5 golden rules for capital raisings

National Australia Bank’s move to go cap-in-hand to shareholders has tipped coronavirus-induced equity raisings on the ASX well past the $10 billion milestone.

For perspective, ASX companies raised a record $90 billion in capital during the 2009 financial year, so it’s likely that more and more deals will pile up on investors' desks.

In case you missed it, Michelle Lopez from Aberdeen Standard Investments and Ben Rundle of NAOS Asset Management recently discussed the key things you should know when it comes to assessing a raising and how they approach these opportunities. I’ve summarised their views in this wire to help you capitalise on the best capital raisings.

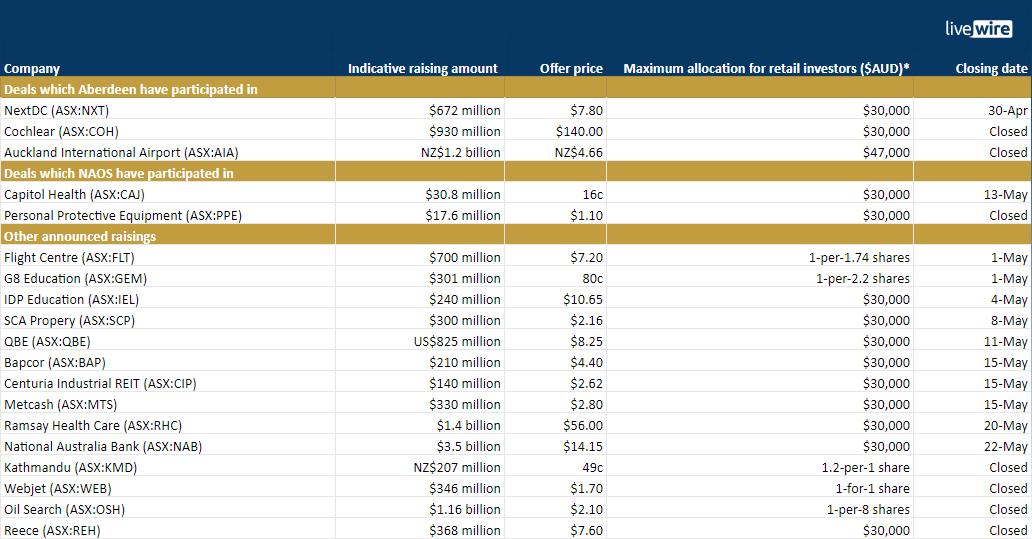

Table: Over $11 billion and counting... equity raisings due to COVID-19

Click to enlarge

Source: Livewire, ASX announcements (as at 23 April 2020). *Some offers may be subject to scale backs

The golden rules

1 - Take a long view

As a starting point, Michelle suggests only participating in opportunities where investors have a positive outlook on the given company’s business and fundamentals.

"We really are investing in those companies, come capital raising that we want to be long-term shareholders in. For us, the process is quite organic in the sense of it's not just about the discount, which is typically where people focus or spend a lot of their time focusing on."

The thinking is similar for Ben, who reckons investors should take a 3-5 year view when participating in a raising.

2 - Understand the use of capital

When it comes to assessing an opportunity, the use of capital is where Michelle spends most of her time and considers two factors in particular. The first is de-risking the balance sheet.

"What we want to see within the capital raising is enough money to see them through at least the next 12 to 18 months given the very sharp dislocation that we're seeing in the markets at the moment. Because what we know is that once the balance sheet risk has been removed, companies tend to rerate and that's where you see the strong share price appreciation."

The other is the growth aspect. If money is being put towards growth, then investors need to consider whether any short-term dilution of returns will be more than offset over the long-term by earnings growth management expects to accrete from M&A or the organic opportunity in question.

3 – Examine management’s track record for success

Ben adds that where money is being put towards growth, investors need to research management’s track record in successfully executing past deals.

"A lot of acquisitions in our view don't actually work despite the fact that there will be distressed assets out there and there might be a huge amount of opportunity. If the management team doesn't have a great track record in acquiring businesses, then that's something we're very cautious of."

4 – Check for management alignment

Both Michelle and Ben believe it’s critical to see company executives and founders participate in an equity raising. That shows alignment with investors and is also a sign of confidence that should help attract deep-pocketed institutional investors.

5 - Consider the discount

Michelle says the discount is important as the more enticing it is, the more likely investors will be willing to participate.

"But you do need to be careful with the discount, and not just look at the closing price, but really the performance in the lead up to the capital raise."

Deals Aberdeen and NAOS have taken up

Putting those golden rules into practice, Michelle said Aberdeen has participated in equity raises from Cochlear (ASX:COH), NEXTDC (ASX:NXT) & Auckland International Airport (ASX:AIA).

On Cochlear...

"Post the capital raising they've got close to $1 billion of liquidity, and this really ensures that the balance sheet risk is completely off the table and allows them to invest through the next period of material dislocation. What that means is that this company is actually going to come out at the other end in a much stronger position, and it's going to come out when competitors are in a position that they're still defending product recalls, and could potentially be in possible financial distress."

On NextDC...

"The capital raising really shores up their balance sheet and allows them to progress with the growth strategy that they have been very clearly articulating and executing on over the last four to five years. So with that in mind and the response from capital raising, we are comfortable owners of them."

On Auckland International Airport...

"This is a strategic asset that is imperative to the future of New Zealand as a nation. And we felt the intrinsic value of that company wasn't being reflected in the valuation. So that was one that we participated in and I've got very strong confidence in the long term."

As for NAOS, Ben had taken up opportunities in People Infrastructure (ASX:PPE) and Capitol Health (ASX:CAJ).

On People Infrastructure...

"About 50% of their earnings are exposed to providing nurses to hospitals. Now obviously that's come under a little bit of pressure lately because a lot of the hospitals are actually empty while they prepare for a potential onslaught of patients to come from COVID-19. The capital raise is partly for balance sheet repair; they carried a little bit too much debt coming into this and it's also partly to take advantage of acquisition opportunities and the management team has a fantastic track record of doing so."

On Capitol Health...

"Radiology for us, we think it's a fairly stable business and that, post COVID-19 world, will come back pretty quickly. So we think that coming out of this with a strong balance sheet, those assets will be certainly sought after."

Check out our Buy Hold Sell series

- Access Michelle and Ben's full interview on assessing capital raisings here

- In case you missed it, they also discuss '5 pandemic-resistant growth stocks' here

- Later this week, they'll discuss ex-20 stocks that are popular among investors right now

- View the full Buy Hold Sell archive here

Never miss an update

Enjoy this wire? Hit the ‘like’ button to let us know.

Stay up to date with my current content by

following me below and you’ll be notified every time I post a wire

I have over 15 years’ experience covering financial markets and property, with a particular interest in ETFs and personal finance. I split my time between Australia and Canada to bring a global perspective to my work.

........

This article is for informational purposes only and should not be considered financial advice. The article may contain the views or opinions of third party contributors to Livewire Markets. These contributors have not considered your objectives, financial situation, or needs. The information in this article should not be relied upon as a substitute for personal financial advice. Livewire Markets recommends that you seek independent advice before you apply for any financial product or service. Livewire Markets is exempt from requiring an AFSL under ASIC Regulatory Guide 36, section 66.

2 topics

5 stocks mentioned

1 contributor mentioned

I have over 15 years’ experience covering financial markets and property, with a particular interest in ETFs and personal finance. I split my time between Australia and Canada to bring a global perspective to my work.

Expertise

I have over 15 years’ experience covering financial markets and property, with a particular interest in ETFs and personal finance. I split my time between Australia and Canada to bring a global perspective to my work.

Expertise

Comments

Comments

Sign In or Join Free to comment

most popular

Investment Theme

If 24 LICs ran the Melbourne Cup, which ones would we back?

Affluence Funds Management

Equities

Buy Hold Sell: 5 ASX stayers built to go the distance

Livewire Markets