Three factors that influence company performance

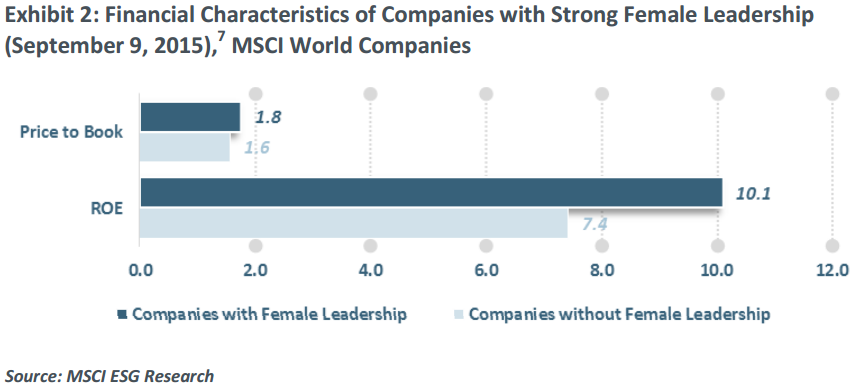

Assessing management is one of the more difficult tasks investors face. In recent years, research has identified three quantifiable factors that influence company performance: CEO remuneration, gender equality at a board/executive level, and family/founder ownership. Global index provider MSCI recently released a report stating that “companies with lower total summary CEO pay levels, more consistently displayed higher long-term investment returns.” MSCI also stated last year that “companies in the MSCI World Index with strong female leadership generated a ROE of 10.1% per year, versus 7.4% for those without.” Research from Pitcairn Financial Group, a leading US-based family office, then demonstrated that “family-owned firms within the S&P 500 index annually returned ~135 basis points more than the broad market over a 20-year period.” Read on for a deeper understanding of what’s driving each of these observations.

Factor 1 – Executive Pay

Intuition would suggest that Executive remuneration would be correlated to share price performance. However, research has shown the opposite to be true. According to MSCI’s report titled: “Are CEOs Paid for Performance?”:

“Companies that awarded their Chief Executive Officers (CEOs) higher equity incentives had below-median returns based on a sample of 429 large-cap U.S. companies observed from 2006 to 2015. On a 10-year cumulative basis, total shareholder returns of those companies whose total summary pay (the level that must be disclosed in the summary tables of proxy statements) was below their sector median outperformed those companies where pay exceeded the sector median by as much as 39% … The highest paid had the worst performance by a significant margin. It just argues for the equity portion of CEO pay to be more conservative.”

Dr. Kym Sheehan wrote her Ph.D. thesis on executive pay and is the Founder of The Executive Remuneration Reporter, which analyses and advises on remuneration-related resolutions. In response to the paper, she told Livewire that it’s important to look deeper than the reported numbers.

“When looking at Executive pay, investors need to focus on the following:

- What the remuneration opportunity is. E.g.: fixed remuneration + maximum short term incentive (STI) opportunity + size of long term incentive (LTI) grant;

- The performance measures. What does the executive have to do to earn the maximum STI opportunity, and for the LTI grant to vest;

- What the outcomes are in any given year.”

“With performance measures, investors need to understand how these items are measured (statutory or underlying basis) and whether the values used for remuneration are adjusted further from the numbers reported generally by the company (including the underlying numbers reported in its results presentations). A clear example of a company that does this is Newcrest Mining.”

Nicholas Moore from Macquarie Group is the highest paid CEO in Australia, based on his total actual remuneration due to an uncapped short-term incentive scheme.

Dr. Sheehan has kindly prepared a summary of the Executive pay of five outperformers (Commonwealth Bank of Australia, CSL, Ramsay Health Care, Sydney Airport and Transurban), and five underperformers (BHP Billiton Limited, National Australian Bank, Origin Energy, QBE Insurance and Woodside Petroleum) based on total shareholder return, over the past five years.

[high flyers and underperformers - CEO pay FY2011-FY2015 prepared for LIVEWIRE MARKETS 12 AUGUST 2016.pdf]

Factor 2 - Gender diversity

Corinne Post and Kris Byron, from Lehigh University and Georgia State University respectively, performed a meta-analysis of 140 studies on gender diversity at a board level. They found: “female board representation is positively related to accounting returns and that this relationship is more positive in countries with stronger shareholder protections.”

Contrary to a common conception that female board members are too conservative, MSCI found no “strong evidence that having more women in board positions indicate greater risk aversion.”

MSCI defines a company as having ‘strong female leadership’ if:

“the company’s board has three or more women or if its percentage of women on the board is above its country average. A company is also considered to have ‘strong female leadership’ if it has a female CEO and at least one woman on the board.”

Despite making up half the population, women make up less than a quarter of board positions among ASX 200 companies, according to the Australian Institute of Company Directors.

Factor 3 – Founder/family ownership

Research from industry groups and multiple universities have suggested that companies where the founder or founding family retains significant ownership perform better over a number of metrics.

A 2003 study by Ronald Anderson and David Reeb found that companies with family members as CEO perform better than those without (our emphasis added):

“Additional analysis reveals that the relation between family holdings and firm performance is nonlinear and that when family members serve as CEO, performance is better than with outside CEOs. Overall, our results are inconsistent with the hypothesis that minority shareholders are adversely affected by family ownership, suggesting that family ownership is an effective organizational structure.”

Additionally, research at Purdue University suggested that companies with a founder CEO were significantly more innovative:

“Our main results show that the existence of a founder CEO is correlated with a 31 percent increase in the citation-weighted patent count before we control for R&D spending and a 23 percent increase in the citation-weighted patent count after we control for R&D spending, suggesting that founder CEOs are more effective and efficient innovators than professional CEOs. As boundary conditions of the relationship, we find that the positive effect of founder CEOs on innovation is stronger in more competitive and innovative industries. Furthermore, our results suggest that founder CEOs are more likely to take their firms in a new technological direction. Finally, we provide evidence that the innovations of founder CEO-managed firms create more financial value than the innovations of professional CEO-managed firms. Our findings are particularly convincing because the results are consistent across various robustness checks that control for potential selection issues and other endogeneity concerns.” – Lee, Kim & Bae, Purdue University.

Special thanks to Dr. Kym Sheehan for her contributions to this article. You can view her Livewire profile here: (VIEW LINK)

Further reading:

Access the MSCI paper "Are CEOs Paid For Performance?" here: (VIEW LINK)

Access the MSCI paper "Women on Boards" here: (VIEW LINK)

Never miss an update

Enjoy this wire? Hit the ‘like’ button to let us know.

Stay up to date with my current content by

following me below and you’ll be notified every time I post a wire

Livewire Exclusive brings you exclusive content from a wide range of leading fund managers and investment professionals.

4 topics

Livewire Markets

Livewire Exclusive brings you exclusive content from a wide range of leading fund managers and investment professionals.

Expertise

Livewire Markets

Livewire Exclusive brings you exclusive content from a wide range of leading fund managers and investment professionals.

Expertise

Comments

Comments

Sign In or Join Free to comment

most popular

Equities

What a 40% year taught us: 4 lessons from the past 12 months (and 3 new stocks to buy)

Seneca Financial Solutions

Equities

How to invest $100k for growth

Livewire Markets