Why we stay ‘married’ to quality businesses

Last year saw a ‘junk rally’ in equity markets: higher quality businesses delivered generally weaker returns, while lower quality businesses did better. This made it hard for fund managers like us – who are wedded to the high-quality end of the market – to keep up with the benchmark. Is our adherence to quality, through thick and thin, the right approach? We think so, and the research bears this out.

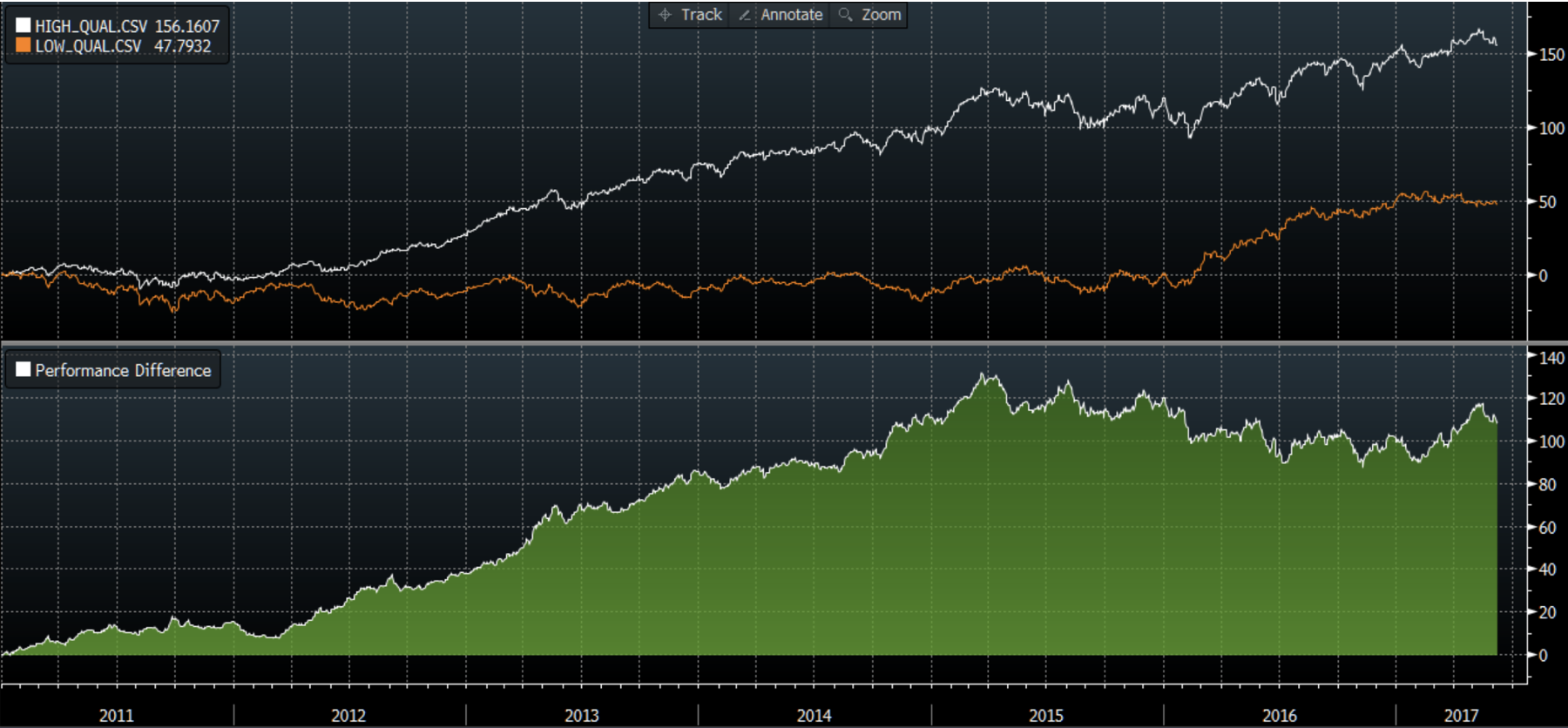

At Montgomery Investment Management we maintain a database that grades all the companies in our investment universe in terms of quality, and this allows us to construct some simple quality indices. In this example, a high-quality index made up of companies with above-average quality scores, equally-weighted, and a low-quality index made up of “other” companies, again, equally-weighted.

Using some of Bloomberg’s portfolio functionality, we can quickly map out the performance of these portfolios relative to one another over a reasonable stretch of time. This approach allows us to go back as far as 2011, and the chart below sets out the results.

You can see from the chart that over this period, the high-quality portfolio has done significantly better than the low-quality portfolio. However, you can also see a dip in that relative performance through 2016.

In this case we have divided companies into just two categories: “good” and “not good”. If we split them into more categories (eg “very good” vs “good”) the 2016 dip becomes more pronounced, but for this discussion we’ll keep it simple.

Before we move on, we should acknowledge that in the Australian market, a large part of the “not good” category is drawn from the resources sector. In our eyes, a commodity producer with no pricing power is hard to view as high quality, and in 2016 we saw a strong rally from the resources sector. While many investors would share our view on the quality of these companies, it is reasonable to ask whether the effect we saw in 2016 could be better characterised as a resources rally than a junk rally.

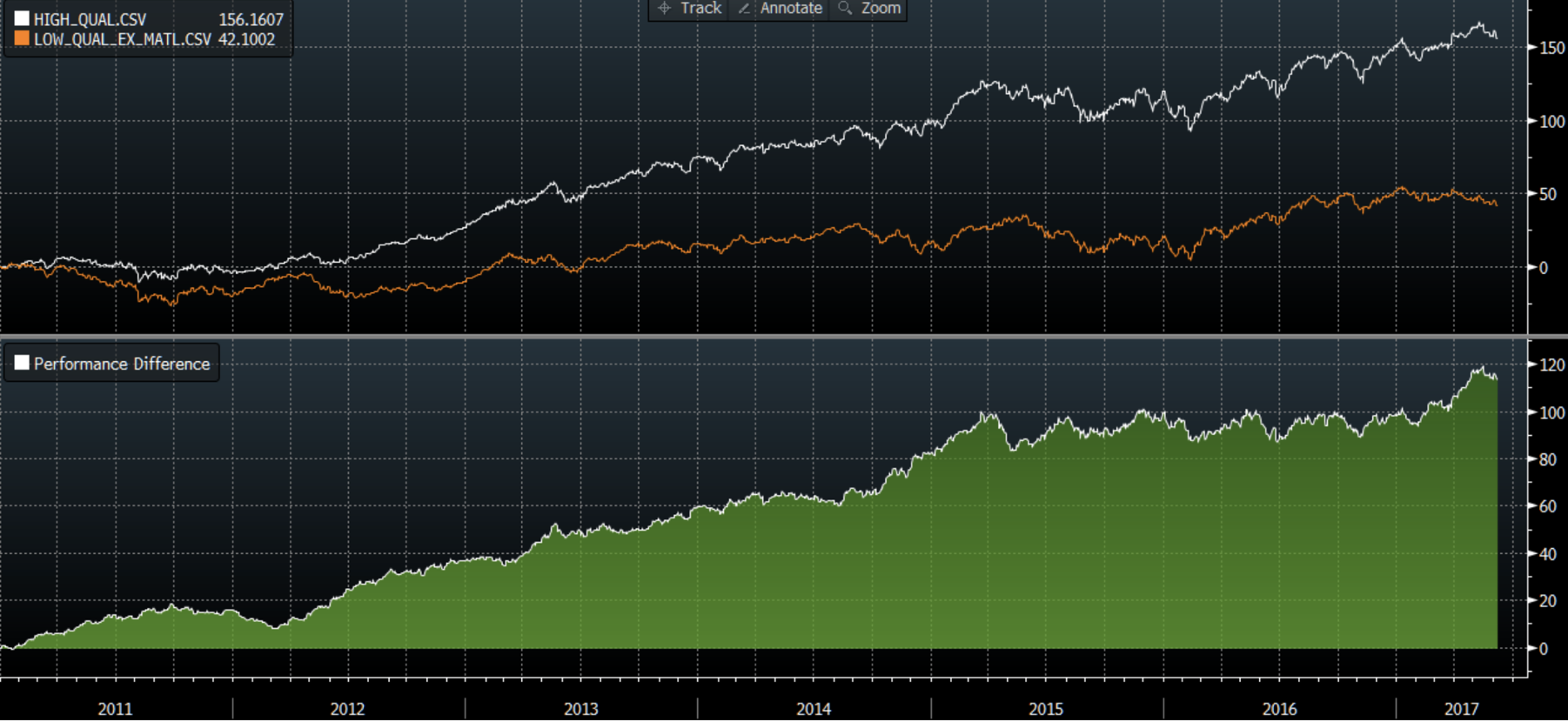

For completeness, below we repeat the analysis with materials companies removed from the low-quality portfolio. We see here that while quality took a break in 2016, it treaded water rather than going backwards, so it is reasonable to think that a lot of what we saw in 2016 was driven by the resources sector. Given that the Australian market has a heavy weighting to resources, this has a meaningful bearing on the performance of capitalisation-weighted index benchmarks.

So, what do we take away from this? To my mind there are several points worth making:

Firstly, quality has done well over a reasonable stretch of time, and this provides some support for fund managers wanting to focus on quality businesses. This view also sits comfortably with academic research covering longer periods of time and many different geographic markets.

Secondly, quality sometimes doesn’t perform. Again, this is consistent with the academic research. It’s also inevitable. If quality outperformed year in, year out, that would soon become obvious to all investors, and the long-term outperformance of quality would be competed away. In equity markets, there is no advantage in knowing something that everyone else knows.

This brings us to the question of whether we should always be invested in quality, or whether we should be willing to switch to the other side when we feel that a period of underperformance is imminent. The charts don’t help with this one, and we need to resort to some investment philosophy.

For MIM, quality is a cornerstone of our investment philosophy. We are effectively married to it, and the rationale goes like this:

We are confident that over long stretches of time, high-quality businesses will deliver good investment results. There is a wealth of empirical evidence and common sense that underpins this confidence.

We are much less confident that we could successfully and consistently time a switch between high-quality and low-quality. In our view, markets are extremely unpredictable over short periods of time, and any investment approach that requires such prediction is inherently uncertain.

This leads to a view that in switching out of quality when we think the time is right, we would be giving up a relatively certain long-term result to chase a rather less certain short-term result.

In markets that can be driven by short-term thinking, it’s easy to see the appeal of trying to time these cycles, but that is not what we do. Instead, we try to make clear to our investors that we are investing for the long term, and then we try to do what we know will work over that time frame.

For better, for worse.

Never miss an update

Enjoy this wire? Hit the ‘like’ button to let us know.

Stay up to date with my current content by

following me below and you’ll be notified every time I post a wire

Tim Kelley has retired from Montgomery Investment Management, effective 30 September 2021. Tim’s final project has been drafting our investment guidelines to integrate environmental, social and corporate governance (ESG) considerations into our investment process. Tim remains a shareholder of Montgomery Investment Management.

Tim Kelley has retired from Montgomery Investment Management, effective 30 September 2021. Tim’s final project has been drafting our investment guidelines to integrate environmental, social and corporate governance (ESG) considerations into our...

Expertise

Tim Kelley has retired from Montgomery Investment Management, effective 30 September 2021. Tim’s final project has been drafting our investment guidelines to integrate environmental, social and corporate governance (ESG) considerations into our...

Expertise

Comments

Comments

Sign In or Join Free to comment