Will the S&P 500 break out or be pushed back into its range?

Global equities eked out further gains last week, largely reflecting more vaccine hopes, good JP Morgan earnings and general relief that more widespread lockdowns were not re-imposed in the United States. Indeed, the tech-heavy NASDAQ actually slipped back last week while the S&P 500 gained, with a modest rotation into smalls caps and ‘value’ stocks.

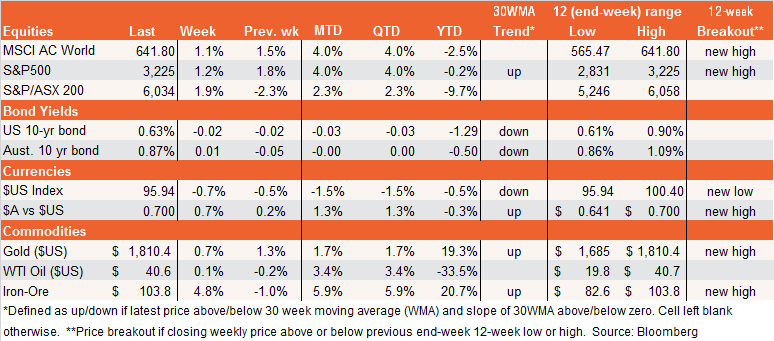

The S&P 500 ended the week at the top end of its 3,000-3,200 range since early July – to be down, unbelievably, only 4.7% from its mid-February all-time high. The obvious question this week is whether the market can break out or is pushed back into its range. The U.S. Q2 earnings reporting season rolls on this week, with 75 S&P 500 companies reporting, including IBM and Microsoft (day-trader plaything Tesla also reports on Wednesday!). We also get July PMI reports on manufacturing and services on Friday.

To my mind, however, the market is still of a view to dismiss most earnings and economic data weakness as ‘old news’ – neither the failure of U.S. weekly jobless claims to fall last week, nor the pullback in consumer sentiment caused much of a ripple.

Meanwhile, the market is quick to seize on any glimmer of good news – such as more hopeful vaccine trials or any U.S. corporation managing to report earnings slightly less horrible than expected. Also helping is the fact that bad news likely means the Fed will stimulate even further, with growing talk of the U.S. central bank promising to keep interest rates very low for a very long time.

Indeed, the only factor that seems capable of upsetting the market is lockdown news. In this regard, California imposed further restrictions last week, but stopped short of another full lockdown. And some U.S. states – with even worse virus breakouts – appear to be trialing greater use of face masks in public, as a mean of avoiding lock downs. Maybe face masks (which experts increasingly concede appear capable of at least slowing virus spread) could be a lockdown-avoiding game changer until such time as a vaccine arrives?

All up, even more important than earnings and economic data, how the virus continues to play out in America – and State/local government responses – remains the most critical factor for markets over the coming week.

Australian market

Local equities also managed to bounce last week despite Melbourne’s virus outbreak continuing to escalate. Local economic data was mixed, with a further encouraging rebound in employment over June as a whole (although the unemployment rate rose from 7.1% to 7.4% as more people re-entered the labour force) and a lift in the NAB measure of business conditions. That said, consumer confidence slipped back and the official fortnightly job tracker hinted the employment rebound may have stalled in the last two weeks of June.

The $A edged higher last week, helped by further gains in iron-ore prices as Chinese GDP data confirmed a solid Q2 economic bounce back. That said, Chinese retail spending for the month of June disappointed, highlighting the fact the world’s second largest economy is relying on good old-fashioned State-directed industrial projects rather than consumer spending.

The highlight this week will be the Federal Government’s budget update on Thursday, although some details of the extension of the JobKeeper program were released this morning. What’s clear is that Australia won’t face the ‘fiscal cliff’ that many fear, though somewhat less generous support will be likely in coming months – both due to budget concerns and to encourage those better-positioned businesses and workers to learn to walk on their own two feet again as early as possible.

Most critical of all, however, will be the the virus situation in NSW – and in particular whether it gets bad enough to force greater restrictions.

Never miss an insight

Each week I will publish my latest thoughts on the macro events shaping the ETF landscape. To be the first to read my insights, hit the follow button below.

Never miss an update

Enjoy this wire? Hit the ‘like’ button to let us know.

Stay up to date with my current content by

following me below and you’ll be notified every time I post a wire

Author, columnist, investment strategist and macro-economist. Previous roles at Federal Treasury, OECD, Macquarie Bank and AFR. I develop economic insights and portfolio construction strategies for BetaShares' retail and adviser clients.

5 topics

Author, columnist, investment strategist and macro-economist. Previous roles at Federal Treasury, OECD, Macquarie Bank and AFR. I develop economic insights and portfolio construction strategies for BetaShares' retail and adviser clients.

Author, columnist, investment strategist and macro-economist. Previous roles at Federal Treasury, OECD, Macquarie Bank and AFR. I develop economic insights and portfolio construction strategies for BetaShares' retail and adviser clients.

Comments

Comments

Sign In or Join Free to comment