Why WeWork works

The concept of flexible office space, or coworking, has been around for decades. It never garnered much attention, until the arrival of WeWork that is.

In just 7 years, WeWork has become a leader in the shared office industry and is reportedly one of the top five most valuable startups, worth a cool US 20 billion. Other than free beer and kombucha on tap, ping pong tables and yoga classes, what makes WeWork work? And how does its success affect commercial real estate investors?

Coworking office space now (left) and then (right).

Coworking office space now (left) and then (right).

The demand drivers for flexible office space are obvious. Flexibility comes first; business owners don’t want to be tied down by a big lease commitment, particular spaces and locations. They want the freedom to work where they are, with scope to grow if their business takes off.

Then they want to pay only for what they need – often a cool décor and vibe. And finally, they want to form networks and build a sense of community. WeWork and coworking spaces like it meet these exacting requirements.

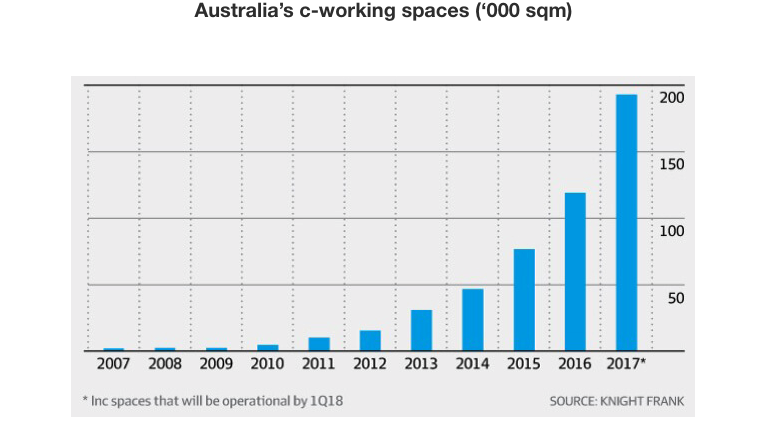

For commercial real estate investors, the growth of coworking has been a boon. According to Jones Lang Lasalle(1), between 2014 and 2017 coworking space has grown in the Asia-Pacific by nearly 36% a year. Europe and the United States experienced annual increases of over 20%. In fact, coworking operators were responsible for over 8% of gross leasing volumes in Asia Pacific last year, a trend likely to continue.

The Knight Frank chart below shows the growth in our market. It’s a similar story in other major financial centres; in Singapore coworking spaces drove around 20% of office demand last year according to Knight Frank and in London WeWork became the largest single office occupier in Central London.

How did this happen? Once upon a time coworking operators were viewed as competitors by office landlords, fighting over tenants. Not anymore. Traditional office landlords have realised they’re in a win-win situation. Not only is WeWork leasing a lot of space and attracting new occupiers to the office market, it is also driving landlords themselves to offer flexible workspace solutions to avoid being outpaced. And WeWork shows them how to do it.

Major Singapore office developers have been quick to catch on; Mapletree Investment’s version of coworking is called Coqoons, CapitaLand’s Flexi Suites, Keppel Land’s Kloud and Ascendas-Singbridge has thebridge.

Investa, one of Australia’s biggest office landlords, predicts that all its major buildings will have coworking spaces in the near future. Landlords now know they can only benefit by stepping up their collaborations with groups like WeWork. Both want to attract and retain tenants.

Coworking offerings will become a major drawcard for commercial buildings.

Only recently, commercial property naysayers were questioning the relevance of traditional workplaces as the ‘work-from-home’ trend took hold. Now that seems like foolish bandwagon jumping. Humans are innately social creatures and WeWork has tapped into this, mastering the art of ‘community building’.

Would I choose to work alone in my tiny, viewless home office surrounded by packing boxes from a move five years ago? No chance. The prospect of meaningful networking conversations over strawberry-infused water sounds like paradise in comparison. And it appears I am not alone.

Whether this makes WeWork worth $20bn is immaterial to commercial real estate investors. It’s hard to see how a company with little in the way of tangible assets can be worth more than the largest listed US office landlord, Boston Properties, with nearly 50 million square feet of prime office space in markets like New York and San Francisco. I know which I’d rather own.

That said, coworking operators, of which WeWork is one out of a long and growing list, have added tremendous value to the office market, to landlords and to commercial property investors like us. Even if WeWork is not the unicorn the market imagines it to be, office landlords are embracing the needs of the workplaces of the future and are ready to fill its flexible shoes and carry on. That makes the commercial office market in which we invest larger and with more options. And that must be a good thing.

(1) Spotting the opportunities: flexible space in Asia Pacific, Jones Lang Lasalle, 2017

Did you enjoy that?

click here.

Never miss an update

Enjoy this wire? Hit the ‘like’ button to let us know.

Stay up to date with my current content by

following me below and you’ll be notified every time I post a wire

Corrine joined APN Property Group as a Portfolio Manager for the Asian REIT Fund in February 2015. Corrine has over 15 years of experience in property and REIT investment in Australia, Asia and the North American markets.

Corrine joined APN Property Group as a Portfolio Manager for the Asian REIT Fund in February 2015. Corrine has over 15 years of experience in property and REIT investment in Australia, Asia and the North American markets.

Expertise

Corrine joined APN Property Group as a Portfolio Manager for the Asian REIT Fund in February 2015. Corrine has over 15 years of experience in property and REIT investment in Australia, Asia and the North American markets.

Expertise

Comments

Comments

Sign In or Join Free to comment

most popular

Investment Theme

Ross vs the AI hype: her shocking prediction revisited

Livewire Markets

Equities

Buy Hold Sell: 5 ASX stayers built to go the distance

Livewire Markets