Why invest in Small Caps?

Investing in smaller companies has traditionally been a core strategy to achieving significant long term wealth generation for high net worth individuals, family offices, entrepreneurs, etc. And for good reason - we believe there are many compelling reasons to include smaller companies in all portfolios. In this article we investigate why smaller company investing can be so lucrative and the core strategies behind successful smaller company investing…

Why Small Caps?

The evidence

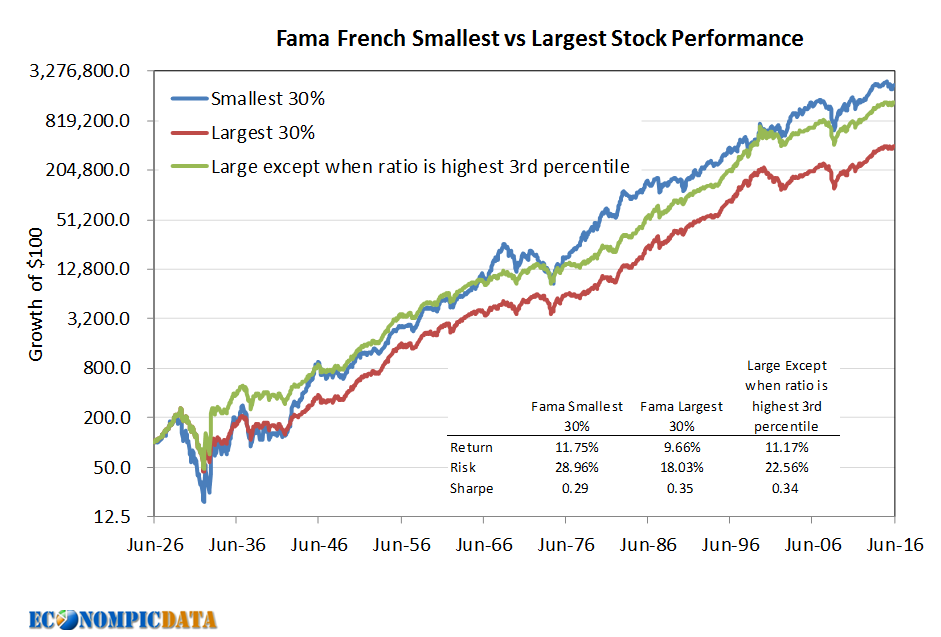

There seems to be consensual agreement in research circles that smaller companies tend to out-perform larger companies over the long term. As you would expect the vast majority of the research in this area has been focused upon the US market so we’ll be primarily looking at US-based evidence. However, the conclusions remain valid for ASX investors in our experience. The chart below shows the long term returns of the smallest 30% of listed US stocks versus the largest 30% over the past 90 years. The data shows that the smallest 30% have on average out-performed the largest 30% by 2.1% through this period.

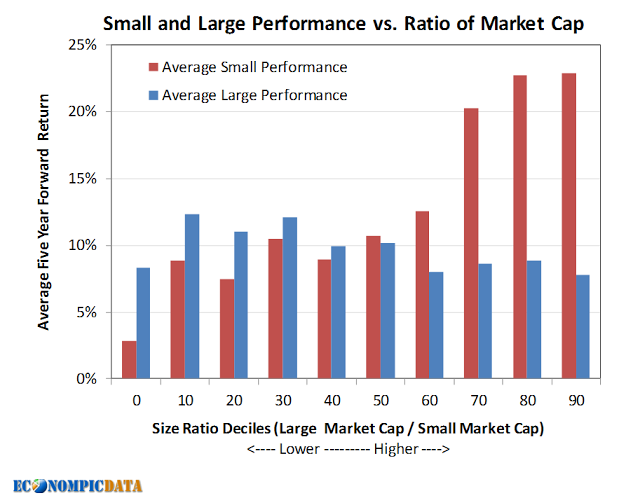

And if we look at the same data and break to down into market cap deciles, the results become even clearer - the smaller the average market cap, the higher the average out-performance. The chart below shows (on the right) the top decile largest companies (by size) versus the the top decile smallest companies and compares their performance. Each step towards the left is one decile lower in the size ratio. The trend is clear:

This data provides compelling evidence that smaller companies offer ripe picking grounds for out-sized long term returns.

This is consistent with our experience in the DMX Capital Partners fund which is 72% ahead of the All Ords after fees since launch 17 months ago - this out-performance reflects the combination of applying a value investing style to a filtered universe of high quality smaller companies:

Why smaller companies tend to outperform

[DMX3.PNG]

In our opinion there are a number of compelling reasons why the strategy of investing in smaller companies tends to out-perform the market over the long term:

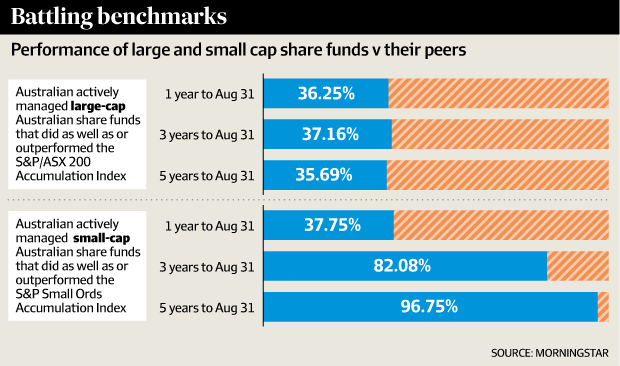

1. A less efficient market - One of the great attractions of smaller company investing is that the majority of ASX listed smaller companies remain below the radar of most investors. Rather than competing with some 30 analysts who each have a detailed financial model on the company as is often the case in the larger company universe, there is often no broker coverage of smaller companies. And beyond the low broker coverage we often work on companies which have very few individual investors following them. This lack of coverage, and resulting lack of analysis, creates significant room for market inefficiencies in the stock valuation, and also leaves ample room for smaller company investors to generate an information edge versus the limited market following. As the market becomes more aware of these initially unknown companies, the potential for a significant re-rating is high. Eventually brokers start looking at these stocks as their market caps increase and the cycle of out-performance continues. The data below shows that small cap funds are far more likely to out-perform than large cap funds reflecting these significant inefficiencies at this end of the market.

“Wall Street research is focused on under 20% of publicly traded companies, those with market capitalisations of over $1.5bn. This leaves a large number of companies with scant analyst coverage. With few investment managers performing in-depth research on small cap firms and the rest relying on conventional research, an astounding number of small cap companies get overlooked. Focusing on this larger number of undiscovered companies increases the odds of uncovering hidden value.” First Wilshire

2. Better management access - In our experience smaller company management teams are generally more receptive towards engaging with investors than larger company management teams. The reason for this is simple: smaller company management teams are generally aiming to improve the markets’ understanding of their businesses, and often only have to deal with a few investors who are looking at their businesses. Smaller businesses often continue to be led by the founders, who are usually very passionate about the company and very keen to tell its story. However, if you are the CEO of a large cap like Telstra, your time is spread in so many directions it is simply impossible to build relationships with the 30 analysts following the company in addition to the many thousands of investors who are exposed to the company. This dynamic means smaller company investors are often privileged to get to know management which allows for a deeper understanding of the publicly available information.

3. Low correlation with the broader market - This is a benefit which is often ignored and misunderstood by the investment community. Smaller companies tend to do their own thing a lot more than larger companies reflecting: a) these businesses often have smaller market shares and/or operate in niche areas and are thus less likely to be affected by macro shifts, b) smaller companies are often trading at a significant discount to their large cap peers due to a lack of market awareness - this lack of awareness also protects their stock prices when their larger cap peers are selling off. The DMX Capital Partners fund has a correlation (R squared) since launch 17 months ago of only 17% with the All Ordinaries Index, and we expect it to remain low looking forward. The fund performs particularly strongly on a relative basis in weak market conditions for the reasons mentioned.

4. Simpler to analyse - Smaller companies are often simpler to analyse due to the focused nature of their business models. For example, when analysing SDI Ltd (ASX: SDI) investors need to be aware of the developments in one industry, the dental industry, and only need to model the company’s geographic segment analysis and the shift from amalgam to non-amalgam products. The depth of modelling required to understand a small company like SDI is of a completely different level to the intricate modelling required to understand a large and complex business like Telstra with its numerous operating divisions. We believe there is less room for error when working on relatively simple smaller company models.

5. Greater upside leverage given their generally lower starting market shares and lower cost structures - Most smaller companies we work on are aiming to increase their market shares from a relatively low starting position. Successful market share growth for smaller companies generally creates significant earnings and valuation upside over the long term. For example, a company starting with a market share of 1% with the objective of reaching a 5% market share in a growing market offers enormous growth potential. However, a larger company which already has a 40% market share will often be aiming to defend its market share from newcomers with the objective of growing in line with the market. In our experience the management psychology behind these two very different strategies is often at two ends of the spectrum. We would prefer to be investing in the aggressor rather than the defender. In addition, smaller companies, due to being capital constrained, are usually particularly focused on cost control and adopting a low cost operating structure. As their revenues grow there is an opportunity for significant operating leverage to drive strong bottom line growth.

“Smaller companies are often run by their founders or a small group of managers who are more motivated to increase shareholder value.” First Wilshire

On this point please refer to our recent article on investing in family companies: (VIEW LINK)

6. Focused investment cases which often provide direct exposure to a potent investment theme - As mentioned, smaller companies are generally far simpler business models than their larger cap peers which are often conglomerates with complex and sometimes contradictory stories. If you are factoring an investment theme into an investment decision, we believe it is a lot easier to get clean exposure to most themes in the smaller companies universe. For example, one investment theme we are aware of is the strong growth ahead for superannuations funds given Australia’s ageing society and dependence on future fund under management growth. Fiducian (ASX: FID) provides clean exposure to this theme given the company’s focused and simple business model. However, a larger cap peer like AMP does provide exposure to this theme but it is massively diluted by the company’s vast array of other businesses.

7. A larger investible universe - The maths of smaller company investing is interesting. If we look at the ASX, there are some 2,200 listed companies but most investors tend to regard the ASX100 or the ASX200 as the definition of the larger company universe. This means 80-90% of the listed universe are smaller companies. With such a large hunting ground for new ideas we believe the chances of success for disciplined smaller companies investors are higher.

8. More powerful investment risk management controls - Ultimately having better understanding of a business than the rest of the market is the strongest and most controllable risk control for any equity investment. As mentioned, gaining a deeper understanding of publicly available information on smaller companies than the rest of the market is generally achievable in our experience, and maintaining it requires consistent work, research, etc. Large cap investors generally don’t have this luxury due to the large number of competing analysts, and thus tend to control risk by focusing upon the standard deviations of returns, value at risk, etc. In our experience these risk controls are often backward-looking and involve far less direct control on the part of the investment manager. We believe smaller company investors have the clear advantage of being more in the driver’s seat when controlling stock specific and portfolio risk.

What makes a successful small cap investor?

Given these compelling reasons for long term smaller company out-performance, it seems natural to ask: what makes a successful small cap investor? Achieving out-sized returns in this sector are clearly not a given.

We believe there are 4 key attributes required to achieve long term investment success as a small cap investor:

1. Quality screening - In the 2000+ universe of ASX listed smaller companies we believe the vast majority do not qualify as high quality businesses. This means the first step to successful smaller company investing is to filter the high quality businesses into an invest-able bucket. This process takes many years of disciplined analysis of each business. At DMX our definition of quality means we are looking for companies with: high quality management, strong balance sheets, good visibility around future earnings, defendable and growing competitive moats, and well defined long term strategies. This may sound like a simple list but the reality is most companies do not tick all of these boxes. We believe less than 100 of the 2000+ universe of smaller companies actually meet our definition of high quality. This may sound surprisingly low but we would suggest this low hit rate is absolutely essential for DMX Capital Partners’ long term success.

2. A love of in-depth research - In our experience the key to understanding a business well is to “kick the tyres”, and really become aware of where the cashflows come from, why customers deal with this company, how management are thinking, etc. It takes a long time to properly understand a business and we believe this is key to maintaining a long term information edge versus the rest of the market.

3. Thinking long term - Successful smaller company investing requires a long term investment horizon in our experience. It is only by thinking about where these businesses will be in 5 years+ that the investment opportunities become clear. And it is only by remaining invested in these businesses for 5 years+ that our investors will benefit from our analysis. It takes time to build a small business into a larger business and it is this process which creates significant value for investors.

4. A focus on the fundamentals - Most investors who have been exposed to financial markets for many years would agree that there is a lot of noise in the markets. The media, other investors, etc will always present opposing viewpoints, and will look to create stories which sell or support their opinions. However, in our experience most of this is just noise which is best ignored. Successful smaller company investing requires an ability to filter the fundamental information from this noise.

CONCLUSION

DMX Capital Partners’ performance since launch is testimony to the attractions of smaller company investing. We believe the application of a disciplined value investing strategy to a filtered universe of high quality smaller companies provides a potent combination for long term out-performance. We will continue to exploit the significant market inefficiencies in the smaller company universe to our investors’ advantage.

Never miss an update

Enjoy this wire? Hit the ‘like’ button to let us know.

Stay up to date with my current content by

following me below and you’ll be notified every time I post a wire

DMX Asset Management Limited is an investment manager focussing on nano and micro-cap value opportunities on the ASX.

1 topic

DMX Asset Management Limited is an investment manager focussing on nano and micro-cap value opportunities on the ASX.

Expertise

DMX Asset Management Limited is an investment manager focussing on nano and micro-cap value opportunities on the ASX.

Expertise

Comments

Comments

Sign In or Join Free to comment

most popular

Investment Theme

If 24 LICs ran the Melbourne Cup, which ones would we back?

Affluence Funds Management

Equities

Buy Hold Sell: 5 ASX stayers built to go the distance

Livewire Markets