Uranium – the bull market has already started

Marcelo Lopez

L2 Capital Partners

Wouldn’t it be nice to find a market to invest in in which the demand has been increasing constantly, supply is being cut and the cost of production is pretty much twice the current price (meaning, the price has to go up)? Well, look no further: I believe the uranium space provides us with such a combination today!

It is one of the very few opportunities at the moment in which the risk x return relationship is quite enticing. 2018 was a bad year for most investments, with stocks, bonds, most commodities (copper, oil, iron ore, etc), real estate and cryptocurrencies down – but uranium went up by almost 40% in the spot market! The bull market has arrived and, because the market cap of most companies in the sector is too small, I believe the returns could be astronomical going forward.

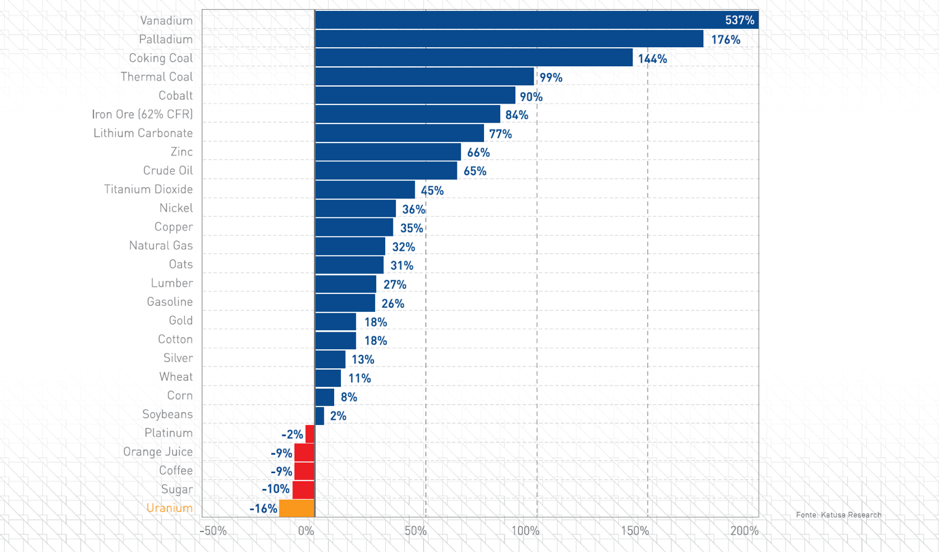

The biggest trigger for 2019 is the decision on Section 232, and it should clear the path for a stronger recovery in the uranium space in the second half of 2019. Few people are paying attention to the developments in the sector and uranium is the less loved, perhaps the most hated, commodity of them all (see chart below with returns over the past 3 years). This makes uranium the perfect target for contrarians.

I intend to write more about uranium in my next posts, where I will lay my bull thesis on the metal, but I would like to dedicate this article to Section 232 – an issue that is not well covered and could be the most important event for 2019 in the sector.

Ur-Energy and Energy Fuels filed the Section 232 petition in January 2018 on the basis of national security and the Department of Commerce (DoC) accepted this petition in July, when the investigations started. The DoC has 270 days to come to a recommendation and, after that, President Trump has up to 90 days to make a decision.

According to the press release, Energy Fuels and Ur-Energy have filed a Section 232 Petition requesting “(1) the Department of Commerce to investigate the effects of uranium imports on U.S. national security and (2) the President to use his authority to adjust imports to ensure the long-term viability of the U.S. uranium mining industry”. Basically, what the petitioners are claiming they want is to avoid dependence of Russia and Russian allies for the supply of uranium and for the president to throw out a lifeline for the miners.

Just to give an idea of the situation in the US today, its mines produce the same amount it did back in 1949! The US is the biggest market for uranium in the world and it consumes 50 million pounds per year, about ¼ of the world’s demand, whilst it produces less than 2 million pounds per year!

Russia and Kazakhstan supply circa 38% of the US’s demand for uranium. This lack of internal production could be a threat, as most of the uranium imported into the US comes from not-so-reliable countries, like Russia, Kazakhstan and Africa. Countries that are friendly to the US are Canada and Australia and they supply just over 50% of the US needs.

Rick Perry, former governor of Texas and current Secretary of Energy of the US, is very fond of nuclear energy. As around 20% of the US base line energy comes from nuclear power, Mr. Perry, together with president Trump, wants to secure uranium supply to the US.

It is becoming increasingly more difficult to get the licenses and approvals to mine uranium in developed countries, like the US, Canada and Australia and a proper project could take up to 15 years to come out of paper and into production– not to mention that, obviously, the project would need a much higher price to be incentivised. This is something that needs to be addressed by the new administration, which, as said before, is fond of nuclear energy.

Many people speculate that Trump is the tariff man and a tariff on imports of uranium is what might happen. If that is the case and Trump really imposes a tariff on the imports of uranium, the intended objectives of the two Section 232 petitioners would not be fully achieved. There might be a system with two different prices (like in the oil market – WTI and Brent), but it will not help the US gain the independence (or reduce its dependence) on imported uranium.

The utilities are not happy and are fighting the mining companies back. Of course, as they want lower prices and are only looking at the near future. After the Section 232 petition, utilities, to put some pressure back on the miners, decided not to contract (long term purchase contracts) any uranium until a decision was made by the DoC or president Trump. Something that they (mis)calculated would take a few weeks, turned into a more than a year (and counting) problem.

We could speculate what the decision from president Trump would be – but whatever the decision, it will clear the way for the purchase of uranium by the utilities, and we could see a fast rise in price. By the time of the decision, the utilities would have not contracted uranium for 1.5 years, which means their inventories will be much lower. Besides, the purchase of uranium is a negotiation that lasts from a couple of months up to half a year. As the average cost of production is way higher than the current price, we can expect a jump in the reported price. Once the utilities start contracting again, the current prices will prove themselves unsustainable.

The long-term contracts comprise most of the uranium trading and is where the real action takes place. Because utilities ceased to contract since the petition was filed, the 40% increase in the spot prices I mentioned could not have been realised in the long-term prices. As a matter of fact, the spread between both was driven to the lowest level in over 10 years.

One important point to notice is that the uranium cycle is not like the mineral coal and other commodities, which can be mined and delivered in a short period of time. Uranium takes in between 1.5 to 2 years to be mined, converted, enriched, assembled and delivered – so it is normal that utilities keep a large inventory. By the way, the current average inventory held by utilities is the lowest it has been in many decades.

On top of that, inventories are not so straight forward as they are in other commodities. Some of the inventory is held as strategic reserves (which are not meant to be sold), some is held as depleted tails (which would require a much higher uranium price to become mobile) and some are in different formats (U3O8, UF6, etc). According to UxC, there was last year something like 17-35 million pounds of uranium classified as a mobile inventory – this number, although impressive, is less than the deficit between production and demand for last year (this year the gap should widen even more).

Nuclear reactors are very expensive to build and, once in operation, fuel (uranium) is a very small component of their cost. Therefore, the risk of not having the fuel is way higher than the risk of overpaying for it. I would go as far as saying the price is almost irrelevant for utilities. What they need is the certainty that they will have the material at the time arranged and in the right specifications.

Many people are not paying attention to the sector and think it is in a clear decay. But I think differently. I believe this is the single best investment opportunity in the markets at the moment. It is one in which the relationship between risk and return is extremely favourable and should benefit the ones who did their homework and selected good companies that are poised to profit enormously when the bull market arrives. And, to appropriate a phrase from Rick Rule, it is not a case of IF the bull market arrives, but WHEN it arrives.

Never miss an update

Enjoy this wire? Hit the ‘like’ button to let us know.

Stay up to date with my current content by

following me below and you’ll be notified every time I post a wire

Marcelo Lopez, CFA, has been a portfolio manager at L2 Capital Partners since 2009 and focuses on opportunities globally. Prior to that he was a portfolio manager at Gartmore Investment Management in London.

4 topics

Marcelo Lopez

Portfolio Manager

L2 Capital Partners

Marcelo Lopez, CFA, has been a portfolio manager at L2 Capital Partners since 2009 and focuses on opportunities globally. Prior to that he was a portfolio manager at Gartmore Investment Management in London.

Expertise

Marcelo Lopez

Portfolio Manager

L2 Capital Partners

Marcelo Lopez, CFA, has been a portfolio manager at L2 Capital Partners since 2009 and focuses on opportunities globally. Prior to that he was a portfolio manager at Gartmore Investment Management in London.

Expertise

Comments

Comments

Sign In or Join Free to comment