4 ways to handle a stock market crash

Scott Shuttleworth

Vega Capital

As Peter Lynch once famously said “You get recessions, you have stock market declines. If you don’t understand that’s going to happen, then you’re not ready, you won’t do well in the markets”. Today I’m going to discuss some ways in which investors can protect their portfolios from downside risk.

We employ almost all of these methods at The Vega Fund.

Diversification

Investors can reduce downside exposure (particularly from idiosyncratic risk) by being diversified across individual stocks and sectors. This is particularly important for investors with little time to research industries and individual stocks since idiosyncratic risks are best monitored by professionals who can do so on a continuous basis.

During a recession however, diversification amongst stocks is unlikely enough to protect from falls in prices. This is where diversification amongst negatively correlated asset classes can help.

Negatively correlated assets

An asset having negative correlation with respect to stocks simply means that when the price of said stocks fall, the price for this asset will rise. One example of this is a put option which will increase in value as the underlying stock it’s written on falls in price.

However you don’t necessarily need to pay for a put in order to have downside protection. An investor could sell a call option, effectively selling some upside in their investment to hedge some downside risk.

Other alternatives involve buying a VIX future contract. Typically during a correction or recession, stock price volatility will spike. Since the VIX future contract is linked to stock price volatility (via the implied volatility of options), it will increase in value during a negative market event.

By introducing negatively correlated assets into our portfolio, we're effectively hedging said portfolio. We can improve the effectiveness of our hedging by increasing the number of hedges we hold as stock prices rise and reduce them as stock prices fall. Since hedges are typically cheaper in rising markets and more expensive in falling markets, we end up buying our hedges at a low price and selling them at a higher price. As such, we can actually both protect our portfolio and earn returns over time.

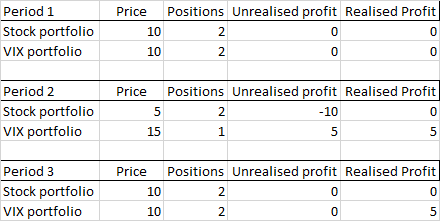

In the below we've attempted to show this as an example. We start in period 1 with our portfolio - 2 units of stocks and 2 units of VIX.

In period 2, stock prices fall by 50 per cent and the VIX increases by 50 per cent. We hold our stocks and sell down 1 unit of VIX for a profit of 5.

In period 3, both the stock market and VIX normalise back to their original prices. We still get to keep 5 in profit from the prior market moves. The VIX position is also built back up to 2 units.

This is a simplified example but provides the intuition on how Vega usually manages downside risk.

Holding cash

Holding cash in our view is one of the least preferred options to mitigating downside risk. That said, we do hold a lot of cash in our portfolio (circa 50 per cent) but this is acting as reserve capital for our derivatives positions as opposed to a means of downside protection.

The issue with cash is that it’s guaranteed to under-perform over time relative to a portfolio of stocks or other risk assets. As such, it adds a continuous negative drag to a portfolio’s returns. Since recessions are often years apart, the opportunity cost of the drag is actually quite large.

Even if the portfolio weightings of cash are adjusted over time based on stock valuations, cash may still be a drag on performance if stock prices rise despite appearing expensive.

We believe it’s worthwhile for investors to compare the opportunity cost of the drag relative to the cost of other forms of downside protection.

Taking a long term view

Regardless of the downside exposure a recession brings, it’s ultimately just one event and a normal part of the business cycle. Many recessions will follow in the future and each down market will eventually recover. Patience is the key.

Never miss an update

Enjoy this wire? Hit the ‘like’ button to let us know.

Stay up to date with my current content by

following me below and you’ll be notified every time I post a wire

Scott has seven years of experience in investment and risk management, was previously an analyst at Montgomery Investment Management, and holds a degree Economics from the UWA as well as a Master’s degree in Financial Mathematics from UNSW.

15 topics

Scott Shuttleworth

Founder and Portfolio Manager

Vega Capital

Scott has seven years of experience in investment and risk management, was previously an analyst at Montgomery Investment Management, and holds a degree Economics from the UWA as well as a Master’s degree in Financial Mathematics from UNSW.

Expertise

Scott Shuttleworth

Founder and Portfolio Manager

Vega Capital

Scott has seven years of experience in investment and risk management, was previously an analyst at Montgomery Investment Management, and holds a degree Economics from the UWA as well as a Master’s degree in Financial Mathematics from UNSW.

Expertise

Comments

Comments

Sign In or Join Free to comment