86% of capital raisings have outperformed the market

Relief from the COVID-19 shutdown appears to be getting closer as governments in Australia, and other parts of the world, plan for how society looks coming out of hibernation. Australia has led the world in capital raisings which, in hindsight, may prove to be excessive but understandable given the extreme uncertainty. There will be winners and losers out of this market dislocation as their always is during economic recessions. We continue to search diligently for stocks that represent long term value based on our assessed sustainable valuation models. The huge value divergence within the market suggest that there is rich pickings for alpha generation.

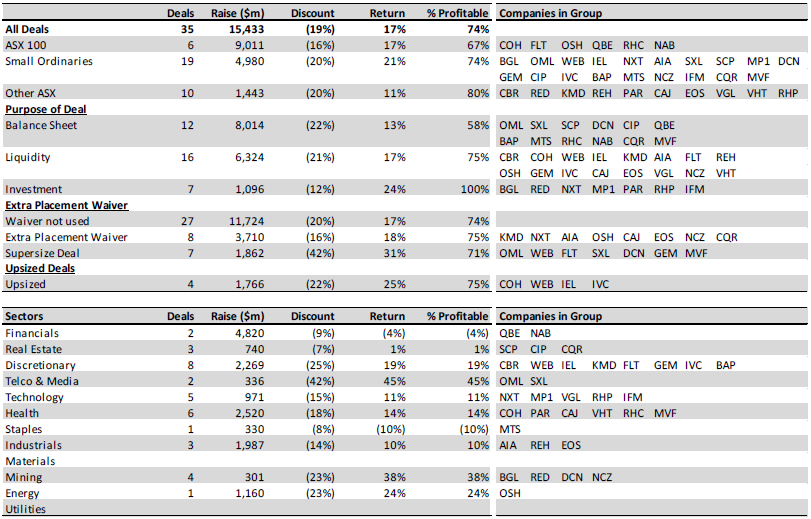

Equity raising in lockdown

Australia is leading the world in equity raisings during the COVID-19 crisis, which is a little surprising given the lockdown in Australia is not as restrictive as some other countries. According to Deal Logic, Australia comprises some 42% of global equity raisings since 1 March 2020. We suspect boards and management have long memories from the GFC, reminding them that raising early and once was a better outcome than waiting and hoping. Since mid-March, more than AUD 15bn in equity raisings via 35 deals (and counting) have been announced, with balance sheet and liquidity concerns being the primary driver. Goldman Sachs has calculated that 86% of the raisings have outperformed the market to date with the larger discounted equity offerings generating more alpha as one would expect and in line with the GFC experience.

Given we are now starting to relax the economic and social restrictions in Australia, many boards may have raised in excess of their requirements, which could result in substantial buybacks at prices well above the price raised. This was certainly the case during the GFC. It will be interesting to observe whether boards go down a different path and use excess capital to make opportunistic investments.

We have been surprised, albeit with sympathy, by the dire scenarios and resulting size of raising that some companies have executed. For example, both Oil Search and G8 Education raised enough equity to survive current conditions until the end of CY21. Other companies, such as Metcash, QBE, Ramsay and even NAB, to a certain extent, have also surprised the market with their equity raising. Management commentary for these surprise raisings tended to include an aspect of growth and potential opportunities coming out of the downturn.

Dividends have become collateral damage of the equity raisings and lower earnings.

Macquarie Research estimates that dividend forecasts for Australian companies have been cut by 23% since the February high. We expect dividends and earnings to fall further from here, with the reporting season in August to provide further clarity. Despite banks being in a much better capital position today, compared to the GFC, the unprecedented nature of the crisis and the social element of helping customers get through the downturn has resulted in dividends being substantially cut or deferred.

When it became clear in early March that shutdowns within Australia and globally were likely, due to the COVID-19 crisis, we quickly started to adjust our earnings and valuations across our investable universe. Drawing a line in the sand is always exceedingly difficult in a situation that is in such a high degree of flux. However, we have assumed that Q2 and Q3 within Australia will see negative GDP growth followed by the start of a recovery (from a low base) in Q4 2020. Recovery of earnings for many companies will take years to reach 2019 levels and by our estimates, some will remain lower until 2023.

Nikko AM has been supporting companies within the Comparative Value Analysis strategy (CVA) that have raised capital via placements. In some instances we have taken in excess of our pro-rata which has, in general, been alpha generating.

Table 1 - Summary of ASX equity raisings since mid-March 2020

Source: Macquarie Research

An unprecedented stimulus

Governments, central banks and various other government agencies around the world have been working together to stabilise their country’s economy and support people and businesses during the government-mandated restrictions and shutdowns. The fiscal and monetary responses have been typical of countries during wartime and thus are unprecedented in the sheer geographic and size scale. The policy response and mass deployment of government resources will, as is always the case in a downturn, inevitably generate winners and losers. This type of dislocation always changes how society acts and spends.

The stimulus may also fuel inflationary pressures and thus eventually push interest rates higher.

The policy response from the Australian government is one of the largest in the world as a share of GDP. A highlight of the policy response has been the coordination from the various government agencies and the state governments via the ‘National Cabinet’. The National Cabinet has allowed both federal and state governments to coordinate health and policy responses on a national level while also being able to act quickly and independently on their own. The fiscal and monetary response now totals about 16% of GDP and the quick response allows it to be deployed quickly. WA, QLD and NT are the first to relax social distancing laws with the other states and territory likely to follow over the next few weeks. This relaxation is well ahead of where the Federal Government was suggesting when they first introduced the measures.

The stimulus is required given the severity of the shutdown, which is resulting in some incredibly dire forward-looking economic data. Consumer and business confidence has plummeted to levels rarely or ever seen. Unemployment levels are likely to go above 10% according to most economic commentators and the RBA is suggesting in its latest monetary policy decision that they expect output to fall by around 10% over the 1H20 and thus 6% over the full year followed by a bounce of 6% in 2021. The RBA is also of the view that although unemployment may peak at 10% over the coming months, it will remain above 7% at the end of 2021. Additional data that is illustrating how deep the government’s mandated lockdown is impacting the economy is April car sales, which plummeted 52% month-on-month and 48% year-on-year to the lowest level since the 1990s.

We would expect both state and federal governments to introduce further stimulus once the lockdown measures have been relaxed to help the economy come out of the recession. The RBA has all but suggested that interest rates will remain very low for the next few years given that inflation is expected to remain below their targeted range for that long.

New COVID-19 cases appear to have peaked in most advanced economies resulting in discussion and actual action in moving out of lockdown across the globe. The high-frequency Apple mobility trend data is suggesting that movement amongst the general population troughed in early April and has certainly increased strongly over the past few weeks.

Banking on dividends

In our previous report COVID-19 Special: Spotlight on Sectors, we shared our view that the banks’ capital levels were in much better shape before the COVID-19 pandemic than they were in the lead up to the GFC and so they should get through the crisis without raising capital. On 27 April, NAB proved this forecast was incorrect when it released its 1H’20 results early, which included a $3.5b equity raising and a substantially reduced dividend.

The pro-cyclicality of both impairments and risk weighted assets means that the capital levels are likely to be lower than what the board are comfortable with.

The irony is that as the economy moves out of the COVID-19 recession, banks will have excess capital exactly when they don’t require it and conversely lower capital going into an economic downturn just when they need it.

ANZ and Westpac have deferred their dividend and any potential capital raising, making the economically rational decision of holding back dividends and thus not raising dilutive capital at levels below book value unless absolutely necessary. If the economic situation continues to improve we would expect all the banks to pay a final dividend later in the year in their full year result.

The bank sector looks attractively valued based on the assumption that the downturn doesn’t become too dire and thus impairment levels remain manageable. Even under the worst case scenarios that ANZ, WBC and NAB have outlined, the banks remain profitable. However, the low interest rate environment that appears to be the base case for some years, and the obvious uncertainties around the ultimate levels of bad debts, make the short- to medium-term outlook for banks more problematic. However it is arguable that this is already priced in given that, with the exception of CBA, the banks are trading well below book value.

Stay one step ahead

We manage using an intrinsic value style that seeks to identify good value stocks that offer the best compromise between risk and expected return. Click 'follow' to be the first to read our latest insights, including where we are finding the most compelling opportunities on the ASX.

Never miss an update

Enjoy this wire? Hit the ‘like’ button to let us know.

Stay up to date with my current content by

following me below and you’ll be notified every time I post a wire

Brad joined the business in 2002. He has 28 years’ experience primarily in the funds management and stockbroking industry, and has overall responsibility for managing the Australian equities team, process and portfolios. Prior to joining, Brad was Director, Corporate Finance with Westpac, a Senior Resource Analyst with Ord Minnett and in his early career, a geologist working with a number of resource companies. Brad has portfolio management responsibilities for the Tyndall Australian Share Wholesale Fund and Tyndall CVA Plus Strategy. He has analyst responsibilities for Banks.

........

This material was prepared and is issued by Nikko AM Limited ABN 99 003 376 252 AFSL No: 237563 (Nikko AM Australia). Nikko AM Australia is part of the Nikko AM Group. The information contained in this material is of a general nature only and does not constitute personal advice, nor does it constitute an offer of any financial product. It is for the use of researchers, licensed financial advisers and their authorised representatives, and does not take into account the objectives, financial situation or needs of any individual. The information in this material has been prepared from what is considered to be reliable information, but the accuracy and integrity of the information is not guaranteed. Figures, charts, opinions and other data, including statistics, in this material are current as at the date of publication, unless stated otherwise. The graphs and figures contained in this material include either past or backdated data, and make no promise of future investment returns. Past performance is not an indicator of future performance. Any economic or market forecasts are not guaranteed. Any references to particular securities or sectors are for illustrative purposes only and are as at the date of publication of this material. This is not a recommendation in relation to any named securities or sectors and no warranty or guarantee is provided.

9 stocks mentioned

Tyndall AM

Brad joined the business in 2002. He has 28 years’ experience primarily in the funds management and stockbroking industry, and has overall responsibility for managing the Australian equities team, process and portfolios. Prior to joining, Brad was...

Expertise

Tyndall AM

Brad joined the business in 2002. He has 28 years’ experience primarily in the funds management and stockbroking industry, and has overall responsibility for managing the Australian equities team, process and portfolios. Prior to joining, Brad was...

Expertise

Comments

Comments

Sign In or Join Free to comment

most popular

Equities

Buy Hold Sell: 5 ASX innovators with massive potential

Livewire Markets

Equities

21 ASX stocks that should be on your radar

Livewire Markets