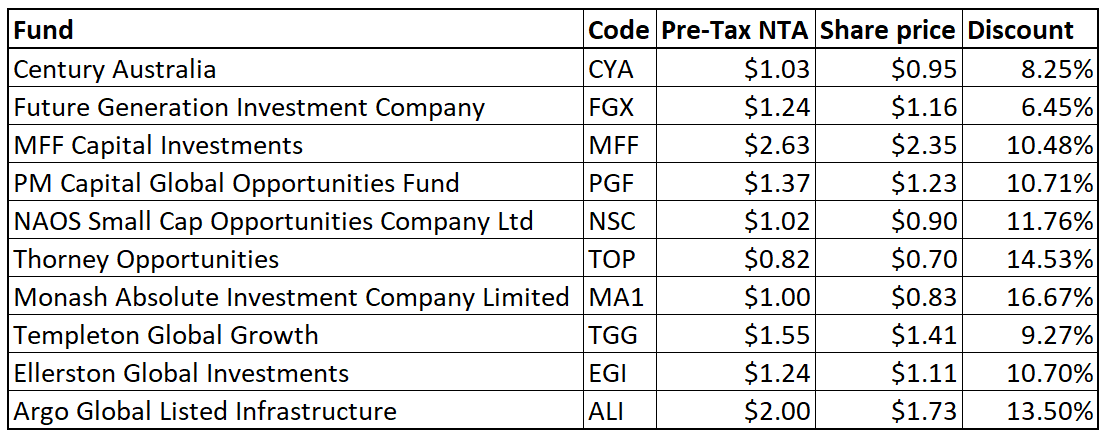

10 LICs trading at a discount

There are a range of brokers and researchers who produce regularly monthly or quarterly updates on the LIC sector. While the quality and depth of the research available is excellent, providing complete coverage of over 100 companies and trusts takes can take several weeks.

The LICs presented below are not an exhaustive list, but the information is as up-to-date as possible, with the last of the net tangible assets (NTA) updates referenced here being released to the ASX Wednesday night.

Below you’ll find a table of the share prices, NTA, and discounts of the funds, followed by some comments on each of the managers.

Century Australia (CYA)

This old LIC has been given a new lease on life since the management was taken over by Wilson Asset Management in April last year. While the majority of LICs managed by the team at WAM trade at a premium to NTA, Century maintains a reasonable discount of 8%. Performance has been solid, with CYA outperforming the ASX300 Accumulation Index by 4.5% since the appointment of the new manager in April 2017.

While many LICs carry a liability for tax on unrealised gains, the poor performance of the previous manager has left this company with significant carry forward losses. This means that the post-tax NTA is actually higher than the pre-tax NTA. As a result, the level of fully franked dividends that CYA can pay is currently reliant on the franked dividend income received from the underlying companies in the portfolio. CYA recently announced a fully franked interim dividend based on the franking credits available.

Future Generation Investment Company (FGX)

Unlike the other LICs in this list, Future Generation is not managed by a single firm. Instead, the investment committee has selected a list of some of Australia’s best performing fund managers, many of whom are inaccessible to retail investors.

The Company exists for the dual purposes of providing returns to shareholders, while providing a stable stream of funding to Australian children’s charities. For this reason, all the fund managers and service providers (including Livewire) waive their fees and costs. Instead of paying fees, the fund donates 1% of the assets per annum to a selection of charities.

Since inception in September 2014, Future Generation has outperformed its benchmark by 3.3%, and has managed to do so with significantly less volatility than the broader market.

MFF Capital Investments (MFF)

This company was formerly known as the Magellan Flagship Fund and is managed by Magellan co-founder Chris Mackay. This was the first pool of capital raised by Hamish Douglass and Mackay when they launched Magellan. Though their duties are separated these days, the relationship between Mackay and Douglass remains “extremely strong.”

Frustratingly, the company does not disclose its long-term performance against a benchmark. According to Independent Investment Research’s last update, it had produced a portfolio return of 21.8% p.a. over the five years to the end of December 2017. For comparison, the Magellan Global Fund produced a return of 18.4%, while competitor Platinum Capital returned 16.3% over the same period.

PM Capital Global Opportunities Fund (PGF)

With over 30 years working as an investor, you’d be hard pressed to find a portfolio manager on this list with more experience than Paul Moore. The bottom-up strategy is focussed on long-term global thematics such as the consolidation of brewing companies or the post-GFC housing recovery.

PGF’s investment strategy is based on the same philosophy and process as PM Capital’s Global Companies Fund, which was recently the best performing strategy in its category over 1, 3, 5, 7, and 8 years according to Morningstar.

The company has traded at an average discount of around 13% since listing, but this has begun to narrow in the last year after a period of strong portfolio performance.

NAOS Small Cap Opportunities Company Ltd (NSC)

This is another example of an older LIC with a new fund manager taking the reins. NAOS is a small-cap specialist with a solid track record of performance. Their other two LICs have outperformed their benchmarks by 12.01% and 13.85% since inception.

This LIC was previously Contango Microcap Limited, but management was transferred to NAOS late last year. The portfolio looks quite different to many ASX small cap funds, with financials and healthcare featuring heavily, while technology and materials are not significant exposures. Some holdings include Over The Wire Holdings, Australian Ethical Investment, and MNF Group.

Thorney Opportunities Limited (TOP)

This LIC is the brain-child of billionaire investor, Alex Waislitz. Though the listed company was launched in 2013, Waislitz has been managing money since the early 90s. The board of directors is truly impressive. Apart from Waislitz, it includes Ellerston Capital’s CIO, Ashok Jacob; Chairman of Ardent Leisure and Estia Health, Dr Gary Weiss; and Henry Lanzer AM, Managing Partner of one of Australia’s top law firms, Arnold Bloch Leibler.

The firm doesn’t provide up-to-date performance figures, however, they do provide plenty of detail on their major holdings. These include AMA Group, OneVue Holdings, and iSelect.

Monash Absolute Investment Company (MA1)

Monash Investors Limited Principals and Portfolio Managers, Simon Shields and Shane Fitzgerald, have been working together since 2011. Shields was formerly the Head of Australian Equities at UBS, where Fitzgerald was a Director and Investment Analyst. In 2012 they left UBS to start Monash Investors, which had strong initial performance.

Unfortunately for both the firm and investors, the strategy experienced a period of underperformance soon after the company was listed. More recently, performance has been improving. A recent presentation shows that the underlying strategy returned 13.75% for the FYTD, as at the end of February.

In the most recent update, the company commented on the performance and discount:

- “Based on data from Macquarie Wealth Management Research, the performance of the NTA over the last year placed MA1 as one of the highest returning Australian Equity LICs.

- Despite this, the MA1 discount, to NTA remains one of the largest in the market at around 16% despite there no longer being any options on issue.”

Templeton Global Growth (TGG)

This is one of the oldest LICs on the ASX, having first listed in 1987. The company is managed by Franklin Templeton Investments, which has existed for more than 60 years and manages nearly a trillion AUD worth of assets. It’s had a mixed record of performance in recent years; it’s one and five-year performance figures are strong, while the two and three-year numbers are well below its benchmark.

Despite the "growth" in the name, the fund appears to be skewed toward a value style. Its latest presentation emphasises the lack of value globally, and highlights the lower average price to book ratio of the company's portfolio relative to its index. It's encouraging to see that the board considers closing the discount to NTA a priority.

Ellerston Global Investments (EGI)

While most global fund managers tend to focus on the large-to-mega-cap universe, EGI’s focus is on the small-to-mid-cap space. Despite this, you’ll find a range of themes in the portfolio that will be familiar to investors in larger cap funds.

One interesting observation is that the last of the attached EGI options expire in April. As Dominic McCormick explained in a recent article, the expiry of these options can be indicative of a buying opportunity.

I sat down with Portfolio Manager, Arik Star, for a recent episode of The Rules of Investing. Check it out if you’re interested in learning more about the strategy and how he thinks.

Argo Global Listed Infrastructure Limited (ALI)

ALI was launched in 2015 to considerable fanfare. Cohen and Steers, the portfolio manager for the strategy, has a long history of successfully managing listed real assets. However, performance has been hard to come by for the vehicle since listing. Even now, nearly three years later, the company is trading below its initial issue price.

If listed infrastructure is what you’re looking for however, it’s one of only a small handful of options on the ASX. The pedigree of Cohen and Steers, including the more than AU$70 billion of funds that it manages globally, suggest that a reversion to mean is possible here.

Notice: This article contains general information only, it does not constitute advice to trade in any of the securities mentioned. Investors should seek professional financial advice before making decisions to invest.

The author holds long positions in both Future Generation Investment Company (FGX) and PM Capital Global Opportunities Fund (PGF).

Livewire Markets is a service provider to Future Generation Investment Company, these services are provided free of charge.

Never miss an update

Enjoy this wire? Hit the ‘like’ button to let us know.

Stay up to date with my current content by

following me below and you’ll be notified every time I post a wire

Patrick is the founder and director of PLP Finance Media, a content production and strategy consulting agency specialising in investment content and communications. He also writes for A Rich Life.

Patrick was a Market Analyst, Editor, Senior Editor, and Managing Editor at Livewire Markets between 2015 and 2022. He was the Content Director and a member of the Investment Strategy & Research Group at Betashares between 2022 and 2024. He is an expert on listed products, commodities, and investment strategy, with a particular interest in gold and uranium,.

1 topic

8 stocks mentioned

3 contributors mentioned

Patrick is the founder and director of PLP Finance Media, a content production and strategy consulting agency specialising in investment content and communications. He also writes for A Rich Life. Patrick was a Market Analyst, Editor, Senior...

Expertise

Patrick is the founder and director of PLP Finance Media, a content production and strategy consulting agency specialising in investment content and communications. He also writes for A Rich Life. Patrick was a Market Analyst, Editor, Senior...

Expertise

Comments

Comments

Sign In or Join Free to comment