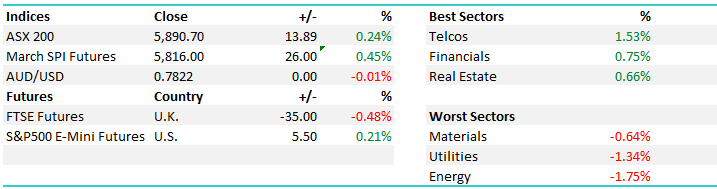

What Mattered Today; NAB rallies on decent trading update

Another calmer day for Aussie stocks with the market having bouts of indecision in early trade before buyers settled in and pushed the index up throughout the afternoon – a decent close near the session highs with the Telco stocks doing most of the heavy lifting. On the flipside, we saw weakness in the Energy space which is understandable given the decent move out of Crude in recent times.

The ASX 200 put on +13pts or +0.24% to close at 5890 – US Futures are ticking around par

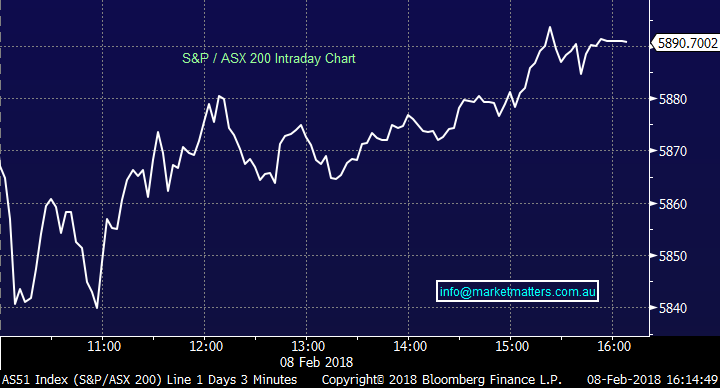

ASX 200 Intra-Day Chart

ASX 200 Daily Chart

REPORTING…

Rio Tinto (RIO) – reported yesterday and the numbers were good, underlying earnings the best since 2014 and these guys are very flush with cash – the balance sheet is in exceptional condition and there’s a strong chance of more cash going back to shareholders throughout 2018. The stock was down today on the overnight metals selloff courtesy of a stronger $US however the inflationary trade that should continue to play out in 2018 is supportive of RIO. We saw it on Tuesday when the mkt was weak, most buying into the weakness was seen amongst the miners. RIO lost -0.98% to close at $77.54 today

Rio Tinto Daily Chart

AGL (AGL) First half result was weak – they missed in terms of both revenue and underlying earnings + the divi was a miss as well and the stock was sold off by -2.05% to close at $22.01, its lowest level since early 2017

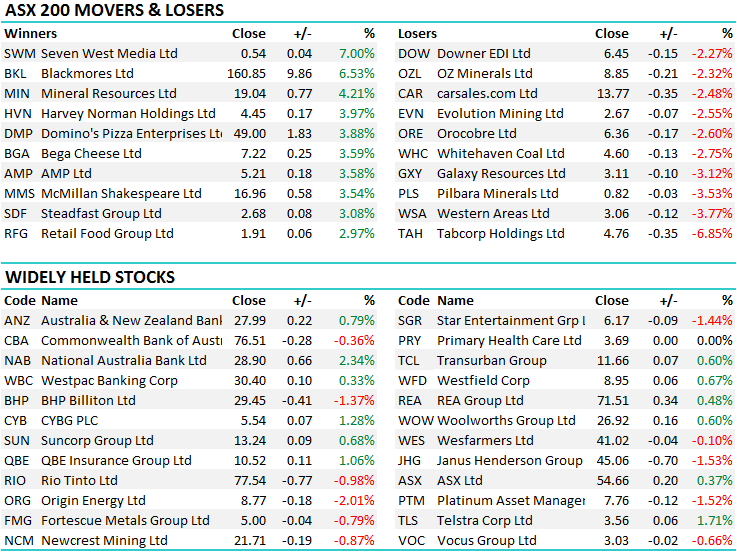

AMP (AMP) The mkt dislikes AMP – I’m not a fan either – and the result today was simply a case of being better than feared and the stock put +3.58%. Earnings a slight beat, divi was inline but underlying trends here remain weak, margins in wealth are weakening and just really, not much to entice me to step up and buy AMP.

Centuria (CMA) 1H18 operating NPAT of $19.9m which was inline / +ve while FY18 guidance reaffirmed EPS 18.6cps, DPS 18.1cps – all inline. Earnings here have experienced ~93% growth relative to pcp courtesy of acquisitions over the past 12 months - stock up +1.29% as a result . they will continue to be acquirers…

Mirvac (MGR) better headline numbers than the market thought however that was largely driven by the interest expense that came in lower than expected, as did tax – so quality of the beat low. FY18 Guidance maintained at 6-8% EPS growth, or EPS of 15.3-15.6cps, with a FY18DPS of 11.0c + they also announced plans to buy back 2.6% of its shares via an on market buy-back. It will commence 23 Feb 2018.

Mineral Resources (MIN) good result here for MIN and the stock rallied hard on the back of it – they always report at a weird time, go into a halt intra day and the mkt panics then realises it’s simply earnings – which were good. Earnings +16% higher and dividend bigger than thought. Stock rallied +4.21% to close at $19.04 following a recent pretty savage sell off.

NAB After trading near a 1 year low yesterday NAB trading update was good today – cash earnings +3% on last year, capital ok, bad debts well behaved, strong articulation of strategy and the stock bounced hard +2.34% to close at $28.90 – with some obvious rotation from the other banks – CBA down -0.36% the biggest funding vehicle, while the others were up, but not as much as NAB.

NAB Daily Chart

CATCHING OUR EYE

1.Broker Moves; Obviously reporting season is important to get a feel for underlying earnings / trends etc, however it’s also worth looking at broker reactions to results, it provides a good read into market positioning / views on particular stocks.

Here’s yesterday’s moves;

- Carsales.com Downgraded to Neutral at Macquarie; PT A$14

- Carsales.com Upgraded to Neutral at UBS; Price Target A$14

- GTN Rated New Buy at Canaccord; PT A$3.65

- Steadfast Upgraded to Buy at Morningstar

- Transurban Downgraded to Neutral at Goldman; PT A$12.26

- Macquarie Atlas Downgraded to Sell at Goldman; PT A$5.31

- Greencross Downgraded to Neutral at UBS; PT A$6.15

- Genworth Australia Raised to Neutral at Evans and Partners

- Sonic Healthcare Upgraded to Neutral at Credit Suisse; PT A$24

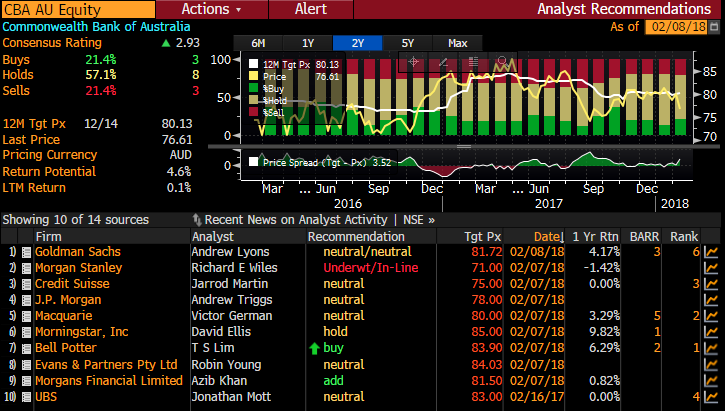

- CBA Upgraded to Buy at Bell Potter; Price Target A$83.90

We had a few questions around the topic of consensus recently given we write about it regularly, so here’s our take using CBA as an example. 14 local brokers cover CBA (Shaw and Partners do but we’re in the middle of an analyst change), of them, 57% have holds, 21% buys and the same sells. The 12 month price target is the average of all PT’s and the return potential is the different between current price and PT. All pretty straight forward – and no really earth shattering stuff.

Looking at earnings, the numbers below are the average of analysts’ expectations courtesy of Bloomberg. As you can see, earnings per share are expected to be $2.875 between 31 Dec 17 and 30th June 18. If CBA deliver that, they’ll have FY EPS of $5.69. – which all things being equal the market is positioned for. The real key to using consensus is to see how the market is positioned around a stock – are they optimistic or pessimistic? We prefer it when analysts are pessimistic more so than when analysts are optimistic as a group. Imbedded optimism creates more chance for disappointment. When our expectations around a particular stocks diverge from the consensus view, that’s when the best opportunities can arise.

Here’s a quick look at TS Lim at Bells – no 1 rated analyst of CBA according to Bloomberg at the moment – and his prevailing calls. Yesterday, he upgraded to a BUY and $83.90 target.

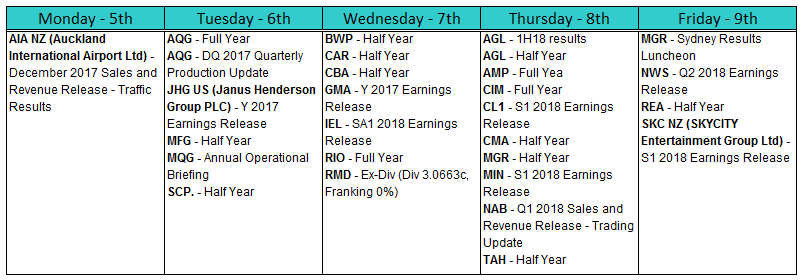

REPORTING THIS WEEK

James & the Market Matters Team

The above is an extract from the Market Matters Afternoon Report. To gain access to all reports for the next 14 days, including our picks into the market drop, CLICK HERE

Never miss an update

Enjoy this wire? Hit the ‘like’ button to let us know.

Stay up to date with my current content by

following me below and you’ll be notified every time I post a wire

James is Director & Lead Portfolio Manager at Market Partners - a collective of highly experienced investment professionals, operating independently, managing discretionary portfolios for wholesale investors.

James is also Portfolio Manager & primary author at Market Matters, a digital advice & investment platform with over 2500 members that offers real market intel & six portfolios open for investment.

8 stocks mentioned

James is Director & Lead Portfolio Manager at Market Partners - a collective of highly experienced investment professionals, operating independently, managing discretionary portfolios for wholesale investors. James is also Portfolio Manager &...

Expertise

James is Director & Lead Portfolio Manager at Market Partners - a collective of highly experienced investment professionals, operating independently, managing discretionary portfolios for wholesale investors. James is also Portfolio Manager &...

Expertise

Comments

Comments

Sign In or Join Free to comment

most popular

Equities

The Magnificent Seven can’t carry the market forever

Pzena Investment Management