TOL - 3rd Aug, 2022

Citi's case for an iron ore rebound - and how it affects the ASX miners

When people think of investing in Australian assets, three things probably spring to mind:

- sky-high property prices,

- generous dividends, and

- our inextricable links to the Chinese economy.

Within our local market, these considerations are most crucial for the Big Three iron ore miners. The miners are also vital to every equities investor.

Even if you only invest in the ASX 200, 10% of the index is already beholden to just one name - BHP Group ASX:BHP. The same can be said about the popular Vanguard Australian Shares Index ETF ASX:VAS.

But there has been a big change over the last few months. From a peak of US$214/tonne in June 2021, the price of the most actively traded futures contract for Dalian iron ore has collapsed to just US$107/tonne, as of recording.

Having said this, it's still an incredible run-up from a low of just under US$40/tonne in 2016.

So, is the multi-year bull market for iron ore finally ending - and are more falls ahead? Or are we at a turning point for a new supercycle? This wire will examine that question in great detail, with the help of a note from Citigroup's commodities analysts and Rio Tinto's ASX: RIO recent earnings report.

Citigroup's case

Positive policy moves are the basis for Citi's shift in tone around the price of iron ore. Analysts led by Paul McTaggart believe China's monetary policies are easing - and that all this new stimulus could provide a healthy lift for the precious export.

On the supply side, McTaggart and the team believe lower iron ore prices have seen a significant reduction in seaborne supply from smaller suppliers. Couple this backdrop with a lack of domestic production given the country's zero-COVID lockdowns and they think that the iron ore price could perform strongly through the end of the year.

The only catch? China's property sector

The protests, backlash against mortgage repayments, and debt defaults have dominated headlines for many months now. Iron ore is used to create steel, which has been crucial for China's property development space.

But if projects are not being done and cities are being blown up before they are finished, how is the outlook for iron ore demand anything less than muddy?

McTaggart's team says you only need to look at the data. The demand-supply "delta" (a finance term referring to the rate of change) is turning positive. Indeed, new home starts and completions are outpacing the rate of ongoing projects. This differential is traditionally a leading indicator for iron ore price movements - one way or the other.

The following chart is an example of this "delta" that the team refers to:

The next chart is an example of their thesis - how more property starts are a leading indicator for iron ore's price moves:

Which iron ore miners is Citi buying?

The two larger ones, in short. Citi argues that the savage sell-off in iron ore miners coupled with a friendly monetary policy from Beijing will be great news for the ASX Big Three. And what's more, a weaker Australian dollar (in turn, caused by an incredibly strong US Dollar) will be great news given the cost to export the commodity is cheaper in these times.

Of the three major names, Citi is buying two based on valuation and potential dividend yields - BHP and Rio Tinto. And, as a bonus, while not strictly an iron ore-focused name, they are also keen on South32 (ASX: S32). Fortescue gets a "hold" rating.

But have the analysts read this?

Speaking of Rio Tinto, the company handed down its latest quarterly earnings report last week. And this line caught my attention in preparation for this story:

As a result, we are paying our second highest ever interim dividend of $4.3 billion, a 50% payout, in line with our policy. The market environment has become more challenging at the end of the period.

The first part sounds really good, right? $4 billion in dividends? Then, those cheers get very quickly silenced by the next bit - the market environment has become challenging.

The $4 billion figure was also touted by management as the second largest payout ever. However, you don't have to dig far to find out that last year's payout (the largest ever) was more than double this year's figure at $9 billion.

Even in payout terms, the proportion has reduced from a recent average of 65% to 50%.

While this is a company-specific story, it will be interesting to see how the other major miners handle this period of intense headwinds and negative headlines around the Chinese property sector. To add to their woes, recent media reporting has suggested the Chinese government has backed a new "giant" called (oddly enough) Mineral Resources Group.

The aim is to renegotiate the prices that the country's steel producers get for the iron ore it imports.

And if the bargaining fails, they could restart even more home-grown iron ore plants or look to other places like Mongolia and parts of Africa. Or it could just go independent completely and even shut out Australia as an iron ore source.

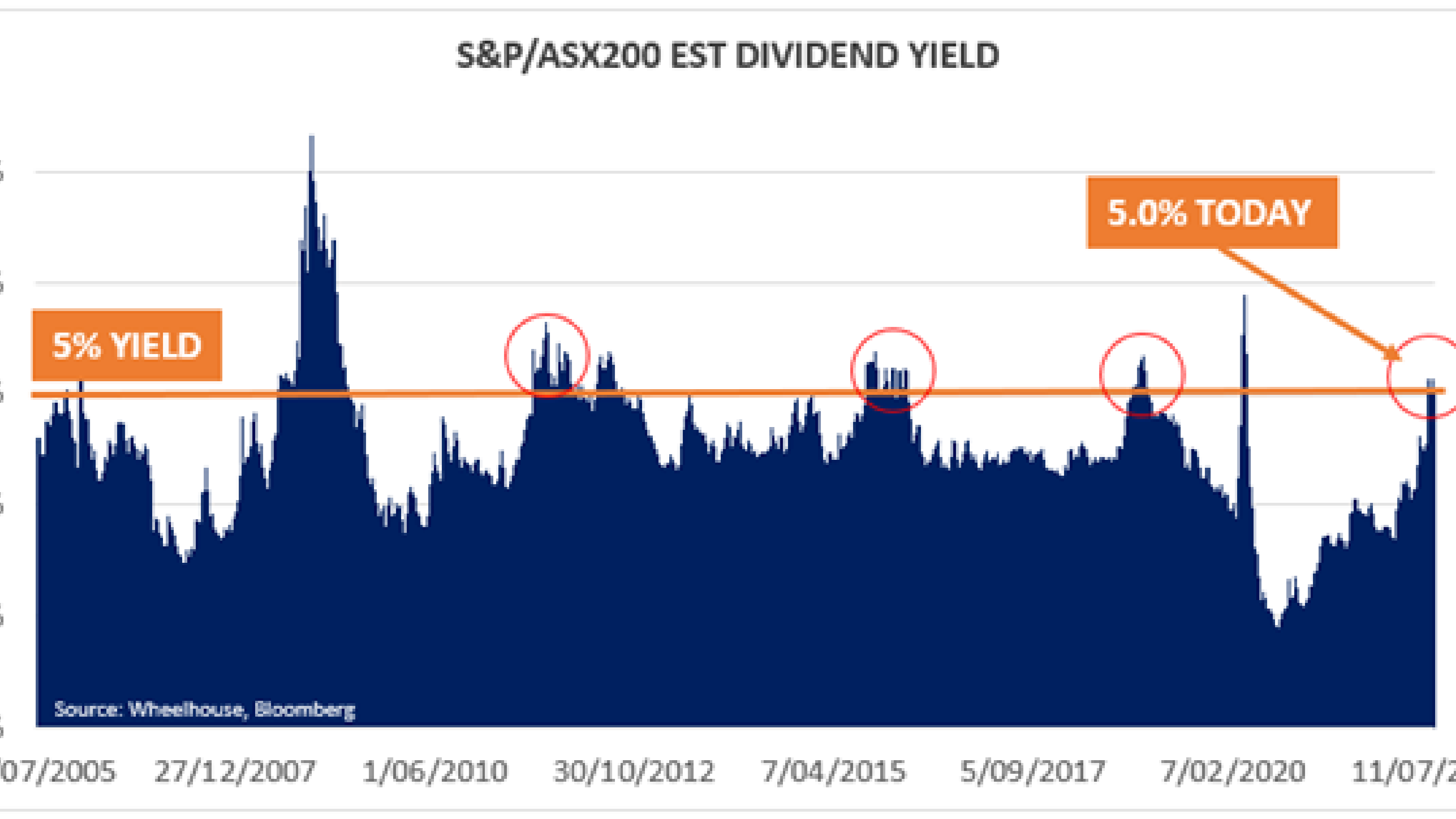

The dividend story was also discussed by Alastair MacLeod at Wheelhouse Partners, who argues that there is a new danger in trying to extrapolate future dividend payouts:

Equities

The ASX200 is yielding 5%, is the market a buy?

View

As a bonus, you can also read about Macquarie's take on the BHP quarterly earnings report in a recent edition of Charts and Caffeine:

Daily Report

BHP earnings please brokers despite soft outlook

View

For now, all investors need to focus their eyes on are two dates this month. They are:

- BHP's full-year report (August 16th)

- Fortescue's full-year report (August 29th)

It is there we will find out if Rio Tinto's story is just a Rio story - or something a lot more sinister. If it's the latter, then UBS' call to downgrade Fortescue Metals (ASX: FMG) to a sell from neutral may very well be vindicated.

Never miss an insight

If you're not an existing Livewire subscriber you can sign up to get free access to investment ideas and strategies from Australia's leading investors.

Never miss an update

Enjoy this wire? Hit the ‘like’ button to let us know.

Stay up to date with my current content by

following me below and you’ll be notified every time I post a wire

This is an archived profile. Hans was a senior editor at Livewire Markets from April 2022 to February 2025.

........

Livewire gives readers access to information and educational content provided by financial services professionals and companies (“Livewire Contributors”). Livewire does not operate under an Australian financial services licence and relies on the exemption available under section 911A(2)(eb) of the Corporations Act 2001 (Cth) in respect of any advice given. Any advice on this site is general in nature and does not take into consideration your objectives, financial situation or needs. Before making a decision please consider these and any relevant Product Disclosure Statement. Livewire has commercial relationships with some Livewire Contributors.

4 topics

5 stocks mentioned

1 contributor mentioned

This is an archived profile. Hans was a senior editor at Livewire Markets from April 2022 to February 2025.

Expertise

This is an archived profile. Hans was a senior editor at Livewire Markets from April 2022 to February 2025.

Expertise

Comments

Comments

Sign In or Join Free to comment

most popular

Funds

The 5 best-performing super funds of the year

Livewire Markets

Equities

Buy Hold Sell: 5 ASX stayers built to go the distance

Livewire Markets