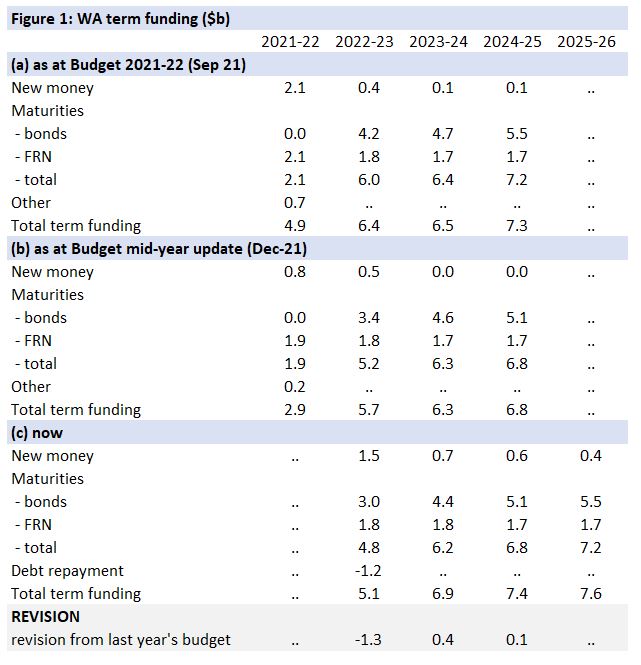

WA has downgraded its debt issuance in 2022-23 (ie, FY23) by a large $1.3bn (or 20%) from its September 2021 budget estimate of $6.4bn and by $0.6bn from its December estimate (see the table below). Like NSW, which is pre-emptively repaying $11bn of debt, WA is actively repaying $1.2bn of its debt. Victoria also recently announced it is creating a NSW-style debt retirement fund to be funded by asset sales that will be used for repaying COVID debts. CCI forecasts other states to follow suit and focus on debt reduction as interest rates return to more normal levels.

State and territory budgets are improving across the country, but WA continues to outpace its peers by a margin, posting large and upgraded budget surpluses. WA has used the windfall from high commodity prices and a stronger-than-expected economy, as well as material delays to a very large infrastructure programme, to repay debt, reduce its borrowing, and fund more current spending.

The expected general government cash budget surplus for 2021-22 was upgraded by $2.1bn from $2.8bn to $4.9bn, while the small forecast deficit of $0.3bn for 2022-23 was revised up by $1.9bn to become a solid surplus of $1.6bn.

The more important non-financial sector cash budget – which incorporates WA’s large public corporations – also saw upgrades, with the forecast surplus in 2021-22 revised up by $2.6bn from $1.5bn to $4.2bn and the expected deficit in 2022-23 trimmed by $1.3bn from $2.5bn to $1.2bn. These are broadly in line with CCI’s bullish forecasts.

Following the release of the WA budget, WATC's revised issuance task revealed it had significantly reduced its FY23 task from its original estimate in September 2021 of $6.4bn to just $5.1bn (ie, $1.3bn or 20% lower) with the risk that FY23 issuance is cut further if WA's budget bottom-line continues to outperform expectations. In WA's case, most of the windfall reflects strong commodity markets, although there is the broader risk that all the states benefit from ongoing strength in consumer spending via upside surprises to the GST revenue paid by the Commonwealth.

The reduced issuance from WATC comes after a significant reduction in Victoria's funding task for FY23. TCV's latest update of $21.3bn represents a $4.5bn (or 17%) reduction from the original $25.8bn estimate published in May 2021 and compares with the $23.6bn updated estimate published in December 2021. WA also follows the NT’s equally impressive $0.8bn reduction in its issuance requirement for FY23.

Never miss an update

Enjoy this wire? Hit the 'like' button to let us know. Stay up to date with my content by hitting the 'follow' button below and you'll be notified every time I post a wire.

Not already a Livewire member? Sign up today to get free access to investment ideas and strategies from Australia’s leading investors.

Never miss an update

Enjoy this wire? Hit the ‘like’ button to let us know.

Stay up to date with my current content by

following me below and you’ll be notified every time I post a wire

Based in Sydney, Kieran Davies is Chief Macro Strategist at Coolabah Capital Investments, an asset manager with 40 executives and over $8 billion in fixed-income strategies. Kieran is responsible for macroeconomic research and investment strategy, contributing to the investment decisions of the firm. Kieran has long experience as a macroeconomist in both the private and public sectors. He has worked most recently as Chief Markets Economist for National Australia Bank and was previously Chief Economist, Australia and New Zealand, for Barclays Bank and ABN Amro Bank/RBS. Kieran also worked as Principal Adviser on the macroeconomy and budget policy in the Commonwealth Treasury and Director of Forecasting.

........

Investment Disclaimer

Past performance does not assure future returns. All investments carry risks, including that the value of investments may vary, future returns may differ from past returns, and that your capital is not guaranteed. This information has been prepared by Coolabah Capital Investments Pty Ltd (ACN 153 327 872). It is general information only and is not intended to provide you with financial advice. You should not rely on any information herein in making any investment decisions. To the extent permitted by law, no liability is accepted for any loss or damage as a result of any reliance on this information. The Product Disclosure Statement (PDS) for the funds should be considered before deciding whether to acquire or hold units in it. A PDS for these products can be obtained by visiting www.coolabahcapital.com. Neither Coolabah Capital Investments Pty Ltd, Equity Trustees Ltd (ACN 004 031 298) nor their respective shareholders, directors and associated businesses assume any liability to investors in connection with any investment in the funds, or guarantees the performance of any obligations to investors, the performance of the funds or any particular rate of return. The repayment of capital is not guaranteed. Investments in the funds are not deposits or liabilities of any of the above-mentioned parties, nor of any Authorised Deposit-taking Institution. The funds are subject to investment risks, which could include delays in repayment and/or loss of income and capital invested. Past performance is not an indicator of nor assures any future returns or risks. Coolabah Capital Investments (Retail) Pty Limited (CCIR) (ACN 153 555 867) is an authorised representative (#000414337) of Coolabah Capital Institutional Investments Pty Ltd (CCII) (AFSL 482238). Both CCIR and CCII are wholly owned subsidiaries of Coolabah Capital Investments Pty Ltd. Equity Trustees Ltd (AFSL 240975) is the Responsible Entity for these funds. Equity Trustees Ltd is a subsidiary of EQT Holdings Limited (ACN 607 797 615), a publicly listed company on the Australian Securities Exchange (ASX: EQT).

Forward-Looking Disclaimer

This presentation contains some forward-looking information. These statements are not guarantees of future performance and undue reliance should not be placed on them. Such forward-looking statements necessarily involve known and unknown risks and uncertainties, which may cause actual performance and financial results in future periods to differ materially from any projections of future performance or result expressed or implied by such forward-looking statements. Although forward-looking statements contained in this presentation are based upon what Coolabah Capital Investments Pty Ltd believes are reasonable assumptions, there can be no assurance that forward-looking statements will prove to be accurate, as actual results and future events could differ materially from those anticipated in such statements. Coolabah Capital Investments Pty Ltd undertakes no obligation to update forward-looking statements if circumstances or management’s estimates or opinions should change except as required by applicable securities laws. The reader is cautioned not to place undue reliance on forward-looking statements.

Never miss an update

Get the latest insights from me in your inbox when they’re published.

Sign In or Join Free to follow and be notified when I next publish

Based in Sydney, Kieran Davies is Chief Macro Strategist at Coolabah Capital Investments, an asset manager with 40 executives and over $8 billion in fixed-income strategies. Kieran is responsible for macroeconomic research and investment strategy,...

Based in Sydney, Kieran Davies is Chief Macro Strategist at Coolabah Capital Investments, an asset manager with 40 executives and over $8 billion in fixed-income strategies. Kieran is responsible for macroeconomic research and investment strategy,...