Unemployment ticks up, Perpetual rewards patience! (BIN, PPT, ILU)

The market traded up to our ~7200 target this morning on February index option expiry, we often see a squeeze into expiry which corresponds with a short term top in the market. For now, it playing out on que at the index level at least. The buying early was underpinned by an uptick in the unemployment rate which printed 5.3% versus the 5.2% expected which is a positive read for further rate cuts. The AUD was sold and the market bidded up as a consequence.

Data

Source: Bloomberg

While the headline was soft, the actual composition wasn’t. A higher participation rate implies strength, so does the number of full-time jobs being added v part-times, overall, not such a weak print in our opinion. At the sector level today, the IT names remained under pressure, Wisetech (WTC) down another -11.78% clearly weighed however as we wrote this morning, it simply feels like the tech sector more generally is due a pause, similar to the overall market.

On the reporting front today, we had a number of portfolio holdings out with results, with some mixed outcomes. The Platinum Portfolio holds Bingo (BIN) -0.94%, Boral (BLD) +0.21% & NRW Holdings (NWH) -1.66%. while the Income Portfolio holds Perpetual (PPT) +11.15%. More on these below.

Reporting schedule available here: CLICK HERE

Overall, the ASX 200 rose 17pts / +0.25% today to close at 7162, another record high. Dow Futures are trading down -50pts/-0.18%

ASX 200 Chart

ASX 200 Chart

CATCHING MY EYE

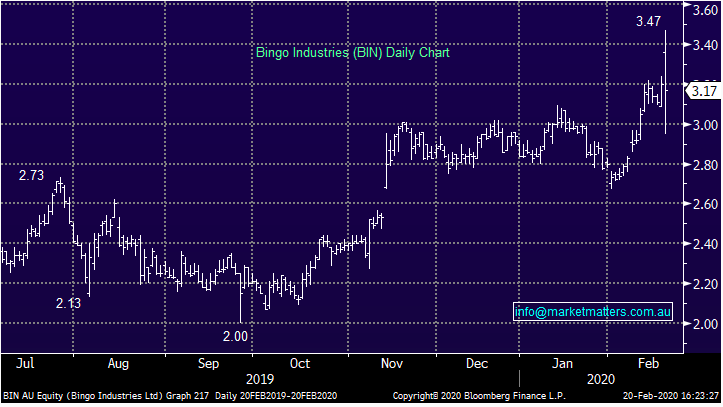

Bingo (BIN) -0.94%: A volatile session for the waste management business after delivering 1H20 numbers this am. Underlying EBITDA for the period of $82m was a beat and more importantly, margins super strong at 33%. Interim DPS of 2.2c ahead of forecast and the runway for the next few years looks strong. They reiterated FY20 underlying EBITDA guidance of $159 to $164m. Outlook statement as expected (previously guided to): “Headwinds in multi-dwelling residential construction are expected to continue in FY20 with improvement forecast for CY21. Infrastructure and the broader construction pipeline remain robust together with opportunities for further growth in Commercial & Industrial (C&I).”

While the stock is clearly not cheap, and there remains a decent dispersion in the mkt about their outlook (shown through volatility in SP today) we like the medium-term story of BIN.

Bingo (BIN) Chart

Perpetual (PPT) +11.15%:A strong performer for the income portfolio today after a good 1H20 result. Underlying NPAT of $56.1m beat forecasts of $55m while they reduced their dividend to 105cps fully franked as they tweak their focus on growth. That’s what got the mkt excited today which went with a bullish note out from Bells, they upgraded their PT from $41 to $51.20 with a buy rec. We continue to like PPT and view it as a reasonably priced mix of income and growth.

Perpetual (PPT) Chart

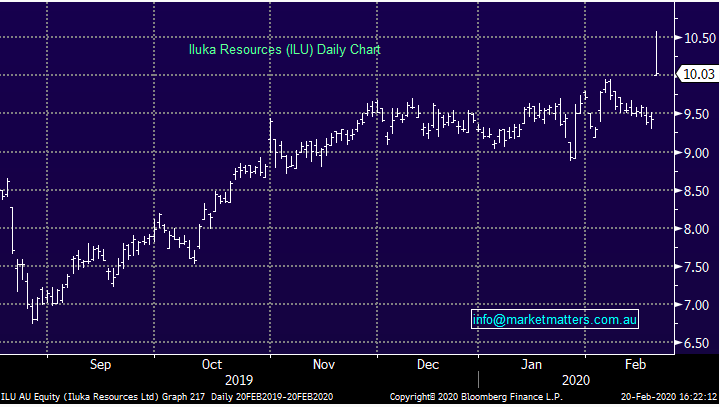

Iluka (ILU) +6.36%: rallied on their half year despite numbers looking just a tickle below consensus at the full year. Sales were down around 8% on the year as prices slid, while EBITDA rose 15%. Disruptions at their Sierra rutile facility have also been suspended over the past few days because of some community unrest however the company expects operations to come back online in the coming days. The big reason the stock rallied wasn’t for their mineral sands, it came from the company’s plan to demerge Royalty Co which would house the payments from BHP on a royalty over Mining Area C. There has been speculation around what Iluka would do with these payments, which generated $85m of EBITDA in 2019.

Under these plans, Iluka would retain a minority stake in Royalty Co who would also look at purchasing royalties over other mining operations.

Iluka (ILU) Chart

Elsewhere in reporting:

NRW Holdings (NWH) -1.66%: Messy given acquisition during the period however they did revenue of $808.7m (good) with comparative EBITDA of $94.6m, up strongly on the period. They had previously guided to $1.5bn revenue for the year, however they now say this will be $2b, although the market was already there - importantly, most already contracted. We like NWH, along with our other exposure in the space being Emeco (EHL), which has enjoyed a good run.

Whitehaven Coal (WHC) -5.51%: Not a lot to get excited about here, 1H20 NPAT of $27.4m vs expectations of 45.2m on revenue of $885.1m vs expectations for $915.1m, adjusted EBITDA of $177.3m vs expectations for $204.5m. Expect downgrades although weakness shouldn’t come as a huge surprise given coal price trends.

Santos (STO) -1.22%: From an operational and financial perspective, all going very well. Plenty of exploration and development activity to drive production to >120MMboe in 2025. Only clouds are oil prices near term, and weak domestic gas and Asian LNG spot market. Volume growth however should offset, and dramatic reduction in cost base now over 4 years means Santos can make decent profits. We like into current weakness

Sandfire (SFR) +1.36%: 1H20 results seemed lighter on that I thought at first glance. Haven’t had a chance to dig much here although FY20 guidance maintained. Remains on track to make a decision to mine T3 development project by mid calendar year 2020

…. we’ll cover off on a few more results tomorrow given a quieter day on the desk expected (maybe!). Snowed today.

Broker Moves:

· OZ Minerals Rated New Accumulate at Ord Minnett; PT A$11.30

· Charter Hall Group Cut to Neutral at UBS; PT A$13.80

· Vocus Cut to Neutral at UBS; PT A$3.85

· Vocus Cut to Sell at Morningstar

· Vocus Raised to Buy at Jefferies; PT A$4.35

· Domino’s Pizza Enterprises Cut to Sell at UBS; PT A$52.50

· Domino’s Pizza Enterprises Cut to Sell at Morningstar

· Domino’s Pizza Enterprises Raised to Overweight at JPMorgan

· Domino’s Pizza Enterprises Cut to Underperform at Credit Suisse

· WiseTech Cut to Neutral at Citi; PT A$22.60

· WiseTech Cut to Neutral at Evans & Partners Pty Ltd; PT A$24.52

· WiseTech Cut to Sell at Bell Potter; PT A$20

· Western Areas Raised to Buy at Bell Potter; PT A$2.96

· Wesfarmers Raised to Outperform at Macquarie; PT A$52.60

· SmartGroup Raised to Outperform at Macquarie; PT A$7.46

· St Barbara Raised to Neutral at Macquarie; PT A$2.70

· New Hope Raised to Outperform at Macquarie; PT A$2

· Lovisa Raised to Buy at Canaccord; PT A$12.60

· Stockland Raised to Hold at Jefferies; PT A$4.85

· Coles Group Raised to Buy at Goldman; PT A$18.10

· Sonic Healthcare Raised to Outperform at Credit Suisse

· Oil Search Raised to Neutral at Credit Suisse; PT A$6

· Orica Raised to Buy at Jefferies; PT A$25

· Fletcher Building Raised to Buy at Deutsche Bank; PT NZ$5.79

· Fortescue Cut to Underperform at RBC; PT A$8.75

· Avita Medical Cut to Speculative Hold at Bell Potter

· Sims Cut to Neutral at Credit Suisse; PT A$10.60

Stay on top of Reporting Season with live updates

Market Matters publishes daily market reports and sends SMS alerts when we transact on our portfolio. To get our latest market views and hear when we take new positions, trial Market Matters for 14 days at no cost by clicking the 'CONTACT' button bellow.

Never miss an update

Enjoy this wire? Hit the ‘like’ button to let us know.

Stay up to date with my current content by

following me below and you’ll be notified every time I post a wire

James is Director & Lead Portfolio Manager at Market Partners - a collective of highly experienced investment professionals, operating independently, managing discretionary portfolios for wholesale investors.

James is also Portfolio Manager & primary author at Market Matters, a digital advice & investment platform with over 2500 members that offers real market intel & six portfolios open for investment.

........

Any advice provided is of a general nature only

1 topic

3 stocks mentioned

James is Director & Lead Portfolio Manager at Market Partners - a collective of highly experienced investment professionals, operating independently, managing discretionary portfolios for wholesale investors. James is also Portfolio Manager &...

Expertise

James is Director & Lead Portfolio Manager at Market Partners - a collective of highly experienced investment professionals, operating independently, managing discretionary portfolios for wholesale investors. James is also Portfolio Manager &...

Expertise

Comments

Comments

Sign In or Join Free to comment

most popular

Funds

The 5 best-performing super funds of the year

Livewire Markets

Equities

Buy Hold Sell: 5 ASX stayers built to go the distance

Livewire Markets