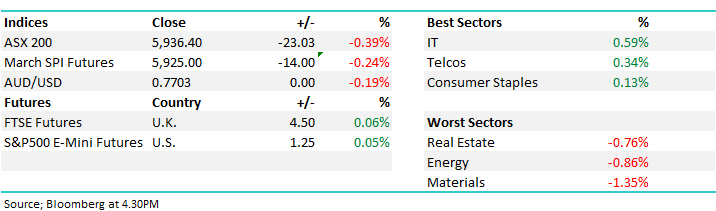

What Mattered Today; TPG & Kathmandu in focus

The market sold off early on the back of the Tech led sell off in the States overnight that saw American indices down around ~1.5% thanks to reports of a data leak within Facebook (OMG!!) + there were a few other factors at play that we wrote about this morning, namely 1. Corporate Bond Markets we think are generating a warning sign for riskier assets like equities 2. A transition deal on BREXIT was agreed which was to be expected, but a positive non-the-less, particularly for their currency which should translate well for our holding in CYBG at some point.

So after the initial sell off with the mkt down ~45points we recovered and closed down -23pts or -0.39% to 5936 (i.e. well off the lows). The banks as a collective were actually higher on the session which is a reasonable sign, remember we want to be seeing stocks rallying, or at least shrugging off bad news and with the combination of weaker overseas markets + the ongoing Royal Commission the news was far from supportive today – yet all – bar NAB – finished in the black.

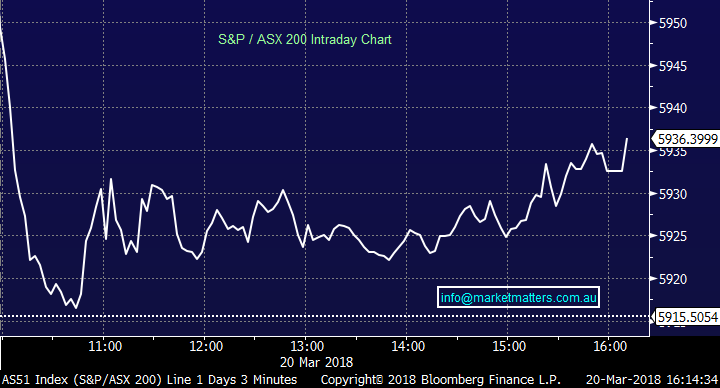

ASX 200 Chart – mkt grinded higher throughout the day

ASX 200 Chart

CATCHING OUR EYE

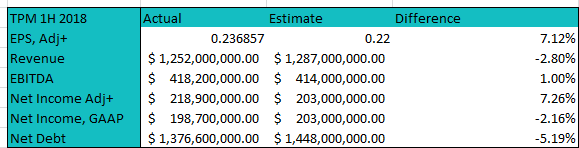

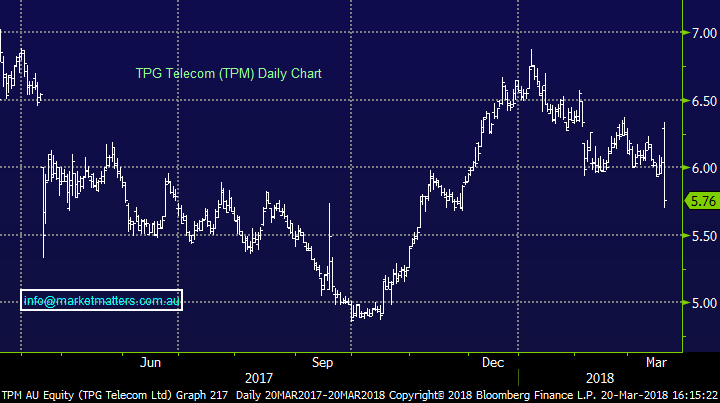

TPG Telecom (TPM) $5.76 / -4.64%; A wild ride today for TPG stock with the share pricing trading in a ~10% range, which is clearly big after they reported half year earnings before market this morning. There was some obvious confusion around the result with a positive initial reaction followed by some fairly aggressive selling thereafter. I was on Sky Business just after the result dropped suggesting it was a reasonable one given clear headwinds / uncertainty facing the sector, however it seems the consensus disagrees.

We don’t own the stock and would be reluctant to step in given we own Telstra around current levels, however the result (we thought) was reasonable on first look. Underlying earnings beat expectations once an amortization change was taken out, and the EBITDA line printed a marginal beat (1%). Revenue was a miss , net debt was better + they upped FY guidance slightly – the mkt had EBITDA at $817m with the company saying they now expect $825m to $835m – however the reason for the upgrade was actually a slowdown in the NBN roll out, so it’s just a delay in feeling the earnings hit rather than an upgrade on underlying operational strength. Importantly they also said that mobile build is on track / budget both locally and in Singapore while they announced a 2cps dividend – not sure why really given the huge capex requirements going forward!

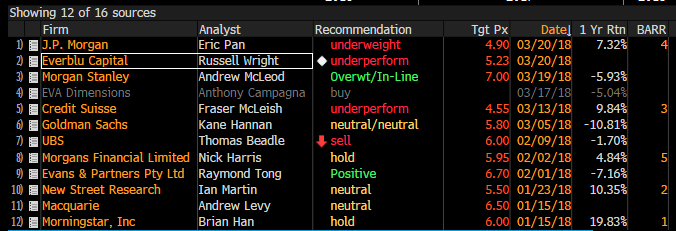

We don’t own the stock however it’s on our radar as a short term vehicle given the very mixed analyst expectations….often creates opportunity when the consensus gets it wrong.

Analyst Expectations – TPG

TPM Telecom (TPM) Chart

Kathmandu (KMD) $2.30 / unch; Also reported half year numbers this morning which were okay however they announced an acquisition and $60m capital raising at $2.16 per share + SPP at the same level. We haven’t looked closely at KMD for some time however the announcement today – buying a manufacturer / wholesale distributor of footwear (Oboz) + other outdoor accessories mainly targeted to the North American mkt makes a lot of sense in our view. Retail is clearly tough domestically, however those businesses that are focussed (like Nick Scali) have continued to do okay.

In the case of KMD, they trade on 12x and a 6% yield which is about the average they’ve traded at last year, however in 2016 they had an average PE of 15x, so we’ve seen a decline in earnings + a re-rate on the multiple. The acquisition announced today, while not huge is a step in the right direction. It will be EPS accretive by mid-single digits by FY19 and is a clear move in the right direction which could underpin a multiple re-rate and see the stock price rally back reasonably hard.

The stock will likely get hit when it comes out of the halt however this is a stock worth a look –some more work at least as an income play that has a very low correlation to the market…

Kathmandu (KMD) Chart

Have a great night

James & the Market Matters Team

The above is an extract from the Market Matters afternoon Report. For a free 14 day trial of our service CLICK HERE

Never miss an update

Enjoy this wire? Hit the ‘like’ button to let us know.

Stay up to date with my current content by

following me below and you’ll be notified every time I post a wire

James is the Lead Portfolio Manager & primary author at Market Matters, a digital advice & investment platform with over 2500 members that offers real market intel & portfolios open for investment. He is also a Senior Portfolio Manager at Shaw and Partners heading up a team that manages direct domestic and international equity & fixed-income portfolios for wholesale investors.

2 stocks mentioned

James is the Lead Portfolio Manager & primary author at Market Matters, a digital advice & investment platform with over 2500 members that offers real market intel & portfolios open for investment. He is also a Senior Portfolio Manager at Shaw and...

Expertise

James is the Lead Portfolio Manager & primary author at Market Matters, a digital advice & investment platform with over 2500 members that offers real market intel & portfolios open for investment. He is also a Senior Portfolio Manager at Shaw and...

Expertise

Comments

Comments

Sign In or Join Free to comment

most popular

Equities

High conviction: What we’re backing for the long term

Livewire Markets