HFA reported stable Assets Under Management and Advice (AUMA) at US$9.47 billion. The ‘Customised’ business has been growing well and management appear confident of further mandate wins in near to mid-term, adding to the 11 accounts it holds currently.

We remain positive about the stock, and happy to collect healthy income returns absent of any material share price movements.

Rural Funds

Australia is known globally as a clean growing region, and a beneficiary of this is agricultural landlord Rural Funds Group (ASX: RFF). RFF is a real estate investment trust (REIT) with a market capitalisation of just over $500m. It owns a diversified portfolio of high quality Australian agricultural assets that are leased to experienced agricultural operators (RFF’s tenants).

Revenues are derived from long-term lease rentals across five sub sectors including poultry infrastructure, tree nut orchards (almonds and macadamias), vineyards, cattle assets and cotton, and agricultural risk (seasonal harvest variation) is essentially borne by the grower.

Importantly, post the recent capital raising, RFF’s gearing ratio has receded to a comfortable 29.5% while its payout ratio of 76% allows for reasonable reinvestment to occur. This approach is consistent with RFF’s objective to provide investors with balanced growth and income.

Given the Group’s experienced management team, sound future prospects and solid (and growing) yield of around 5.3% per cent, we believe RFF presents a solid investment opportunity over a medium investment horizon.

Contributed by Jonathan Wilson, Analyst at Clime Asset Management.

Clime owns shares in JIN, HFA, and RFF.

Never miss an update

Enjoy this wire? Hit the ‘like’ button to let us know.

Stay up to date with my current content by

following me below and you’ll be notified every time I post a wire

The Clime Group is a respected and independent Australian Financial Services Company, which seeks to deliver excellent service and strong risk-adjusted total returns, closely aligned with the objectives of our clients.

3 topics

2 stocks mentioned

Clime Investment Management

Funds Management & Stock Research

Clime Investment Management

The Clime Group is a respected and independent Australian Financial Services Company, which seeks to deliver excellent service and strong risk-adjusted total returns, closely aligned with the objectives of our clients.

Expertise

Clime Investment Management

Funds Management & Stock Research

Clime Investment Management

The Clime Group is a respected and independent Australian Financial Services Company, which seeks to deliver excellent service and strong risk-adjusted total returns, closely aligned with the objectives of our clients.

Expertise

Comments

Comments

Sign In or Join Free to comment

most popular

Investment Theme

If 24 LICs ran the Melbourne Cup, which ones would we back?

Affluence Funds Management