3 fundies and the opportunities they see

No-one saw it coming, and no-one wants it to stay. Covid-19 was the Black Swan that roiled society, cascaded into markets and triggered a global economic downturn that has forced central banks and governments into unleashing their monetary and fiscal bazookas.

The disruption to everyday life has been compounded with the pain of over $20 trillion in losses across global capital markets.

While the moves in markets are extreme, there will be a point when things normalise. But when is that? And how should investors be positioned and have the steep falls in markets created opportunities for the brave? We reached out to three fund managers for their take. Responses come from Dermot Ryan, AMP Capital; Emanuel Datt, Datt Capital and Thomas Poullaouec, T. Rowe Price.

Q. What is your base case for the global economy over the next 6-12 months?

Dermot Ryan, AMP Capital

Markets up to this point have been behind the curve. This may play out longer than the markets expected. Can we compare the duration of what happened over three months in the Wuhan shutdown (where unknown pneumonia cases started to appear in early December) to what is now happening in Milan and now other major regions in the western world?

Which country will come out of this crisis first? If the situation in China is as it is currently presented, then they may have a chance of coming out of this situation first. But we are monitoring the situation closely and trying to get an independent read on actual activity on the ground and through indirect means, as this wouldn’t be the first example of communist propaganda in history.

Emanuel Datt, Datt Capital

In our opinion, there is no doubt that the global economy will be affected in the short term by the spread and consequent fear of COVID-19. We expect there will continue to be significant volatility in the short term.

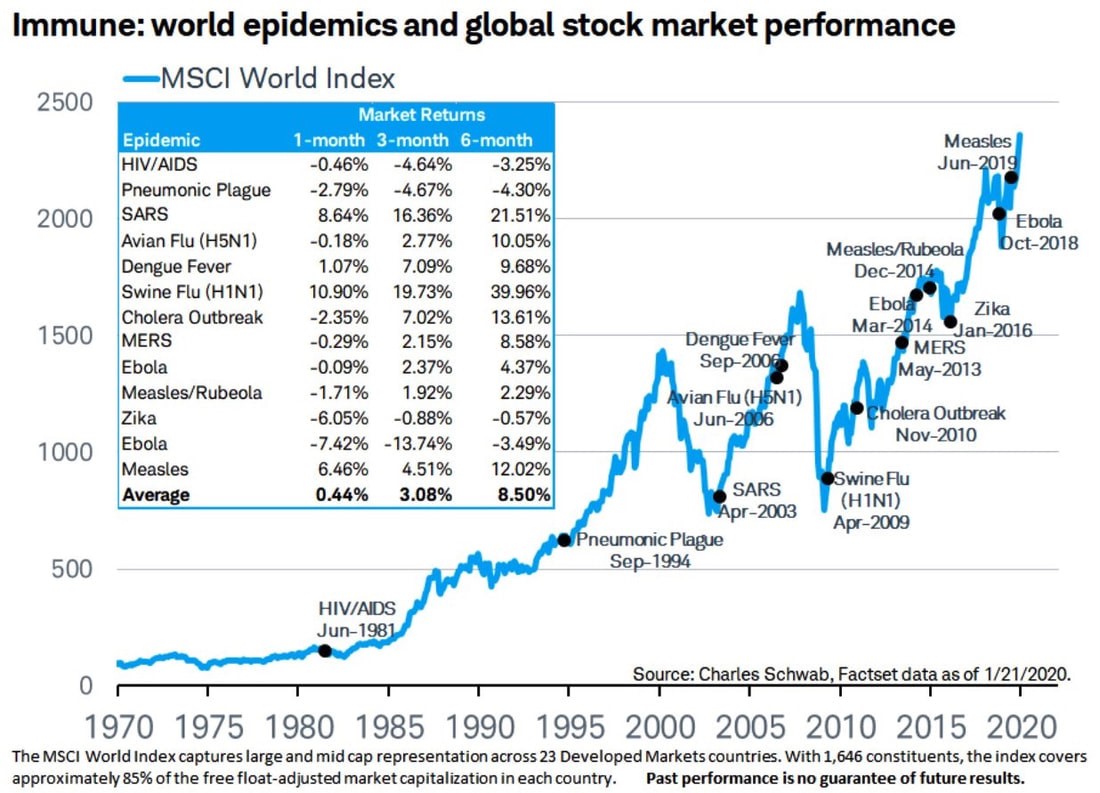

However, over the next 6-12 months, we believe the global economy will recover however will remain sensitive to and driven by geopolitical circumstances; some which have contributed to the recent equity market downturn. We note on average, global markets enjoy positive returns of 8.5% 6 months post an epidemic historically, with downside limited to a low single-digit negative return.

We also note the success that China and South Korea have had in containing the spread of COVID-19 and expect most nations to follow suit over the next month or so.

Thomas Poullaouec, T. Rowe Price

The effect of the coronavirus has had on the global economy and markets has destroyed the hope for a more “normal” market in 2020. Until we get more certainty about when the behaviour will revert to normal, we could anticipate heightened levels of volatility to continue.

Looking at a 6 to 18-month horizon, there are opportunities for investors to look past this downturn.

While volatility is expected to persist, recovery can be just as swift and sudden. The volatility also creates some opportunities to re-position portfolios. Investors can leverage opportunities to look for distressed valuations. Monetary policy and fiscal policies are creating the conditions prone to a sharp rebound after the worst of the virus outbreak is over.

Q. What are your expectations for performance across asset classes, and how are you positioned?

Dermot Ryan, AMP Capital

Our process focusses on investing in stocks with good cashflows and strong balance sheets, solvency can be a problem for companies with too much debt or leveraged businesses.

The question you need to ask about stocks in your portfolio is can they trade through a disruption like this?

Emanuel Datt, Datt Capital

Our asset allocation position is as follows:

- Debt ~45%

- Equities ~45%

- Cash ~10%

Should the COVID-19 pandemic be brought under control, we expect a significant shift in capital flows from fixed income into equities.

We expect yields on longer duration sovereign instruments to increase and equity markets to rise across the board. We could see some sovereign debt issues begin to show in European nations which are highly leveraged and have been affected by the COVID-19 lockdown.

We expect some softness in commercial property markets, due to yield expansion and a decrease in capital available to the sector. In addition, we expect some softness in commercial tenancies as behavioural modifications from the COVID-19 quarantine may be adopted on a more permanent basis by some tenants.

Many alternative strategies rely on market liquidity, the availability of leverage and ability to borrow stock. We broadly anticipate more volatility and downside risk in alternative strategies due to changes in these three important factors over the past week.

Thomas Poullaouec, T. Rowe Price

We have a slight overweight position in equities as valuations are more reasonable relative to extreme lows in bond yields amid the market sell-off. Central bank policy is supportive, yet the outlook is clouded by impacts of the virus. Bond yields are hitting record lows on risk-off sentiment and credit spreads are widening, but we think they are not at extreme levels. Fundamentals are broadly supportive. Therefore, we are maintaining a slight underweight to bonds while monitoring the impacts of the virus on vulnerable sectors.

The low yield environment and low growth justify a constant allocation to alternative investments, which we maintain a neutral position for. There’s also a need for uncorrelated assets, such as hedge funds, at a time of increased volatility.

Q. What changes have you made to your portfolio in light of recent market movements?

Dermot Ryan, AMP Capital

- We are starting to sell some of our defensive stocks and turn into cyclically exposed stocks, but only in names with good balance sheets as we are entering a phase where some companies may need to raise capital in a very difficult market.

- Australian banks have sold off due to the large drop in the yield curve to record lows, which suggests that net interest margin squeeze will continue. But credit quality is still expected to stay strong and our banks are funded with good capital. Some overseas jurisdictions are seeing banks suspend interest payments for individuals and businesses impacted by the virus, so we can’t rule that out here down the line.

- We are overweight infrastructure, rail and utility stocks as we like the resilience of the earnings in those businesses.

- Travel stocks will be a good rebound trade; however, we believe in the short-term working capital and increased reluctance for corporates and leisure travel will mean we are seeing airlines globally grounding large parts of their fleet.

- Supermarkets are benefiting with a surge of stocking capacity but are already on quite high valuations, so upside is perhaps limited.

- With more people working from home, telcos will also benefit as people upgrade broadband and mobile data packages. Telcos are already showing encouraging signs as mobile price wars abate and average revenue per user on their networks grow.

Overall, it’s difficult but vitally important to stay calm and make long term decisions. Don’t panic or make rash changes to your investment strategy or asset allocation, in fact look for opportunities to deploy long term investments in equities at attractive valuations.

Emanuel Datt, Datt Capital

Our strategy has not changed amongst the recent chaos. Our portfolio is anchored by private debt opportunities which are secured against real assets at low leverage. We also tend to hold larger amounts of cash than a typical fund manager. This assists us in mitigating equity market risk and allow us to take advantage of equity market volatility when others may be selling.

We have been finding some exceptional equity opportunities which we have been selectively deploying capital into. Our strategy of focusing on opportunities which have clear catalysts and elements of hidden value has not changed through this period.

Thomas Poullaouec, T. Rowe Price

While uncertainty may persist near-term, we took the opportunity to add to equities as the swift repricing has offered more attractive relative valuations for stocks as bonds have become increasingly expensive.

- Within U.S. equities, we trimmed exposure to growth stocks and added to value as cyclically oriented companies have sold off more, further expanding relative valuations in favour of value stocks which could see a more pronounced rebound.

- Within fixed income, we reduced our exposure to emerging market bonds as they may be vulnerable to further downside risk given current valuation levels and a growing list of idiosyncratic concerns.

In conclusion

As the saying goes "history doesn't repeat itself but it often does rhyme". Societies and markets have been through pandemics before and human ingenuity has meant we've come out stronger.

For investors, the key will be to weather the storm by making sensible decisions, holding good quality assets, considering diversifying further and taking advantage of opportunities as they emerge.

Never miss an update

Stay up to date with my content by hitting the 'follow' button below and you'll be notified every time I post a wire. Not already a Livewire member? Sign up today to get free access to investment ideas and strategies from Australia's leading investors.

Never miss an update

Enjoy this wire? Hit the ‘like’ button to let us know.

Stay up to date with my current content by

following me below and you’ll be notified every time I post a wire

Based in Canada, Vishal has over 15 years' experience in financial journalism and has a particular interest in property, exchange-traded funds (ETFs), investing strategy and financial history.

3 topics

2 contributors mentioned

Based in Canada, Vishal has over 15 years' experience in financial journalism and has a particular interest in property, exchange-traded funds (ETFs), investing strategy and financial history.

Expertise

Based in Canada, Vishal has over 15 years' experience in financial journalism and has a particular interest in property, exchange-traded funds (ETFs), investing strategy and financial history.

Expertise

Comments

Comments

Sign In or Join Free to comment