What Mattered Today: Swings & roundabouts with FMG production

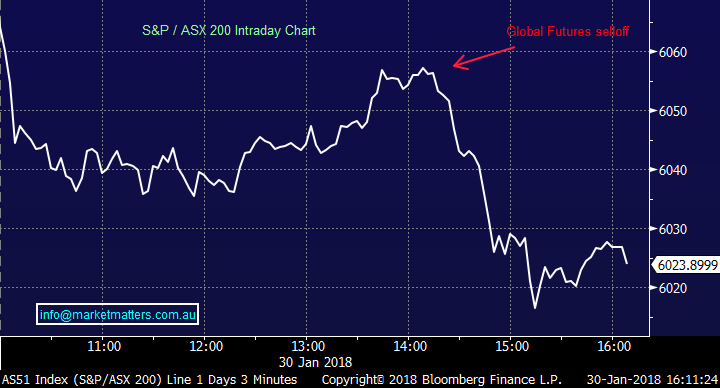

Local stocks hit the skids today courtesy of a weak lead from the US mkt overnight however we saw more selling in US Futures throughout our session today – at our close S&P Futures are trading down another -0.57% pricing a drop of ~170pts on the Dow when trading kicks off this evening. We’re starting to see an uptick in selling across global bond markets (yields higher) with the 10 year in the US printing 2.72% overnight – a big move and enough to spook equity investors as well.

In strong markets cash feels like a drag and in weak markets it never feels enough – today was weak with the mkt heading back down to test the 6000 region again with a 6016 low. Lots to get ones head around today in terms of quarterly production numbers with some big volatility in some of the names reporting, while we also had an interim result from Credit Corp (CCP) – the stock offered hard as a result ending down ~8%. More on these themes below.

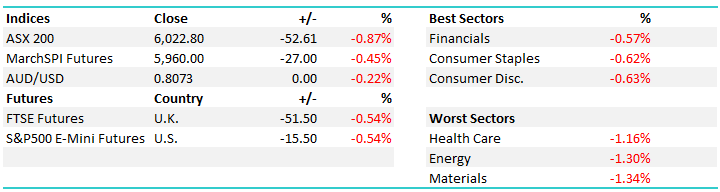

For the day the S&P/ASX 200 index lost -52 points, or -0.87 per cent, to 6022 while the All Ordinaries fell 52 points, or 0.85 per cent, to 6135.

ASX 200 Intra-Day Chart

ASX 200 Daily Chart

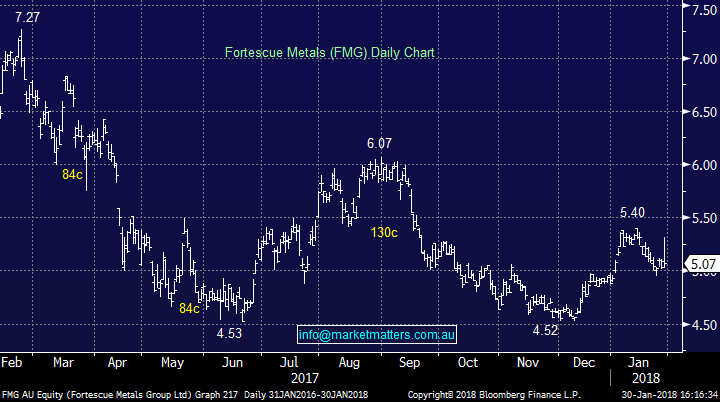

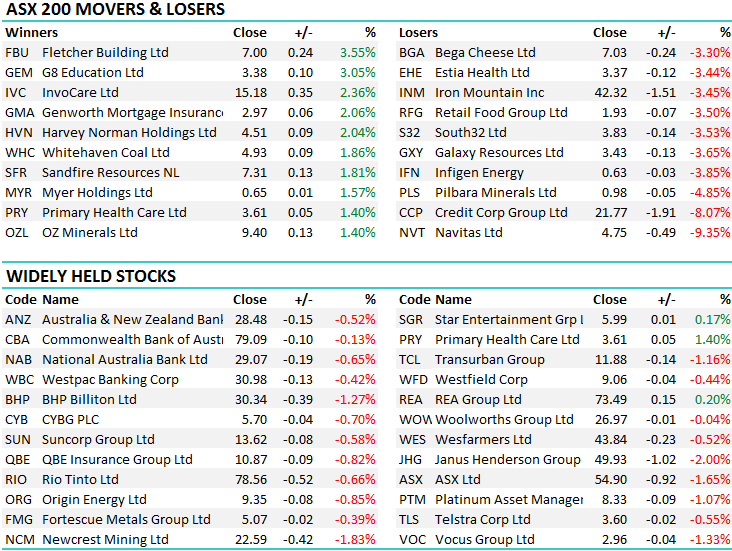

1.Foretscue Metals (FMG) $5.07 / -0.39%; Big volatility in FMG today with some curly parts to their Dec QTR production numbers offset by some reasonable commentary in terms Iron Ore demand and trends in terms of price realization. In short, the scorecard was OK on prodn/sales, costs & guidance although a slight miss on price realization offset to a degree of optimism around a potential ‘inflexion point’ mid Jan. In simple terms, FMG mine Iron Ore, it’s lower quality than others so a discount is applied versus the benchmark. A combination of some softer demand, environmental curbs in China which reduced the appetite for lower quality inputs and the discount that FMG usually gets blew out. In the Dec QTR that discount was bigger than the mkt thought it would, coming in at 34% versus the 1H18 discount of 32%.

However, similar to what we saw recently from White Haven Coal (WHC) who produce lower quality Met Coal (goes into Steel making) they saw a change in buying demand from mid Jan as well. So what does this all mean? In short, the discount should ease in 2H18 and is likely to land in their guidance range – 70-75% realisation or a 25-30% discount.

Elsewhere, costs still on the down low and getting better hitting a record qtrly low at US$12.08, a tad lower than $12.15 in SQ17. Guidance also maintained at US11-12/t which is a lot better than RIO and BHP. Net debt ticked up a bit but we / the mkt expected that given a few one offs that I won’t go into. Despite that, balance sheet still strong and free cash running at the rate of ~12% annualised yield. C1 cost guidance for the full year is maintained at $11-12/wmt: FY18 full year price realisation guidance is maintained at 70-75% of the Platts 62 CFR.

Overall – we like it here, we bought it ‘controversially’ for our Income Portfolio at $4.99 but would add to into further weakness if it played out.

Fortescue Metals Daily Chart - 6+% range in FMG today which is BIG

2. IOOF (IFL) $10.78 / -0.65%; IFL announced their December Funds Under Management, Advice and Supervision (FUMAS) numbers today, printing +4.7% growth in the figure over the quarter to $154.6bil total – big number and a record for IFL, now regaining all FUMAS lost to JHG in 2015 after selling the Perennial business at the time. IOOF has been a big winner in the advice space with a mass outflow from the big banks and life insurers – seems that Financial Planners now want to distance themselves from the big banks, I would too if I operated in that space (which I don’t). Anyway, much of the uplift can be attributed to the addition of 43 advisers over the quarter, and IFL will soon sit one notch behind AMP as the largest advice business in Australia. The leverage here is around the lower cost base post the ANZ Wealth acquisition (courtesy of synergies) with these benefits coming into the fray later in the year.

The stock drifted slightly today but the mkt was weak and it did outperform - the result was in line / slightly better in our view. We own IFL in the Platinum Portfolio and remain comfortable for now

IOOF Daily Chart

3. Newcrest Mining (NCM) $22.59/ -1.83%: Gold was weak overnight and down another $6 during Asian today which didn’t help, however NCM didn’t help themselves either with a 2Q scorecard that was on the lower end of the expected range – they printed 613k/oz versus consensus of 643k/oz while they did maintain full year production guidance of 2.4-2.7m/oz which is a positive.

Never the less, our main concern for gold at the moment and this is obviously relevant for EVN below, is a short term low in the US currency as we wrote about yesterday / and again this morning seems likely which should put the kibosh on Gold in the short term. We own NCM (reluctantly), think it’s a self-help story, is cheap v global and local peers and will print better numbers over time – it’s just the timing that’s the issue. Our trigger finger is getting itchy on this holding.

Newcrest Daily Chart

4. Evolution Mining $2.77 / +0.36%; another solid quarter for Evolution, “on track to comfortably deliver FY18” guidance with production expected at the higher end of guidance alongside reporting a record low cost of $784/oz. An effort was also made to lower debt, falling 32% in the quarter to reduce gearing to 9.5% - net debt around $230m when the mkt was expecting around $250m. A really good result here, better than its bigger rival above.

Evolution Daily Chart

5. Sandfire Resources (SFR) $7.31 / +1.81%; maintained guidance across gold and copper but said it would be at the upper end which was a good result. Dec QTR Copper production was inline at 16k/tonnes while they provided good colour in terms of their development projects saying progress made in Doolgunna (WA – copper/gold) and Black Butte (USA - copper) sites. A good result overall

Sandfire Daily Chart

6. Credit Corp (CCP) $21.77 /-8.07%: Morgan’s upgraded yesterday moving their PT up +5.8% to $23.80 while other brokers that cover this stock are reasonably keen on it, however the interim result today from CCP was a clear miss – mainly around the volume of purchased debt ledgers (PDLs). In short, they buy distressed debt from banks and others at a percentage in the dollar then back themselves to collect that and more. PDL’s are like their inventory and it seems the mkt has become more competitive here, pushing up the costs of that ‘inventory’. They’ve pulled back on their buying as a result which is sensible in the long term, however in the short term we see likely earnings downgrades as a result. It trades on a reasonable PE of 20 current and around 17 forward so not cheap, but not expensive, my concern lies around the mkts positioning which is clearly on the long side of the trade here – $19 downside target.

Credit Corp Daily Chart

FREE TRIAL - 14-days free stock market advice - all our reports including every ASX buy & sell recommendation - CLICK HERE TO REGISTER

Have a great night

James & The Market Matters Team

Never miss an update

Enjoy this wire? Hit the ‘like’ button to let us know.

Stay up to date with my current content by

following me below and you’ll be notified every time I post a wire

James is the Lead Portfolio Manager & primary author at Market Matters, a digital advice & investment platform with over 2500 members that offers real market intel & portfolios open for investment. He is also a Senior Portfolio Manager at Shaw and Partners heading up a team that manages direct domestic and international equity & fixed-income portfolios for wholesale investors.

6 stocks mentioned

James is the Lead Portfolio Manager & primary author at Market Matters, a digital advice & investment platform with over 2500 members that offers real market intel & portfolios open for investment. He is also a Senior Portfolio Manager at Shaw and...

Expertise

James is the Lead Portfolio Manager & primary author at Market Matters, a digital advice & investment platform with over 2500 members that offers real market intel & portfolios open for investment. He is also a Senior Portfolio Manager at Shaw and...

Expertise

Comments

Comments

Sign In or Join Free to comment

most popular

Equities

Buy Hold Sell: 2 standout ASX names for FY26

Livewire Markets

Commodities

Central banks are doubling down on gold - should you?

Livewire Markets