TOL - 20th Jan, 2021

A greater opportunity in a greater fool world

Gino Rossi

Spheria Asset Management

Many would argue that today’s market bears little resemblance to the Dotcom bubble. Yes, the by-products of increased risk-taking are different. However, the mindset of investors is remarkably similar. The greater fool theory is pervasive; risk is under-priced; and current conditions are being extrapolated into perpetuity.

There are various examples which indicate that the mentality of many investors today is “you can’t possibly lose”.

Bitcoin

The cryptocurrency is a useful gauge of risk appetite since (unlike equities) there is no future expected cash flows, other than the balloon payment that comes upon sale to another market participant. No buyer, no value.

There are microcap stocks exposed to Bitcoin, such as US company Riot Blockchain, for those who find Bitcoin's volatility too passe. Riot is a former US biotech company which now aims to be one of the largest and lowest cost bitcoin miners in North America. The one analyst covering it expects revenue of US$10 million and a loss of -US$20 million in FY20.

The market capitalisation currently sits at an astounding US$1.8 billion.

SPACs

SPACs are another example of elevated risk-taking. SPAC stands for Special Purpose Acquisition Company and involves investors handing over capital before even knowing what they’re buying. SPACs raise money in an initial public offering and use the proceeds to acquire a privately held operating business not identified at the time of listing.

Why undertake this structure? The key reason is that the promoter, often a high-profile investor or former executive, typically receives 20% of the SPAC’s equity. Investment banks are also only too happy to oblige as it is a new source of fees and a much easier route to raise money for clients than a traditional IPO. Yes, private equity is pleased too, since they are often the sellers of the companies these SPACs acquire.

So it’s great for the bankers, private equity firms, SPAC promoters and management teams, but why would investors agree to this? Well, this is less clear. Especially since investors start the venture 20% in the red by granting equity to the SPAC promoter. Some high profile SPACs such as Nikola have been rocky, and SPACs have been used for pump and dump scams in the past. Despite these risks, investors are clambering for more.

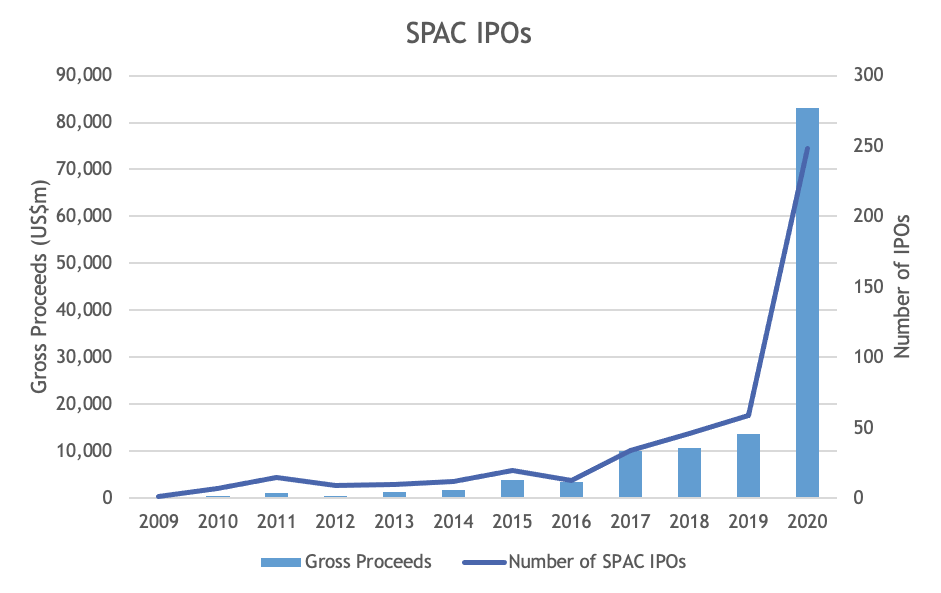

The chart below shows the extent of the increase. In 2020 248 SPACs IPO’d with a combined amount raised of US$83 billion. That’s $83 billion in blank cheques.

Source: SPAC Insider

Increased retail use of call options and passive investing is further evidence of the extent of this risk on environment.

Will investors be adequately compensated for the risk they are now taking in investments such as those mentioned above? We very much doubt it.

The riskiest investments are those where investors perceive no risk at all.

So where can investors turn for long term growth and capital preservation? Underneath the surface and beyond the headlines, significant opportunities are presenting for investors who are not reliant on the greater fool.

Smaller companies: a greater opportunity

The market continues to price smaller companies at a discount, reflecting a greater perceived risk and lower liquidity.

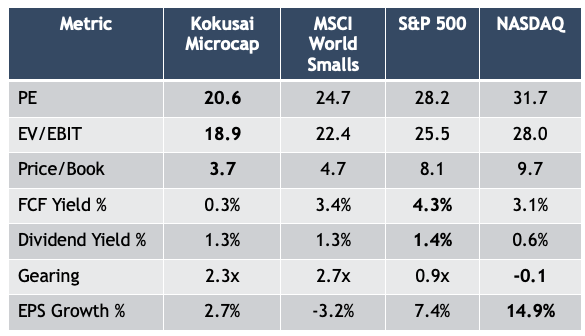

The chart below shows the discount microcaps still trade at relative to larger companies despite their higher long-term growth prospects.

Source: Bloomberg, MSCI, S&P. As at 11 January 2021.

This discount has widened in recent years, partly fuelled by a wave of money into passive funds which push up only the largest stocks. It is reassuring for professional managers such as us to still see risk being priced into this market.

Not only does this part of the market offer cheaper growth prospects, it may offer a capital preservation characteristic too at this stage of the cycle.

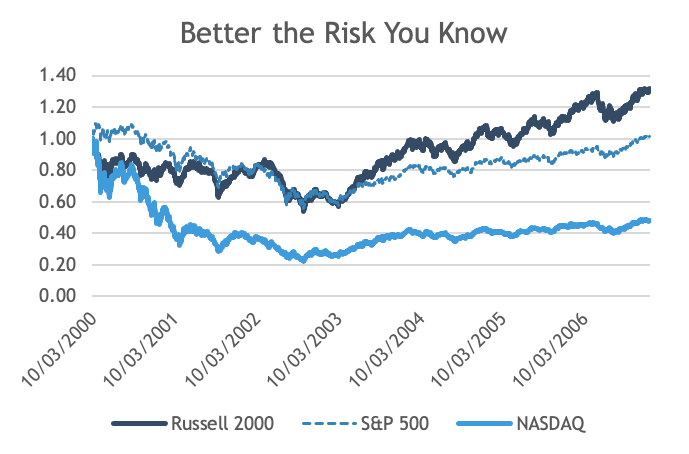

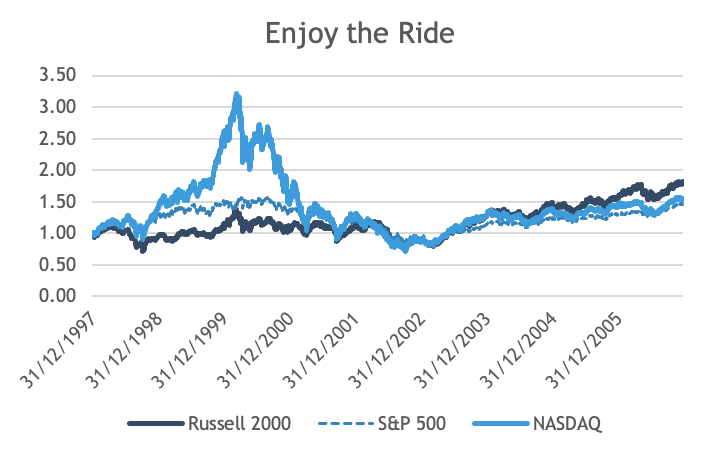

When the NASDAQ was soaring in the late 90s, confidence only grew as the market went higher (we were in a new paradigm, you couldn’t possibly lose!) However, from its peak on the 10th of March 2000 to its lows on the 9th of October 2002, the NASDAQ declined 78%. Smaller companies, despite their perceived risk, declined 46% peak to trough. The S&P500 declined 44% peak to trough.

Source: Bloomberg

Even if investors were wise enough to ride the NASDAQ for more than two years prior to its peak, and having successfully tripled their money, they were in the end no better off than an investor in the Russell 2000 if they did not sell out.

Quality global microcaps of the kind we invest in, do not require a greater fool to deliver a return. Three-quarters of our global microcap portfolio pays a dividend (portfolio dividend yield is 2.3%). Its free cash flow yield is 5.0% and the weighted average company has net cash on its balance sheet.

Across world markets, smaller companies continue to trade at lower multiples - fair compensation for their immaturity and lower liquidity. As an investor, are you being compensated for the risk you are taking? During these heady times we believe investors must take the greater opportunity, not rely on the greater fool.

Investing in tomorrow's leaders

Spheria is a fundamental-based investment manager with a bottom-up focus specialising in small and microcap companies. Stay up to date with all our latest insights by hitting the follow button below or visit the Spheria website for more information.

Never miss an update

Enjoy this wire? Hit the ‘like’ button to let us know.

Stay up to date with my current content by

following me below and you’ll be notified every time I post a wire

Featuring

2 topics

Gino Rossi

Portfolio Manager

Spheria Asset Management

Expertise

Comments

Comments

Sign In or Join Free to comment