What Mattered Today: Property - what crash?

Finally, a day that saw the market close near the highs of the session and importantly, above the 6000 mark for the first time in around 12 days. Some good buying in the unloved REIT sector following speculation of a deal for Westfield which went into a trading halt early with reports of a potential $20b bid for the US exposed landlord. The AFR saying that - the smart money is on a revived bid from European giant Unibail-Rodamco valuing the ASX-listed Westfield at more than $20 billion. The bid is expected to be cash and scrip in nature, and come following a strong run in both companies' share prices. It's also expected to be at about a 10 per cent premium to Westfield's last close, which is typical premium when it comes to property deals. Westfield shares last closed at $8.50, which put a $17.7 billion equity value on the company. (source AFR)

That put a decent bid tone under that sector which is good for our holdings in Vicinity (VCX) which put on +2.5% to close a $2.87 – Apparently a 6pm press conference going on but details are scarce (sort of). Anyway, a deal here would reignite the sector that everyone loves to hate at the moment given the backdrop of higher interest rates in 2018 and beyond. Similar story playing out in Sydney property with the media reporting BIG falls but for quality assets there is still decent appetite.

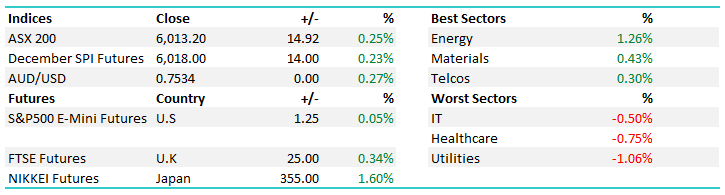

Anyway, a big day in corporate Australia and I tried to cover most this morning in Direct From The Desk – Click HERE...On the mkt today, the Energy stocks were best on ground while the utilities struggled again – the third straight session! An overall range today of +/- 16 points, a high of 6015, a low of 5599 and a close of 6013, up +15pts or +0.25%

ASX 200 Intra-Day Chart

ASX 200 Intra-Day Chart

ASX 200 Daily Chart

ASX 200 Daily Chart

FREE TRIAL - 14-days free stock market advice - all our reports including every ASX buy & sell recommendation - CLICK HERE TO REGISTER

TOP MOVERS

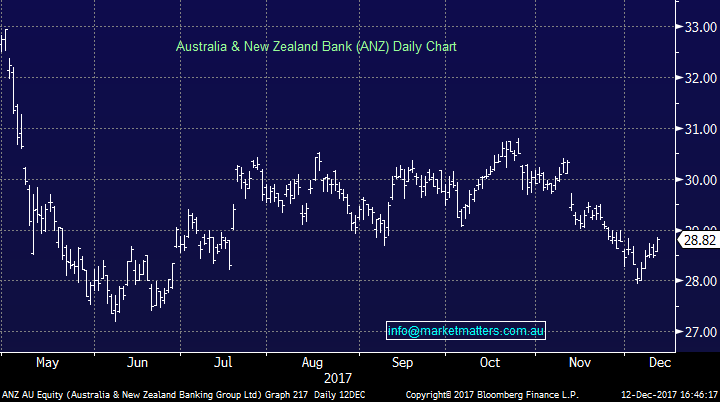

1.ANZ announced the sale of their life business this morning which is a marginal positive. Importantly, the transaction is EPS & ROE neutral assuming they conduct a buy back, adds 65bps to capital (CET1) with the completion late 2018. They sold it for 15.1 2017 PE so no real change to their earnings mix (assuming buy back is completed) but makes the bank a cleaner and simpler proposition. To give some context around the price, CBA sold Comminsure for 16.9x PE so clearly CBA look to have done a better deal. We own CBA, NAB, WBC and CYB and remain bullish the banking sector into Christmas – with the end of the December the most bullish period of the year.

ANZ Daily Chart

2. Property stocks – were the shining light on the ASX today following speculation of a bid for Westfield (WFD). WFD remains in a trading halt however Scentre Group (SCG), which is the domestic spin off of WFD was up +4.07% to close at $4.35 – clearly a big move and the wider property sector was very strong. When you get a decent multiple paid, clearly investors gets refocussed on the imbedded value in the sector over and above the media / market hype about an impending property crash. No deal announced yet, just speculation however clearly when there is smoke…!

Scentre Daily Chart

Elsewhere, we covered the major themes in the DIRECT FROM THE DESK recording early this morning. CLICK HERE

Direct From The Desk; A quick update on recent corporate activity

View

Have a great night

James & the Market Matters Team

Prices as at 12/12/17

Never miss an update

Enjoy this wire? Hit the ‘like’ button to let us know.

Stay up to date with my current content by

following me below and you’ll be notified every time I post a wire

James is Director & Lead Portfolio Manager at Market Partners - a collective of highly experienced investment professionals, operating independently, managing discretionary portfolios for wholesale investors.

James is also Portfolio Manager & primary author at Market Matters, a digital advice & investment platform with over 2500 members that offers real market intel & six portfolios open for investment.

2 stocks mentioned

James is Director & Lead Portfolio Manager at Market Partners - a collective of highly experienced investment professionals, operating independently, managing discretionary portfolios for wholesale investors. James is also Portfolio Manager &...

Expertise

James is Director & Lead Portfolio Manager at Market Partners - a collective of highly experienced investment professionals, operating independently, managing discretionary portfolios for wholesale investors. James is also Portfolio Manager &...

Expertise

Comments

Comments

Sign In or Join Free to comment