5 steps to getting your equity income back on track

Given the unimaginable extent of the dividend cuts across the market, equity income investors must explore new ways to generate sufficient income. Here’s how to design a retirement income strategy that can potentially deliver reliable, consistent income through a multitude of market scenarios.

Step 1: Step back from just thinking about dividend yields

For a large number of investors, their equity income strategy is based on identifying the most attractive high dividend yield names to invest in.

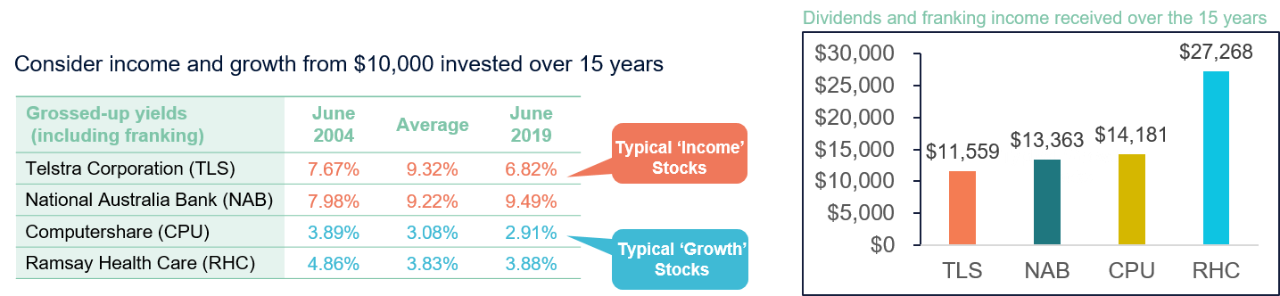

Most income investors will only invest in high dividend yielding stocks like Telstra and National Australia Bank. They may be attractive in the short term, but are these stocks effective at providing income over time? Which of the following four stocks do you think delivered the highest income on a $10,000 investment between June 2004 and June 2019?

Sources: First Sentier Investors, Factset, IRESS. 65 stocks from the current S&P/ASX100 have the required 15 year price and dividend history. Forecast yield data calculated from the following year’s total dividend divided by the start of year stock price. Total income and capital over 15 years calculated assuming $10,000 is invested in June 2004. Any fund or stock mentioned in this presentation does not constitute any offer or inducement to enter into any investment activity.

Look at the difference between yield and long-term income. Investors in the low yield stocks would have received significantly more income than those in high yield names. Investors need to look beyond dividend yields for better income and total return opportunities.

Step 2: Think about income as a dollar concept, not a percentage (yield)

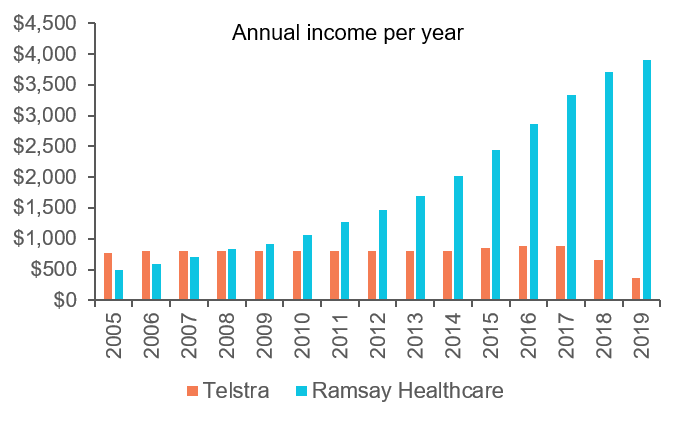

We often see the terms yield and income used interchangeably when describing investment strategies. When developing retirement income plans, the discussion with the client is in dollars. Yet we switch to percentages when thinking about investment strategies. Focusing on yield, which is simply the dividend income as a percentage of the current share price, is a classic example of this change. But as you can see from the higher income delivered by Computershare and Ramsay Healthcare, they couldn’t be further apart. Thinking about dividend income on a ‘yield’ basis can deliver poor income on a ‘dollar’ basis over the long term.

Step 3: Adopt a long-term mindset when thinking about income

In the early years, stocks with higher yields will generate more income. But in the long term, it’s a very different story. For stocks like Ramsay Healthcare, Computershare, and countless others, the low yield has been paid on a share price that has been growing over time.

Sources: First Sentier Investors, Factset, IRESS. 65 stocks from the current S&P/ASX100 have the required 15 year price and dividend history. Forecast yield data calculated from the following year’s total dividend divided by the start of year stock price. Total income and capital over 15 years calculated assuming $10,000 is invested in June 2004. Any fund or stock mentioned in this presentation does not constitute any offer or inducement to enter into any investment activity.

These companies reinvested in their business rather than just paying out high dividends in the early years. Over time, companies that can achieve higher earnings per share typically deliver stronger share price appreciation – and a higher dividend per share growth. This results in potentially higher income – and total return – for the investor over time. This is the key to generating sustainable, long-term income.

Step 4: Embrace a total return focus

By thinking long term and understanding that longer term earnings growth will underpin long-term dividend income, investors can embrace a total return approach to selecting stocks in their portfolio. Just think how powerful that is. A total return approach provides the flexibility to be invested in the right stocks, at the right time, at the right price during different market conditions. This approach can seek to deliver a diversified portfolio that can weather a multitude of market conditions and avoid the concentration problems experienced by many equity income strategies. This means your conservative equity income investors can continue to access the best investment ideas across the share market, even when there is a need for income.

Step 5: Understand the role options can play in your equity income strategy

What if your clients want more income now? A carefully implemented options strategy can be used to balance short term income needs with the generation of long term total returns – and be delivered with smoother returns through the market cycle. In addition to the two traditional streams of income generated from dividends and franking credits, an options strategy can exploit share price volatility to generate a third stream of income called option premium income. This additional stream generates potentially higher income when the market is experiencing elevated volatility – particularly through the tougher periods where companies are forced to cut dividends. These three sources of income provide opportunities to generate above market income distributions through various market conditions.

A powerful case study on the value of advice

For more than 15 years I have been encouraging investors of the critical need to think differently when it comes to generating income from equities compared to traditional income asset classes like bonds and cash. However, there is an understandable desire to keep things simple when it comes to implementing client portfolios. As a result, the investment world is prevalent with the use of ‘rules of thumb’ and ‘assumed truths’. The belief that ‘high dividend yield delivers high income’ is a simplification that receives widespread coverage in this income-starved market. Educating our clients about the reality of this concept provides a valuable opportunity to demonstrate the value of seeking expert financial advice to assist with meeting their retirement income challenge.

Want more insights on Australian income?

A series of regular news updates, research papers, investment strategy updates and thought pieces from some of First Sentier's leading experts can be found here

Never miss an update

Enjoy this wire? Hit the ‘like’ button to let us know.

Stay up to date with my current content by

following me below and you’ll be notified every time I post a wire

Rudi is Head of the Equity Income and Target Return Income Funds, and is responsible for investment strategy, stock selection, portfolio construction, investment process enhancement and management of the Equity Income investment team

........

This material has been prepared and issued by First Sentier Investors (Australia) IM Ltd (ABN 89 114 194 311, AFSL 289017) (Author). The Author forms part of First Sentier Investors, a global asset management business. First Sentier Investors is ultimately owned by Mitsubishi UFJ Financial Group, Inc (MUFG), a global financial group. A copy of the Financial Services Guide for the Author is available from First Sentier Investors on its website.

This material contains general information only. It is not intended to provide you with financial product advice and does not take into account your objectives, financial situation or needs. Before making an investment decision you should consider, with a financial advisor, whether this information is appropriate in light of your investment needs, objectives and financial situation. Any opinions expressed in this material are the opinions of the Author only and are subject to change without notice. Such opinions are not a recommendation to hold, purchase or sell a particular financial product and may not include all of the information needed to make an investment decision in relation to such a financial product.

CFSIL is a subsidiary of the Commonwealth Bank of Australia (Bank). First Sentier Investors was acquired by MUFG on 2 August 2019 and is now financially and legally independent from the Bank. The Author, MUFG, the Bank and their respective affiliates do not guarantee the performance of the Fund(s) or the repayment of capital by the Fund(s). Investments in the Fund(s) are not deposits or other liabilities of MUFG, the Bank nor their respective affiliates and investment-type products are subject to investment risk including loss of income and capital invested.

To the extent permitted by law, no liability is accepted by MUFG, the Author, the Bank nor their affiliates for any loss or damage as a result of any reliance on this material. This material contains, or is based upon, information that the Author believes to be accurate and reliable, however neither the Author, MUFG, the Bank nor their respective affiliates offer any warranty that it contains no factual errors. No part of this material may be reproduced or transmitted in any form or by any means without the prior written consent of the Author.

In Australia, ‘Colonial’, ‘CFS’ and ‘Colonial First State’ are trade marks of Colonial Holding Company Limited and ‘Colonial First State Investments’ is a trade mark of the Bank and all of these trade marks are used by First Sentier Investors under licence.

1 topic

4 stocks mentioned

Rudi is Head of the Equity Income and Target Return Income Funds, and is responsible for investment strategy, stock selection, portfolio construction, investment process enhancement and management of the Equity Income investment team

Expertise

Rudi is Head of the Equity Income and Target Return Income Funds, and is responsible for investment strategy, stock selection, portfolio construction, investment process enhancement and management of the Equity Income investment team

Expertise

Comments

Comments

Sign In or Join Free to comment