5 stocks that could double cash flow in 5 years

Whilst we use a megatrend framework to identify a narrow subset of stocks that we then spend more time understanding, we ultimately invest capital on a stock by stock, bottom up basis. We focus heavily on cash flow growth as a key metric of how we look to invest money. We also acknowledge the need to appropriately diversify the portfolio holdings from an industry perspective.

We spend almost all of our time trying to find ideas where companies can generate cash flow growth, regardless of the macro backdrop we are faced with. If a company can generate strong cash flows in different market environments, then we believe the market will recognise the inherent value in a company’s ability to generate cash flow growth, and the share price will ultimately reflect that.

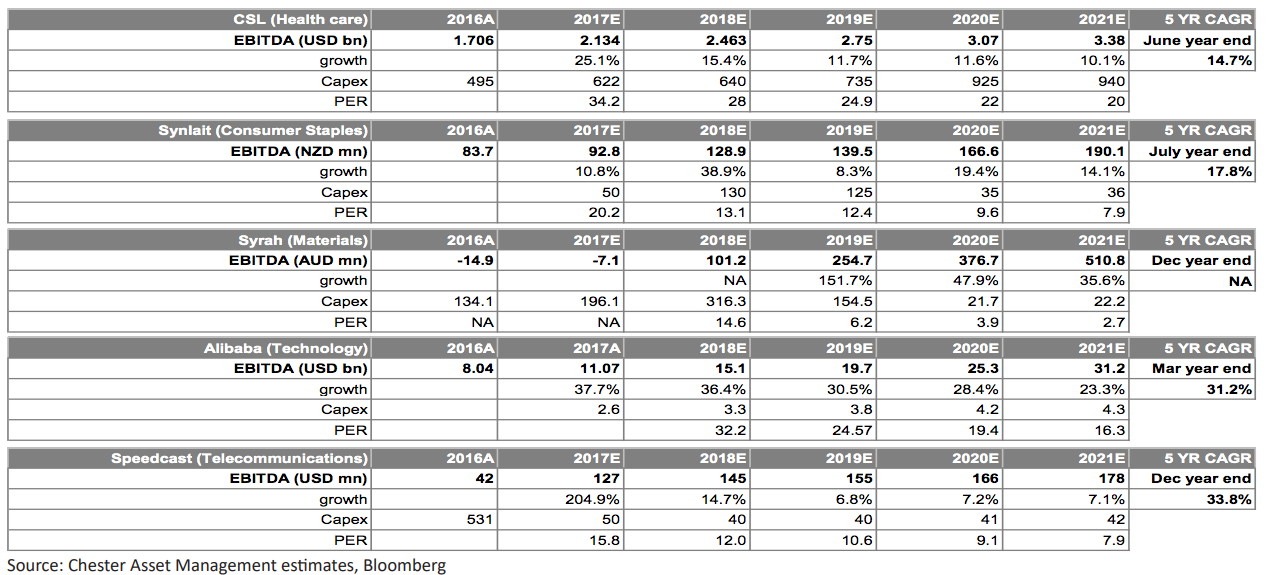

The examples we have set out below provide more detail around this idea, with all these companies (operating in a wide variety of industries) demonstrating an ability to at least double cash flow over the next 5 years (using EBITDA as an admittedly imperfect proxy).

How a company is selected for the portfolio then is a combination of the predictability of those cash flows, or on our belief the market is significantly discounting a company’s ability to generate those cash flows.

Just as important in stock selection, is what is the capital (capex) required to generate that cash flow growth? Return of capital employed is a critical metric to assess a company’s ability to generate shareholder returns. The companies listed below have a combination of organic growth, or are spending significant capital to generate the cash flow trajectory. We think the return on capital provides a strong incentive for these companies to outlay this capital.

CSL

CSL has the dominant position in the global blood therapeutics industry (circa 35% market share). It is the lowest cost producer of plasma derived therapies that treat a wide range of immune deficient diseases. Our thesis revolves around an industry growing at 6-8% per annum with a major competitor (Shire 25% market share) not growing plasma collections at all. This enables the rest of the industry to grow in the mid double digits over the next 12-18 months, with CSL well placed to enhance margins through this period. We view the cash flows as relatively predictable. We see CSL as fair value at current levels, and expect a period of consolidation ahead given the strong price appreciation over the past 6 months. We will look to accumulate on weakness, given we believe, the unique nature of the CSL industry structure and growth profile.

Synlait

Synlait Milk (SM1) is a business to business dairy processing company, in Canterbury (south of Christchurch) in NZ. SM1 doesn’t own brands however they control the supply chain with farmer relationships and processing facilities and (will) control (CFDA and FDA) processing licences. SM1 is probably best known for its relationship with A2 Milk (A2M) as the exclusive supplier of infant milk formula (IMF) to A2M in Australia, NZ and China. SM1 has invested materially in the past 10 years with recent additions leaving the company with ample near-term capacity including; 3 spray dryers with ~140,000tpa capacity; two wet mix kitchens with IMF capacity to 80,000tpa; and two IMF canning facilities, the second being the acquisition of New Zealand Dairy Company in May, providing ~60,000tpa of canning capability.

In the past 5 years as capacity expanded sales volumes increased from ~55,000t in FY11 to 116,000t in FY16. During this time however gross profit increased ~5x from margin expansion from upscaling from base ingredients (whole milk powder, skim milk powder, etc.) to complete nutritional products (IMF). IMF can generate 10x the GM per tonne of base ingredients for Synlait. SM1 has given IMF production guidance of 28,000t in FY18. Beyond FY18 projections get a bit more challenging but it is our understanding SM1 (and hence A2M) are front of the queue for CFDA approval for Chinese labelled IMF products. This is important given consolidation of >2,000 IMF brands to ~500 has potential to create big winners and losers in the ~1Mtpa China IMF market.

We see a case where SM1 can grow to >50,000tpa of canned IMF in 5 years which provides a case for material margin expansion on a margin per tonne and overall gross margin basis.

Syrah Resources

Syrah (SYR) is 6 weeks away from producing high grade graphite flake from the worlds largest graphite mine at one of the lowest costs globally. The graphite flake can be used for a variety of purposes, but the fastest growth area in graphite use is for flake to be processed into spherical graphite which is then used in the production of battery anodes for Lithium Ion batteries. Our assumptions below reflect a confidence that Syrah will spend significant capital processing their flake into spherical graphite. On our estimates, we believe the share price can double in the next 3 years, while understanding there is significant forecasting error in these numbers due to a range of pricing and production outcomes. We believe the share price though is overly discounting the likelihood of this scenario occurring, thus we see a strong valuation margin of safety.

Alibaba

Alibaba (BABA US) is one of the world’s largest companies that dominates online shopping in China. Taobao (consumer to consumer) and Tmall (business to consumer) are the dominant ecommerce sites in China that are backed by Alipay, the dominant online payment system in China. At a recent investor day, BABA upgraded its expectations for FY18 revenue growth from 35% to 45-49%. On a price to growth basis, it remains very compelling value.

Speedcast

Speedcast (SDA) provides satellite telecommunication solutions to remote areas. It provides services to the Energy industry, Cruise ships and Maritime services, Mining sites and Defence force locations. By purchasing Harris Caprock in 2016, it has removed one of its largest competitors in the Energy industry. This is a company transforming acquisition which gives SDA strong diversification across both geographic and sector exposure. We believe the remote communications industry will continue to grow in excess of GDP for the foreseeable future, and SDA is certainly not expensive for the growth it provides.

This is an extract from the Chester High Conviction Fund quarterly market commentary.

Never miss an update

Enjoy this wire? Hit the ‘like’ button to let us know.

Stay up to date with my current content by

following me below and you’ll be notified every time I post a wire

Rob recently founded Chester Asset Management after 7 years at SG Hiscock where he was PM of the SGH Australia Plus product that delivered in excess of 10% outperformance per annum over 3.5 years.

3 stocks mentioned

Rob recently founded Chester Asset Management after 7 years at SG Hiscock where he was PM of the SGH Australia Plus product that delivered in excess of 10% outperformance per annum over 3.5 years.

Rob recently founded Chester Asset Management after 7 years at SG Hiscock where he was PM of the SGH Australia Plus product that delivered in excess of 10% outperformance per annum over 3.5 years.

Comments

Comments

Sign In or Join Free to comment

most popular

Equities

Buy Hold Sell: 5 ASX stayers built to go the distance

Livewire Markets

Funds

The 5 best-performing super funds of the year

Livewire Markets