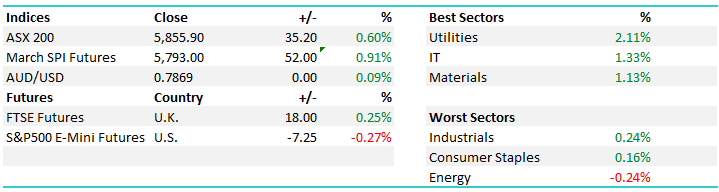

What Mattered Today; Mkt higher ahead of US inflation print on Wednesday

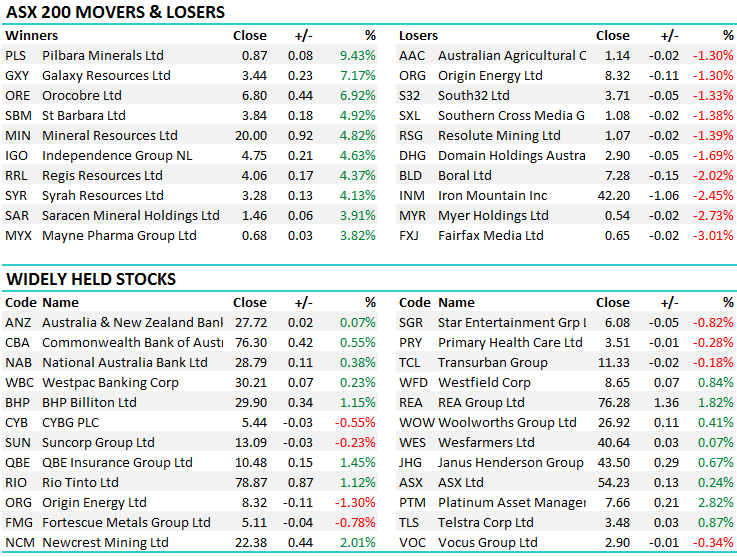

The market continued to recover today post last week’s savage selloff with some of the higher risk plays, particularly in the commodity space doing well – the Lithium Miners like Orocobre, Pilbara Minerals and Galaxy topping the leader board today (adding 6%+) while Kidman Resources (KDR) which we hold in the Platinum Portfolio put on +3.06%. A number of key companies reported today and there was some reasonable volatility as a result. Challenger Group Financial (CGF) did okay in aggregate however it was a volatile session for the annuity provider – a 7.4% daily range, while Cochlear also had a wild ride, initially trading down before recovering to close flat, a ~5% daily range. More on these results later.

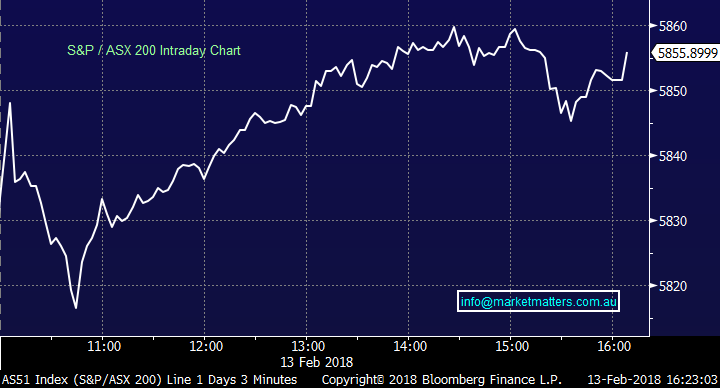

On the market today, the utilities sector was best on ground adding ~2%, the Energy stocks the worst while the broader ASX 200 put on +35pts or +0.60% to close at 5855 – the Friday morning low of 5786 last week now proving to be a reasonable buying opportunity, however the clear risk factor this week comes on Wednesday evening US time with the release of US inflation data. A strong print and the market should take another leg down, however on the flipside, a weaker result will allay a lot of the fears being played out in the mkt at the moment around an overheating US economy + a Fed Reserve that is thought to be behind the curve. Seems like a fairly binary outcome for our mkt on Thursday.

ASX 200 Intra-Day Chart

ASX 200 Daily Chart

CATCHING OUR EYE

1. Challenger Group Financial (CGF) $12.82 / -0.16%: I had a discussion with the team this morning about buying CGF into the weakness around $12 after it reported numbers that looked OK in aggregate however their guidance was a tad light on (or mkt expectations too high). The stock was hit hard early, down to a $12.05 low only to bounce back strongly. We missed it, however wouldn’t be surprised to see it trade lower from here, into a downside technical target of ~$11.50. To recap, CGF is a stock we held last year, bought at $11.95 and sold at $13.80 in the Platinum Portfolio and we’re keen to get back in here, however given cash levels, we stayed patient today.

In terms of the result all metrics were sound with a big uplift in total assets (+18% to $76.5bn) while annuity sales remained strong, with their distribution through platforms + international expansion working well. They re-affirmed FY profit guidance of $545m-$565m which was probably where the issue resided initially, given consensus was already looking for $564m, which implies top end of the range. A strong recovery from the lows to close almost flat on the session.

Challenger Daily Chart

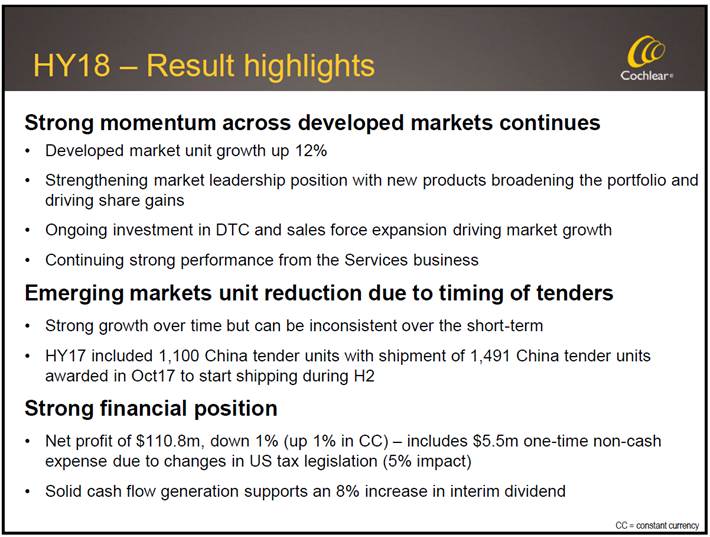

2. Cochlear (COH) $171.74 / -0.03%; Another that saw a big intra-day range today with the mkt reacting poorly to the initial result which was below in terms of the headline profit number of $110m versus the $120m consensus, however they did wear a 5.5% non-cash expense on the back of US tax changes. All up – a good result .

Cochlear Daily Chart

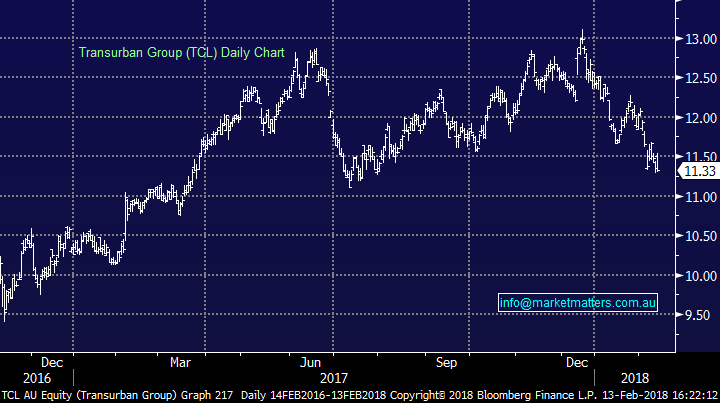

3. Transurban (TCL) $11.33 / -0.18%: Result was inline in terms of earnings however the dividend of 28cps was a tad below the 29cps expected by the market. TCL is obviously a premium infrastructure play on the ASX, an exceptionally strong business, good growth in earnings + dividends over the past 3 years of +12% with the expectation that dividends will continue to grow at a 10% clip in the years ahead – todays result supported that thesis, however the negative influence of rising US interest rates is simply too much of a headwind for us. There is a point that this looks interesting, but not yet.

Transurban Daily Chart

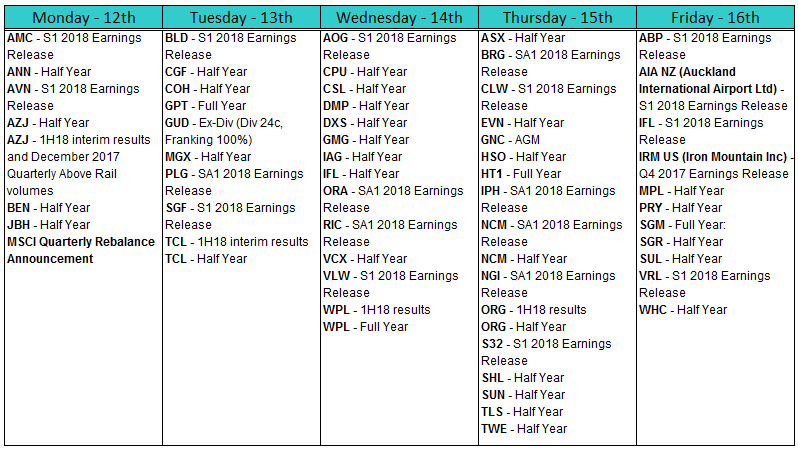

REPORTING THIS WEEK

Have a great night

James & the Market Matters Team

The above is an extract from the Market Matters Afternoon Report. To gain access to all reports for the next 14 days, including our picks into the market drop, CLICK HERE

Never miss an update

Enjoy this wire? Hit the ‘like’ button to let us know.

Stay up to date with my current content by

following me below and you’ll be notified every time I post a wire

James is Director & Lead Portfolio Manager at Market Partners - a collective of highly experienced investment professionals, operating independently, managing discretionary portfolios for wholesale investors.

James is also Portfolio Manager & primary author at Market Matters, a digital advice & investment platform with over 2500 members that offers real market intel & six portfolios open for investment.

3 stocks mentioned

James is Director & Lead Portfolio Manager at Market Partners - a collective of highly experienced investment professionals, operating independently, managing discretionary portfolios for wholesale investors. James is also Portfolio Manager &...

Expertise

James is Director & Lead Portfolio Manager at Market Partners - a collective of highly experienced investment professionals, operating independently, managing discretionary portfolios for wholesale investors. James is also Portfolio Manager &...

Expertise

Comments

Comments

Sign In or Join Free to comment