To end the health crisis, we may begin a debt crisis

Even before COVID-19 changed the world, Tony Cousins of multi-asset and global equities manager Pyrford International was feeling pretty nervous heading into 2020.

"We had for a while believed that the strong performance in 2019 meant that increased uncertainty could lead to weakness in equity markets. Markets are most vulnerable when valuations are expensive and markets have been in expensive territory for several years."

To be precise, the BMO Global Asset Management-owned firm had only 35% exposure to equities within their Global Absolute Return strategy. Tony's ethos is that the best path to sustainable returns with low absolute volatility comes from investing in a strict combination of value and quality. Not one or the other, it has to be both.

The recent volatility provides both good news and bad news for Tony:

- The good - Value has finally emerged, prompting Pyrford to make substantial changes to its asset allocation

- The bad - Fiscal discipline has been "thrown out the window", and there is a risk that if this health crisis is not brought under control quickly, it will lead to unmanageable financial contagion that will roil credit markets

Read on for Tony's views and portfolio positioning.

Caption: Tony Cousins, Chief Investment Officer and Chief Executive Officer, Pyrford International

What is your base, bear and bull case scenario for the global economy over the next 6-12 months?

It's difficult to produce scenario analysis over such a short timeframe given how rapidly the situation is evolving. That said, the current pandemic and the authorities response to it is clearly going to lead to a sharp contraction in output. Effectively shutting down a large part of the economy is going to lead to a demand shock which will clearly be deflationary. The length of this recession will be determined by how long the “lockdown” imposed by authorities lasts.

We have seen some extraordinarily large measures by developed market governments to try and keep businesses afloat and money in the hands of consumers. Fiscal discipline has been thrown out of the window and rightly so. Now is not the time to be concerned about the inevitable rise in government debt. That will need to be dealt with at a later date but for now central banks will ensure that the money is raised through sovereign bond issuance which they can help absorb in the quantitative easing programs.

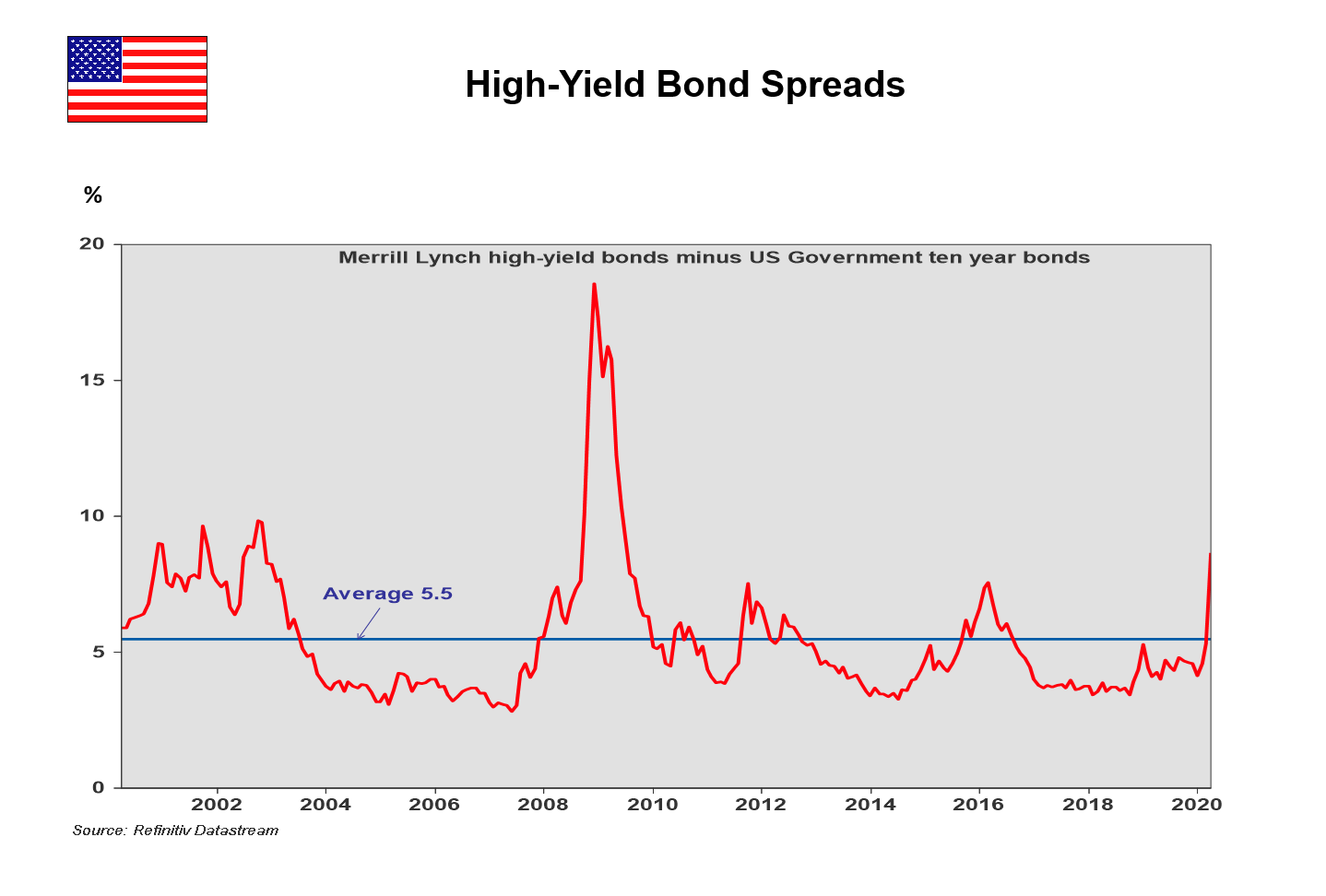

If the lockdown is extended for protracted time period, the danger is that this demand shock will mutate into a financial crisis as companies run out of cash and are unable to raise new capital. We have particular concerns about the US corporate credit market which has exploded in size over the last decade in the era of quantitative easing.

Central banks have printed US$15 trillion dollars of new money and if money is cheap and plentiful, companies will borrow it. Corporate debt to GDP is at an all-time high in the US in part driven by the explosion in share buyback programs. One particular pinch point is that around 50% of US investment-grade bonds are rated BBB, one notch above junk. It would not take much economic dislocation for the businesses of these issuers to be affected sufficiently to cause rating downgrades by S&P or Moody's.

If these bonds cease to be investment grade, many holders simply are not permitted to own them anymore. Selling pressure will build in a market where market-making capacity has shrunk by 85% over the last decade due to the imposition of the Volker rule limiting proprietary capital.

Looking at the most optimistic case, if the pandemic is contained and new cases start falling allowing lockdown to be lifted before there is contagion into the financial economy, there is scope for a swift recovery. Unfortunately the probability of this outturn is not high.

How do you think this will play out across the major asset classes?

Equities have obviously fallen sharply. This is because they were simply too expensive. When markets are as expensive as they have been, they are always very vulnerable to shocks and this was no exception. Many markets are now relatively inexpensive but their ability to recover will be dependent on how long the lockdown lasts as outlined above.

The one exception remains the US equity market which remains overvalued. It had risen to far more overvalued levels than other markets so simply had and still has further to fall.

Sovereign bonds remain very overvalued with historically low yields which simply preclude an adequate rate of return for those who buy at these levels. That said, central banks simply will not allow yields to rise significantly in the foreseeable future. They will simply print money to prevent this from happening.

The biggest cause for concern will be in credit markets where there is a risk of them “seizing up” due to lack of liquidity. Credit and junk bond spreads have blown out to reflect this but probably not enough. Property has to be vulnerable, especially in counties where residential real estate is already highly unaffordable (e.g. Australia, Canada, UK).

How are you positioning your portfolio amid short-term uncertainty?

We went into this crisis with equity weightings at the same very low levels as we held in 2007/8 based on our analysis that equities were very overvalued.

In our Global Absolute Return strategy, our equity weighting was 35% in the AUD offering and as markets have fallen through our predetermined valuation points, we have added equities in two tranches. The first was an increase by 5% to 40% and the recent second tranche was by 10% to 50%. The asset allocation of the portfolio is now 50% in equities, 47% high-quality sovereign bonds and 3% cash.

The cash weighting may appear low but the sovereign bonds are very short duration (less than 2 years) and permit the portfolio to gain greater exposure to non-A$ currencies. If equities fall further from this level, we will increase the equity weighting further.

The key characteristics of the equities we own are higher than market dividend yield, significantly higher than market return on equity and much lower than market debt to equity. It is extremely important that at these times of economic and financial market stress, investors avoid stocks with stretched balance sheets.

Access a global multi-asset investment strategy

Pyrford seeks to provide a stable stream of real returns over the long term with low absolute volatility and significant downside protection. To find out more, click the 'CONTACT' button below.

Disclaimer

BMO Global Asset Management (Asia) Limited (ARBN 618067959), Pyrford International Ltd (ARBN 165504414) and LGM Investments Limited (ABN 19 381 443 479) are exempt from the requirement to hold an Australian financial services licence under the Corporations Act in respect of the financial services each provides to "wholesale" investors (as defined in the Corporations Act) in Australia. Pyrford International Ltd and LGM Investments Limited are regulated by the Financial Conduct Authority under UK laws, and BMO Global Asset Management (Asia) Limited is regulated by the Securities and Futures Commission under Hong Kong laws, which differ from Australian laws.

BMO Global Asset Management (Asia) Ltd ARBN 618067959 is exempt from the requirement to hold an Australian financial services license under the Corporations Act in respect of the financial services it provides to wholesale investors (as defined in the Corporations Act) in Australia. BMO Global Asset Management (Asia) Ltd is incorporated in Hong Kong and authorised and regulated by the Hong Kong Securities and Futures Commission under Hong Kong laws, which differ from Australian laws.

Never miss an update

Enjoy this wire? Hit the ‘like’ button to let us know.

Stay up to date with my current content by

following me below and you’ll be notified every time I post a wire

Livewire Exclusive brings you exclusive content from a wide range of leading fund managers and investment professionals.

........

Disclaimer: This article is for informational purposes only and should not be considered financial advice. The article may contain the views or opinions of third party contributors to Livewire Markets. These contributors have not considered your objectives, financial situation, or needs. The information in this article should not be relied upon as a substitute for personal financial advice. Livewire Markets recommends that you seek independent advice before you apply for any financial product or service. Livewire Markets is exempt from requiring an AFSL under APRA Regulatory Guide 36, section 66.

4 topics

Livewire Markets

Livewire Exclusive brings you exclusive content from a wide range of leading fund managers and investment professionals.

Expertise

Livewire Markets

Livewire Exclusive brings you exclusive content from a wide range of leading fund managers and investment professionals.

Expertise

Comments

Comments

Sign In or Join Free to comment

most popular

Equities

Consequences of capital flows can't be ignored

ClearBridge Investments

Property

The property market’s next big moment is already underway

Livewire Markets