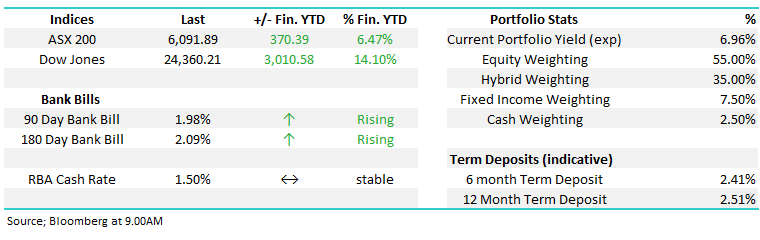

3 overvalued yield stocks (WOW, TCL, BWP)

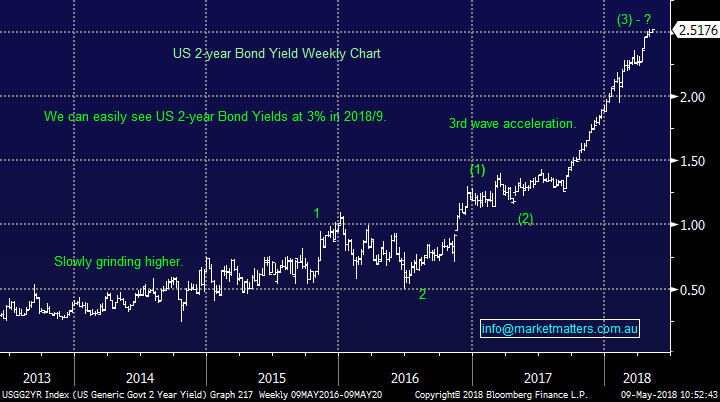

Global interest rates are rising after a multi decade decline in US Bond Yields and recently we saw interest rates / bond yields rally above those on offer by stocks, a fairly new phenomenon to many players in today’s market although it’s definitely not yet occurring in Australia. The US S&P500 is yielding around 2% pa whereas US bond yields have now risen clearly above that on offer from stocks i.e. 2-years at 2.51% and 10-years just under 2.99%.

In Australia the dividend yield on the ASX 200 sits at 4.50% while our 2 years are at 2.02% and our 10 years are around 2.78%, clearly more attractive from yield hungry investors. Historically, rising interest rates don’t have a negative impact on stock markets in a general sense given rising rates are usually underpinned by stronger economic growth and company profits, but with yields being so low for so long, we believe it’s very likely this could cause a psychological shift in investor sentiment, especially considering the magnitude of the rally in stocks during this cycle. More specifically though for income investors, expensive yield stocks will likely feel the brunt of any interest rate led sell off in the market. All this makes for a difficult outlook for yield trades and bond proxies like TCL.

From a timing perspective, we doubt this will happen immediately given the market is now incredibly focussed on this theme with short US bonds (a trade positioned for higher yields) one of the most crowded which implies to us a rest / pullback is close at hand.

US 2-year Bond Yields Chart

US 10-year Bond Yields Chart

3 overvalued yield stocks

Woolworths (WOW) $28.55 – expected yield of 3.15% FF

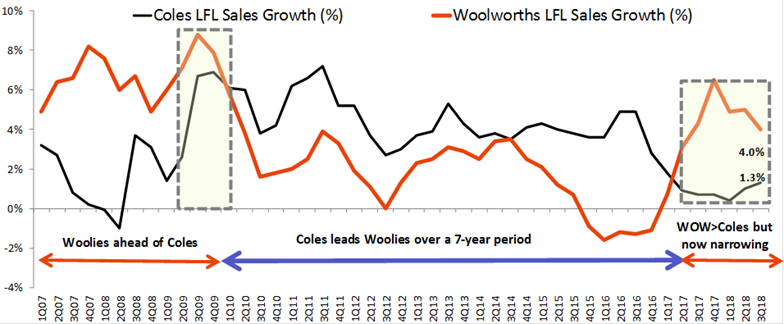

The iconic local supermarket ‘Woolies’ has seen its share price rally from the low $20’s to the high $20’s over the past 12 months , wrestling back its dominance over Coles which it had lost for 7 long years. Looking at like for like sales growth below, there have been ebbs and flows but overall a big turnaround from Woolies since the start of 2017 – however that momentum is now starting to soften.

Like for Like sales growth – Coles v Woolies

Source; Shaw and Partners

In the past month, the WOW share price has rallied around 8% pushing up through $28.00, with the Supermarket now trading on a forward PE based on consensus earnings of 22.4x - making WOW the world’s most expensive Supermarket. Looking at international comparables highlights this fact nicely. i.e Carrefour 16.8x, Sainsbury 14.3x, Kroger 11.5x, Tesco 17.3x, Walmart 17.5x, Morrison’s 18.7x, Casino Guichard 15.5x, WES 18.2x and MTS 16.1x

Now looking at WOW versus the market, it’s trading at a 45% premium to the market multiple (15.5x) yet delivering only 4-9% earnings growth in FY19. Although the certainty / stability of earnings is a key contributor to the current valuation, the PE is too high in our view particularly given the competitive landscape is changing and will likely become far more aggressive especially from Coles, and ALDI, Costco, IGA, AMZN, Kaufland and potentially Lidl.

The other factors supporting the view is margins, which are extremely high in Australia which in itself will entice competition however the biggest near term threat to Woolies is the demerger of Coles in 2019. We’re cynical investors so it’s hard not to think that Coles will do everything in their power between now and then to list with very good momentum – which we started to see in the recent quarterly sales update.

We are negative Woolworths at current levels targeting a move down to $25.00 i.e ~10% lower

Woolworths (WOW) Chart

Transurban (TCL) $12.01 - expected yield of 4.53% unfranked

Transurban (TCL), the incredibility well run toll road operator had an investor day at the end of April and talked a big game, and rightly so, the underlying performance of this business has been exceptionally strong with quality assets that are growing earnings at a pace greater than inflation, plus they have the ability to ‘manufacture’ future growth through their development pipeline.

To be clear, we have no issues with the underlying business in fact, this is one of those ‘Buffet like’ stocks that have great long life assets that are hard to replicate, however rising global interest rates coupled with the likelihood of a growing development pipeline and Transurban, a stock that is priced principally off yield could be hit from two sides.

Lower dividend growth than is currently factored in (given requirement to spend on growth) and a macro backdrop of rising interest rates that make the prevailing dividend less attractive. As it stands, Transurban has an ~$11bn development pipeline, with the potential for this to grow significantly, e.g. Wesconnex at around $16.8bn, North East Link at $16.5bn and Maryland in the US around US$9.0bn.

We are negative Transurban (TCL) at current levels targeting a move down to $10 i.e ~20% lower

Transurban (TCL) Chart

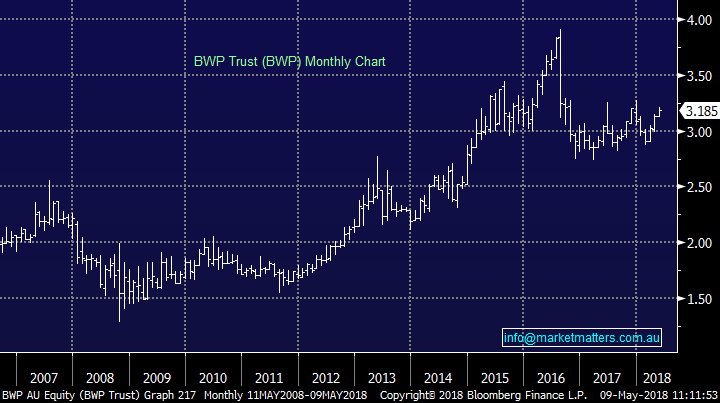

BWP Trust (BWP) - expected yield of 5.57% unfranked

April was a good month for property stocks, with the sector outperforming the strong move in the broader market (+4.5% vs. +3.9%) even though global interest rates also tracked higher through the period – the US 10 year yield cracking 3%. Higher rates are generally a headwind for property prices and therefore an impediment to property stocks. BWP manages commercial property – has about 80 investments spread geographically around Australia with Bunnings Warehouses one of the main tenants (but they also have others).

This is a very well run property company with a well performing primary tenant. That said, it’s expensive trading at an 11% premium to its NTA which sits at $2.82. While the sector collectively trades at a 21% premium to NTA, this is skewed by companies that have funds management businesses and / or other areas of earnings. BWP does not, and in our view the stock screen ‘expensive’ relative to other sector players – Vicinity (VCX) for instance which trades at a -17% discount to NTA .

We are negative BWP at current levels targeting a move to $2.50 i.e ~ 20% lower

BWP Trust Chart

To get our latest market views and hear when we take new positions, trial Market Matters for 14 days at no cost by clicking here.

Have a great day

James & the Market Matters Team

Disclosure

Market Matters may hold stocks mentioned in this report. Subscribers can view a full list of holdings on the website by clicking here. Positions are updated each Friday, or after the session when positions are traded.

Never miss an update

Enjoy this wire? Hit the ‘like’ button to let us know.

Stay up to date with my current content by

following me below and you’ll be notified every time I post a wire

James is the Lead Portfolio Manager & primary author at Market Matters, a digital advice & investment platform with over 2500 members that offers real market intel & portfolios open for investment. He is also a Senior Portfolio Manager at Shaw and Partners heading up a team that manages direct domestic and international equity & fixed-income portfolios for wholesale investors.

3 stocks mentioned

James is the Lead Portfolio Manager & primary author at Market Matters, a digital advice & investment platform with over 2500 members that offers real market intel & portfolios open for investment. He is also a Senior Portfolio Manager at Shaw and...

Expertise

James is the Lead Portfolio Manager & primary author at Market Matters, a digital advice & investment platform with over 2500 members that offers real market intel & portfolios open for investment. He is also a Senior Portfolio Manager at Shaw and...

Expertise

Comments

Comments

Sign In or Join Free to comment

most popular

Equities

High conviction: What we’re backing for the long term

Livewire Markets