Value Investing. Why cheap isn't cheerful

Designating low-PE stocks as value is a flawed concept. On average and over many years, low-PE stocks have generated much lower EPS growth, were more likely to cut their dividend, earned lower returns on capital and had higher financial leverage. There’s more trash than treasure in the bargain bin!

Asserting that a company trading on a lower PE multiple is better value than one trading on a higher multiple assumes away any reason why two businesses should be valued on different multiples. In fact, it assumes that every business should trade on the same earnings multiple. This is clearly flawed. The appropriate measure of value is the price relative to worth.

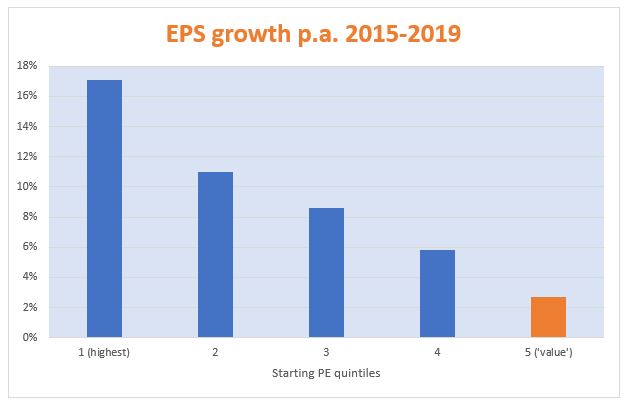

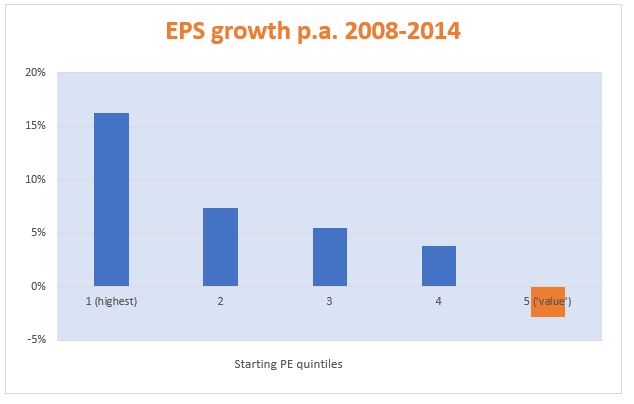

A value manager selecting stocks based on low-PE has, perhaps unwittingly, chosen companies that are lower quality, lower growth and higher risk. The analysis that follows is based on the largest 2,000 publicly traded companies globally by market cap in 2014 and excluded loss-makers. Let's see what you got for your money over the last five years, based on starting PE quintiles at the end of 2014, starting with growth. The value quintile delivered the poorest EPS growth outcome over the last five years.

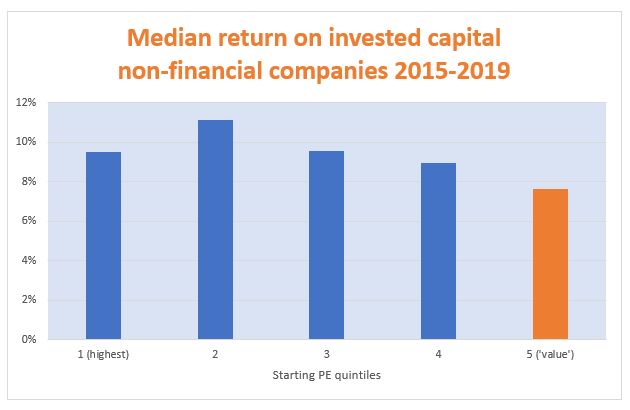

Let's now look at quality, as measured by return on invested capital (ROIC) for the non-financial companies. Growth and quality and intricately linked - the higher the ROIC the more free cash a business has to reinvest and drive future EPS growth. We can see that the value quintile earned the lowest ROIC of the five groups.

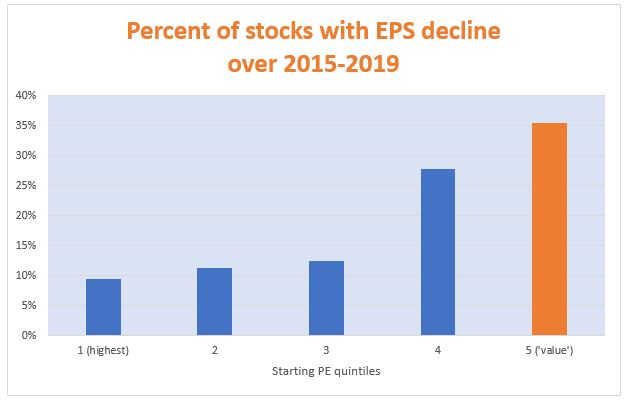

Let's turn to earnings risk. It's one thing to pay a low multiple of earnings, but if profits decline then you are perhaps paying a much higher multiple than you think based on prospective earnings.

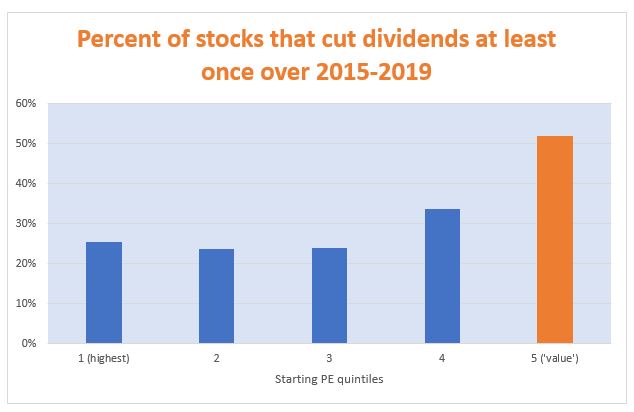

It should be no surprise that the value group was over-represented among

the dividend decliners.

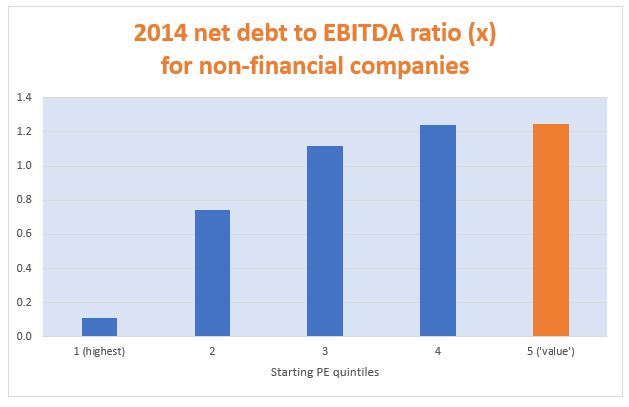

Turning to financial risk, we can see that the leverage ratio of non-financial companies was highest in the value cohorts.

Is it possible that we have chosen a five-year period that simply disadvantages low-PE businesses ? No. In fact, if use PEs at the end of 2007 (pre-GFC) and look at performance over the subsequent seven years, the differences are even starker.

The central flaw in the notion of value stocks or value investing is that it expresses value in terms of a PE multiple relative to an average. Whether a company is good value or not is, rather, a function of its share price relative to its worth. Companies differ in their growth prospects and their risk characteristics, and these differences should be reflected in their PE ratios. Choosing stocks based on a PE discount relative to a market average biases one's portfolio to lower growth, lower quality and higher risk businesses.

Never miss an update

Enjoy this wire? Hit the ‘like’ button to let us know.

Stay up to date with my current content by

following me below and you’ll be notified every time I post a wire

Stephen has been investing in global markets for over 30 years, making him one of Australia’s most experienced international investors.

He is the Founder and Chief Investment Officer of Aoris Investment Management, an independent, Sydney-based firm dedicated to a single strategy: a highly selective global equity portfolio.

Since its inception in March 2018 through to the end of April 2025, the Aoris strategy has ranked in the top 5% over 3 years, 5 years, and since inception, relative to a broad peer group of international equity funds (Morningstar). The firm currently manages just under $2 billion in assets.

Prior to founding Aoris in 2017, Stephen was Head of International Equities at Evans & Partners.

3 topics

Stephen has been investing in global markets for over 30 years, making him one of Australia’s most experienced international investors. He is the Founder and Chief Investment Officer of Aoris Investment Management, an independent, Sydney-based...

Expertise

Stephen has been investing in global markets for over 30 years, making him one of Australia’s most experienced international investors. He is the Founder and Chief Investment Officer of Aoris Investment Management, an independent, Sydney-based...

Expertise

Comments

Comments

Sign In or Join Free to comment