4 reasons to consider currency hedging your global investments

Unlike investing in local shares and property, investors considering exposure to international shares and commodities face the decision of whether to hedge the associated foreign currency exposure.

All else constant, if you are bullish on a global investment exposure but also bullish on the Australian dollar, it makes sense to seek a currency-hedged exposure if available, as otherwise your potential returns will be diminished by a fall in the value of your investment in Australian dollar terms when it comes time to sell and convert back into our local currency. By contrast, if you are bearish on the Australian dollar, it makes sense to consider an unhedged exposure if available.

And of course, for a number of investors, currency hedging can be used as a simple way to remove an additional element of uncertainty in investment returns – and investing in this way means that investors do not have to concern themselves with the impact of often volatile currency fluctuations.

For more detail on how currency moves affect hedged vs unhedged investment returns, please see the technical appendix below.

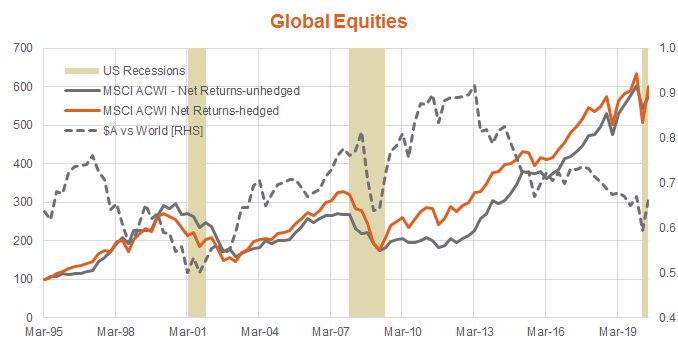

Hedged vs. unhedged global investments over time

The chart below details the historical returns from global equities on both a hedged and an unhedged basis – along with the value of the $A against a basket of global currencies of countries within the global equity index.

Source: Bloomberg. Past performance is not an indicator of future performance.

As evident, over the past 25 years at least, the $A has experienced marked cycles of appreciation and depreciation around a generally flat underlying trend. As a result, the returns from global equities over this long period have been broadly similar on a hedged and unhedged basis (both around 7.5% p.a.).

On this basis alone, and provided the $A remains in a long-run flat trend against other global currencies, there is not a clear cut long-term case to hedge or leave unhedged broad long-term exposure to global equities.

That said, over medium-term time periods, it’s also evident that the $A can sometimes be either positively or negatively correlated with global equity bull market periods. In the late 1990s – and again since around early 2013 to the present – the $A tended to fall even as global equities rose – boosting returns from the latter in unhedged terms. Between 2001 and 2013, however, the $A tended to rise with the rise in global equities, meaning investors would have been better off with hedged global investment exposures.

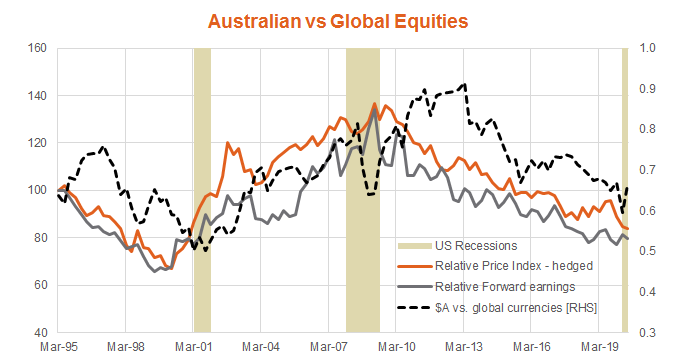

What causes these shifting correlations between the $A and global equities?

In essence, as evident in the chart below, it appears to reflect whether the drivers of global economic growth and equity market performance tend to favour relative performance of Australian corporate earnings and equity prices. Technology booms – as in the late 1990s and much of the past decade, have tended to undermine relative Australian equity and currency performance – which in turn has favoured international investing on unhedged terms. By contrast, commodity booms, as evident in the decade after the Dotcom bust, have tended to boost relative Australian equity and currency performance – which has favoured hedging exposure to international equities.

Source: Bloomberg. MSCI ACWI vs. S&P/ASX 200 Index. Past performance is not an indicator of future performance.

Last but not least, a final feature of the $A and global equity relationship is worth pointing out.

Over the very short-run (say over a few months) the correlation between the $A and global equities tends to be positive – as both are considered ‘risk-on’ assets that move together in line with the ebb and flow of short-run global investor sentiment. What’s more, this positive correlation is especially evident during major ‘risk-off’ periods or global equity bear markets.

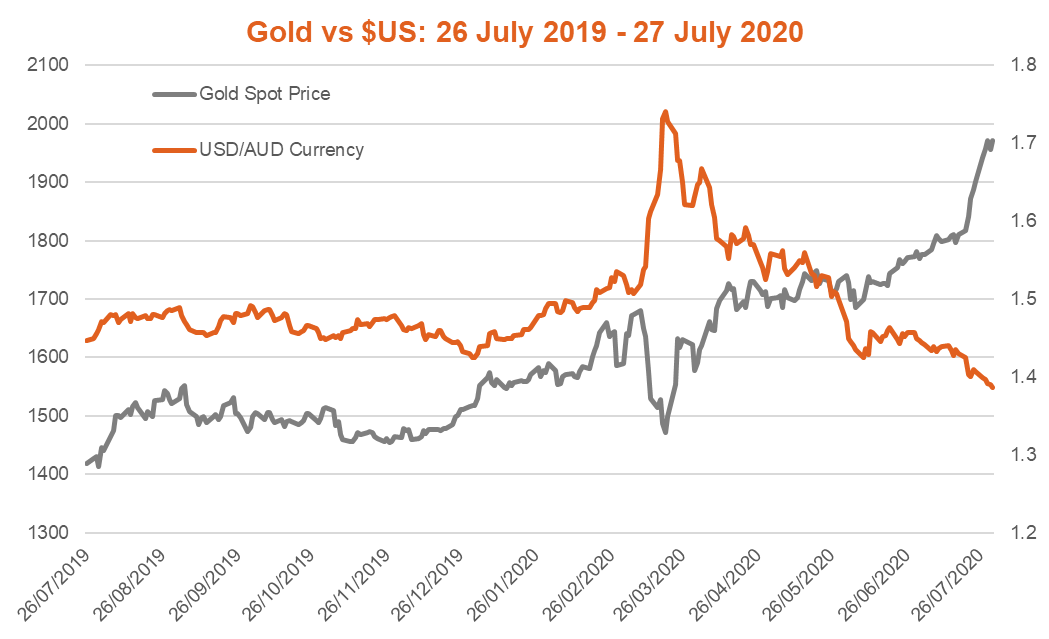

Risk-on? Why hedging may make particular sense today

The past few months of “risk-on” market behaviour has again demonstrated some of the benefits of hedging at the right times. As seen in the chart below, the U.S. Federal Reserve’s extreme monetary stimulus has helped weaken the $US versus the $A, whilst at the same time helping to push up gold prices.

Source: Bloomberg.

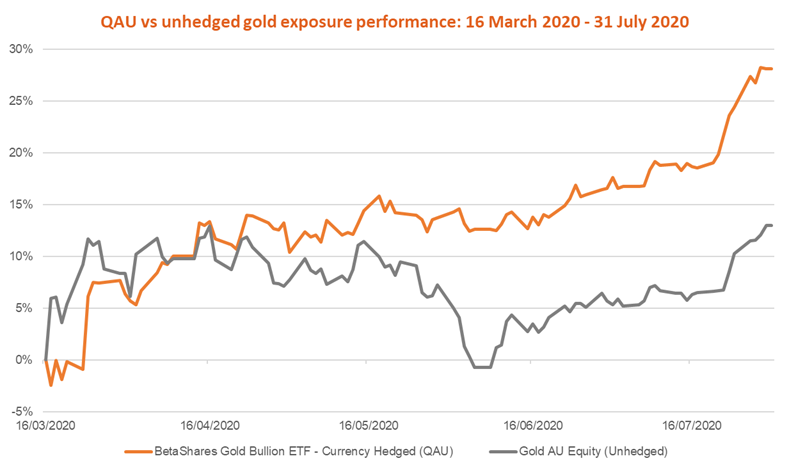

As a result, a hedged gold bullion exposure, such as through the BetaShares Gold Bullion ETF – Currency Hedged (QAU), has performed a lot better than an unhedged gold exposure.

Source: Bloomberg. Past performance is not indicative of future performance.

The same is true of hedged exposure to global equities, such as via the Nasdaq-100.

In short, in a period when the U.S. Federal Reserve is providing extreme monetary stimulus – which in turn is helping weaken the $US – it could well make sense to hedge exposure to global investments (such as gold and equities) likely to do well in this environment.

Bottom line: Four reasons to consider currency hedging

Against this background, in our view there are four reasons an investor might consider currency hedging, at least on occasion:

- As a medium-term investor, you think the next equity-up cycle will be one in which the $A will also strengthen, perhaps reflecting a shift in global economic drivers from, say, disinflationary technology disruption, to a more inflation/commodity-driven boom (perhaps reflecting ongoing extreme global monetary stimulus).

- As shorter-term investor, you think current risk-on sentiment will persist, which will push both equities and the $A higher – so you want to hedge your favoured global trades (such as gold and the Nasdaq-100) to avoid limiting some of your gains through exchange rate loss.

- As either a short or long-run technical trader, you want to base entry and exit into certain global exposures using specific price level or price performance indicators, and don’t want these signals distorted by currency movements.

- As an investor, you simply have no idea as to which way the $A will move over either the short or long term. In this case, you may choose to simply ‘take currency out of the equation’ by focusing on only hedged exposures, or by splitting your exposures into both hedged and non-hedged positions.

Hedge your exposure

To provide investors even greater choice in terms of how they gain exposure to international markets, BetaShares recently launched a range of currency hedged ETFs to complement the exposures that are already available on an unhedged basis. To find out more, please visit our website.

Never miss an update

Enjoy this wire? Hit the ‘like’ button to let us know.

Stay up to date with my current content by

following me below and you’ll be notified every time I post a wire

Author, columnist, investment strategist and macro-economist. Previous roles at Federal Treasury, OECD, Macquarie Bank and AFR. I develop economic insights and portfolio construction strategies for BetaShares' retail and adviser clients.

Featuring

David Bassanese,

Betashares

Author, columnist, investment strategist and macro-economist. Previous roles at Federal Treasury, OECD, Macquarie Bank and AFR. I develop economic insights and portfolio construction strategies for BetaShares' retail and adviser clients.

2 topics

5 stocks mentioned

Author, columnist, investment strategist and macro-economist. Previous roles at Federal Treasury, OECD, Macquarie Bank and AFR. I develop economic insights and portfolio construction strategies for BetaShares' retail and adviser clients.

Comments

Comments

Sign In or Join Free to comment