What is credit and why it’s important

Dean Italia

Medibank Private

Fixed income credit is essentially the activity of lending to groups other than Governments (which are regarded as credit risk free) - at least this can be said of the Australian government. Fixed income is the general classification of the bond market. However, bonds can be issued with fixed or floating rate of interest.

Bonds with a fixed rate have interest rate risk, where the bond price is inversely related to movements in interest rates. Interest rate risk can be avoided by focusing on bonds which pay a floating rate and benefit from higher interest rates.

The dangers of sequencing risk

Credit is likely to appeal to risk averse investors and those investors looking to avoid sequencing risk. Notwithstanding we are 10 years past the events of the global financial crisis (“GFC”), this event is likely a sobering reminder of sequencing risk. Sequencing risk relates to the timing of poor investment returns and the subsequent liquidation of assets to fund living expenses. The sale of assets at the wrong time does not allow the portfolio to ‘catch-up’ during periods when financial markets recovery, which may be years.

Credit reduces sequencing risk as it has an important characteristic that distinguishes it from equities, namely contractual cashflows. When a company borrows money it essentially promises to do two things, pay interest when due and repay principal at maturity. This contractual requirement of fixed income credit mitigates sequencing risk, since credit has a defined maturity date and provided there is no jump-to-default event, an investor will receive 100% of their principal on maturity, even if equity markets are significantly falling.

Managing the risks

Credit is not all created equal. Both duration and jump to default risk needs to be assessed and managed. Duration is the sensitivity of a bond’s price to changes in credit spreads, and jump to default risk is the risk principal is not repaid. A portfolio manager of credit manages these risks. In addition to managing duration and jump to default risk, the other benefits of a credit fund are:

- A fund allows investors to build a diversified portfolio of assets;

- A fund allows investors accessibility to over-the-counter bonds with fund managers taking advantage of pricing inefficiencies created by being non-exchange traded.

Notwithstanding what equity brokers suggest, holding higher yielding equities are not a proxy for fixed income as dividends are at the discretion of a Company’s Board and are also subject to profitability. There is a litany of examples of stocks held out as fixed income proxies (BHP, Telstra and the banks) but recent times of volatility highlight they do not trade like fixed income assets.

The benefits of compounding interest are well known, but not always considered with regards to fixed income. Excluding the payment of income tax on interest, if investors reinvest their 6.5% or 7.0% coupon every year, their capital will double in 11 years and 10 years respectively. Fixed income returns vis a vis equity returns will deliver most of the outcome via income, rather than capital gains, the opposite is generally true for equities.

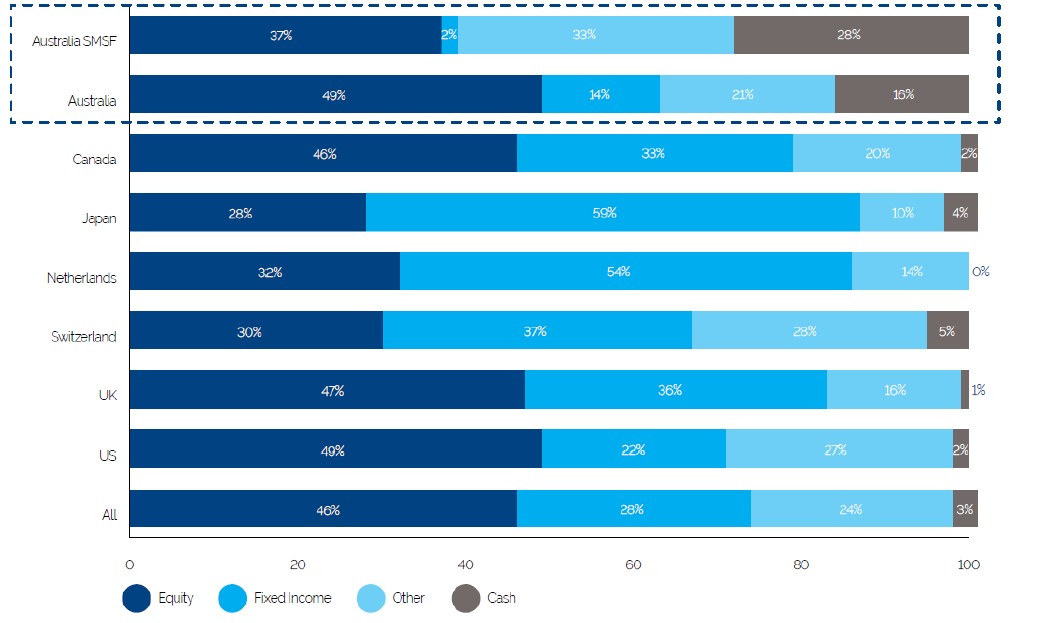

Australians are underweight fixed income relative to the world. Outside of real property Australians have a bias to shares and term deposits. The large allocation to shares essentially owes itself to dividend franking. Allocation by SMSF to fixed income is around 2% (refer Figure 1) which puts Australia in the lowest of developed world, alongside Poland and Korea. While difficult to generalise, as people move towards the later end of their working life, an increase fixed-income exposure will help preserve capital. A rule of thumb is that an investors allocation to equities is 100 minus their age with the balance in fixed income. Accordingly, someone that is 70, should have 30% in equities and 70% in fixed income. Following this ratio would moderate sequencing risk discussed previously.

Figure 1: Global Pension Fund Allocations and Australian SMSF Allocations

Source: Willis Towers Watson; ATO

Conclusion

Owing to the defensive attributes of credit, SMSF and retirees should consider an allocation to credit. Credit is likely to appeal to investors that do not like the volatility of equities, but want to enhance the income returns provided from term deposits. Further, sequencing risk may be moderated with credit’s defined maturity date, which unlike equities is perpetual.

Written by Dean Italia from Mutual Ltd

Never miss an update

Enjoy this wire? Hit the ‘like’ button to let us know.

Stay up to date with my current content by

following me below and you’ll be notified every time I post a wire

Dean Italia is Portfolio Manager of Fixed at Medibank Private. He has over 20 years financial markets experience specialising in corporate credits (financial and non-financial) and structured finance (RMBS, ABS and CMBS).

3 topics

Dean Italia

Portfolio Manager-Fixed Interest

Medibank Private

Dean Italia is Portfolio Manager of Fixed at Medibank Private. He has over 20 years financial markets experience specialising in corporate credits (financial and non-financial) and structured finance (RMBS, ABS and CMBS).

Dean Italia

Portfolio Manager-Fixed Interest

Medibank Private

Dean Italia is Portfolio Manager of Fixed at Medibank Private. He has over 20 years financial markets experience specialising in corporate credits (financial and non-financial) and structured finance (RMBS, ABS and CMBS).

Comments

Comments

Sign In or Join Free to comment