Recovery is certain

The World Wide Pandemic Recession of 2020 will end. History is clear – all recessions have a start and an end. An economic downturn is always followed by economic recovery and economies eventually recapture their past levels of production and income, before moving forward to new highs. This recession will be no different even though its genesis is a unique and catastrophic viral outbreak.

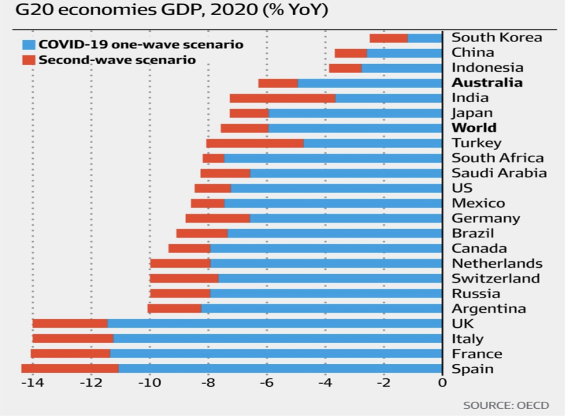

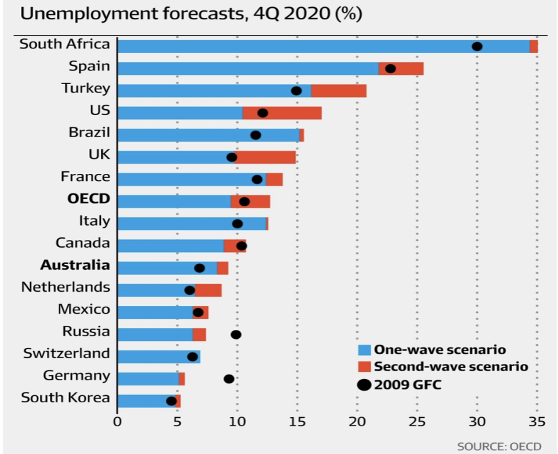

The severity of the recession is shown in the first table with the OECD forecasting what it expects to be the worst of the economic downturn, the blue bars indicating a “one-wave” pandemic scenario, and the orange section if a second-wave scenario eventuates.

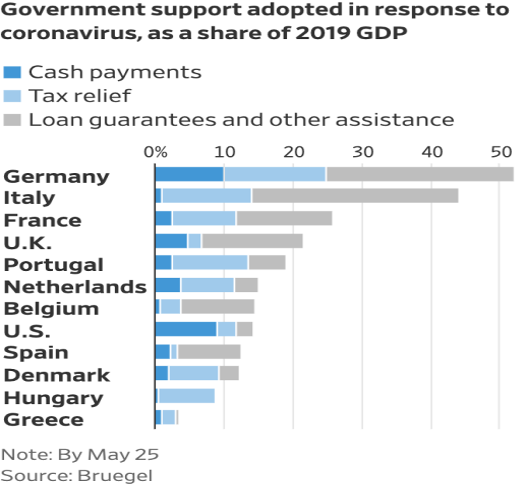

The extraordinary fiscal responses seen across major economies are noted below. The one certain output of these measures is a huge increase in government bond debt across the world.

The severity of the recession and the significance of the policy responses are critical for investors to understand, particularly SMSF investors managing their own superannuation or pension funds. SMSFs have long term commitments (pension liabilities) that will mainly be met from the returns of their investment assets. Short term price movements should be monitored if they materially alter the long term prospects of an investment. However, SMSF investors should recognise that the daily movements in the prices of most liquid assets generally simply reflect elevated levels of “noise”. More speculation rather than real substance, with a lot of fake news.

The “price” of long term assets will oscillate over the short term, driven by a whole range of illogical and senseless factors. However, over time, quality assets that benefit from economic growth and activity will increase in “value” to reflect the rising cash flows that will emerge from that growth.

And over time, sometimes quite a long time, the price of an asset will converge with its value. It is ultimately the movement in price (reflecting the movement in value) that generates the capital growth component of investment returns. The other key part is the cash flow released to the owner, whether that be interest, rent or dividends.

Rational investors patiently seek to generate their returns over a long period. They also spread or diversify their investments and utilise compounding as much as possible.

Traders may also be rational, but they try to game the market price to generate quick returns from the short term mis-pricing of assets in so-called “liquid or actively traded markets”. Whilst the trader rarely bases his or her belief in the mis-pricing of assets on a long term perspective, it is traders that set daily market prices. There are many of them and they are trading against each other. Meanwhile, long term investors sit on the sidelines of the market waiting for an opportunity to enter.

I have positioned these observations to open this letter because the 2020 recession has been so sudden and unique, resulting in truly extraordinary monetary and fiscal responses. The onset of this recession has been sharp, and it is deep. The policy responses have and will dampen the severity of the downturn. They should both aid and hasten the recovery. The unknown factor remains the trajectory of COVID-19 and the risk of a second wave. Whilst the timing of the ultimate medical solution is still unknown, history suggests that human ingenuity will probably discover an effective anti-viral drug and vaccine.

The policy responses, both monetary and fiscal, will act to guide large parts of the economy through their dislocation and hibernation. However, these policy responses will also be fuel for speculative activity. They will create a cynical view of risk that will result in a divergence of asset prices from economic reality. Well established and logical rules for the investment of capital will be challenged. These rules may well struggle to return whilst interest rates are near negative levels and bond yields are held below inflation.

The Central Banks respond

The Central Banks of the world may not be operating in a co-ordinated planned fashion, but they are acting in unison. In some respects, they appear to be behaving with desperation as they are charged with the funding of governments that have amassed mountains of debt.

The numbers are huge. At this point, the US Federal Reserve balance sheet has expanded to 39% of US GDP - having accumulated Treasury securities, US bonds, Mortgage Backed Securities and Corporate debt.

Even this is not as extreme as the expansions seen in the European Central bank (50% of GDP) or the Bank of Japan (117% of GDP).

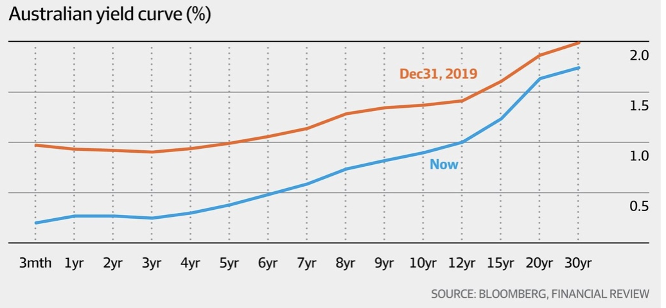

In Australia, the RBA balance sheet has expanded to 14% of GDP after printing $50 billion on asset purchases designed to drive down the bond yield curve (with a specific target of 0.25% for 3 year bonds). The chart below shows that the RBA has been highly successful in driving down the cost of Australia’s government debt. The consequences of this policy for savers or passive investors is especially worrisome.

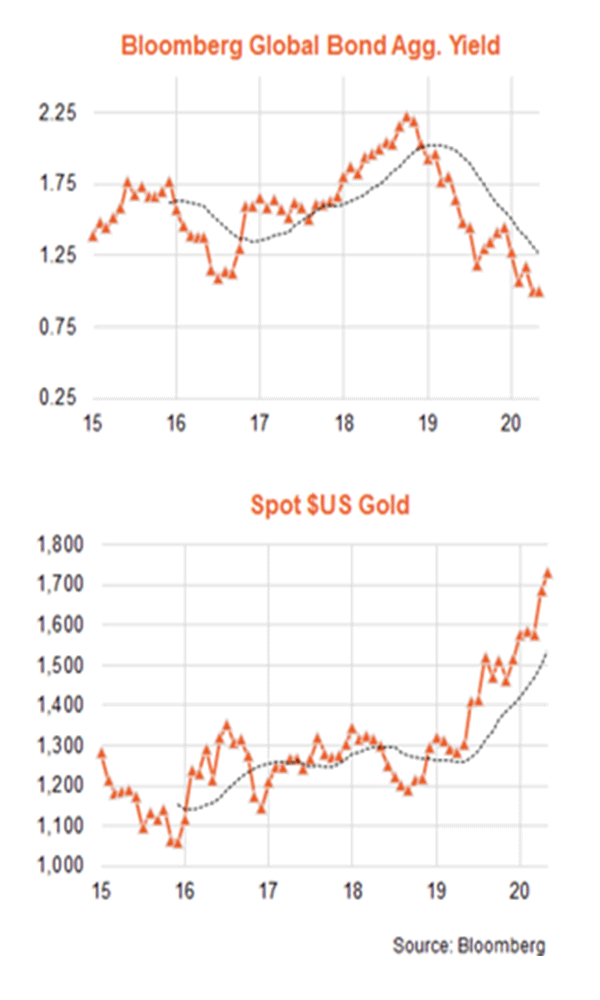

The connection between QE, near zero interest rates, asset inflation and speculation is evident in the next chart. As bond yields across the world have declined (Bloomberg Global yield index), the price of gold has soared. Whilst gold is claimed to be a store of value, it is also effectively like a zero coupon perpetual bond. Its value is difficult to define but it is arguably more finite than a 100 year government bond.

The recovery, asset prices and asset values in Australia

It is our view that the path to full recovery for Australia’s economy is unlikely to occur until some point in 2022. It may be that FY23 is the year that Australia’s economic activity and output matches that of FY19. We may be conservative, but we feel that it is better to be conservatively wrong than optimistically wrong.

The main reason for our view is the closure of our borders, a necessary policy to protect against the influx of the virus. However, the closure has directly affected both our tourism and education sectors. Tourism is our fourth largest export earner; in 2019 there were 9.3 million international tourists visiting Australia who spent $44 billion. Tourism accounts for 8% of our workforce.

Education is also a large export and generated $38 billion in 2019. In 2020, this revenue stream will be decimated and a recovery in the first half of 2021 will require a significant commitment to an arrival isolation program.

Another headwind is the slowing of population growth. It is likely that FY21 will see Australia’s lowest population growth rate since World War 2.

The above observations suggest a significant weakening through 2020 of Australia’s gross production and gross income. When the economy recoups its 2019 level in a few years’ time, it will occur with a moderate increase in both our population and work force. Thus, the per capita income of Australia in FY23 will be lower than in FY19. It is also likely that our unemployment rate in FY23 will be higher than in FY19.

As recovery eventuates, it will have a positive effect on asset values, particularly because of the extraordinary monetary and fiscal responses outlined earlier. Many (but not all) assets will recover their past value, some quicker than others. However, from the point of price recovery, the forward looking investment returns from assets will be lower due to the headwinds of lower per capita income, higher unemployment and enduring low interest rates.

The following chart shows the expected levels of unemployment and compares them to the GFC recession – which, at that time, was the worst since the Great Depression.

Our view is that after a period of sharp retracement in asset prices, there is likely to be a long period of low investment returns. The best indicator of this is both the low actual and negative real yields of longer term government bonds. Whilst they are manipulated by central banks, they do suggest that investment returns across asset classes and balanced portfolios, will be very low for a sustained period.

The problem with the notion of a return to market normality in the pricing of assets is that the major central banks have perverted the “risk free rate of return”. Further, they are increasingly intervening in the market pricing of risk assets (think corporate bonds in the US, and ETFs in Japan) to make them present as being “risk free” and therefore encouraging investors to accept lower returns.

The maintenance of these policies since the GFC, their global spread (and now in Australia) and acceleration in 2020 has created a conundrum for markets and the prices of assets, in particular the sensible allocation of capital based on risk/return.

Our concern is that many of today’s market prices for liquid assets are increasingly reflecting the expectation of a full economic recovery in 3 years’ time. This means that the normal required 3 year rate of return from a risk asset (like share indices) is being discounted at such a low rate that expected FY22 prices are brought forward and become today’s market prices.

Three thoughts flow from this observation:

- Investment returns from the recovery (through market prices) are being brought forward, particularly for liquid and higher risk assets;

- As the likely returns from recovery can theoretically be forecast from the prices (indices) reached in FY19, the projected returns from risk assets will decline as they recover their FY19 levels; and

- The long term returns from risk assets on a “look back basis” in FY23 will not exceed historic norms and so the excessive returns of today are merely “front ending “returns. This is the result of QE and low bond yields, implying that returns will plateau as time transpires.

Concludingly, whilst the short term is always hard to predict, the longer term is more certain. Because this recession is both sharp and deep, the recovery will be stronger than usual. However, the recovery will only take the world (particularly the developed world) back to where it was in FY19. Asset prices that reflected the economic conditions in 2019 may well recover to those levels in anticipation of FY23 outcomes (and beyond) … but normally, they shouldn’t do this until FY22.

This gives the appearance of a decoupling of market prices from the short term economic pain that is widely felt and seen. It also leads to seemingly logical speculation that market prices are recovering too quickly, will falter, and that a relapse is imminent.

We cannot know with any degree of certainty if this will be the case or not. But we do believe that liquid asset prices will be highly volatile throughout the journey back to recovery. Price volatility is the natural result of zero interest costs and rampant currency printing (US, Europe and Japan) which creates the fuel for excessive speculation and leveraged trading.

Increasingly, we will see evidence of economic recovery across the world in coming months. It is already occurring as the economic tracker below shows, albeit from a particularly low base.

Recovery is good for growth assets. Company profits are leveraged to economic recovery as is property. The biggest risk, and one that does not seem to exist at present, is inflation. Whilst in some respects a mild lift in inflation would be positive for company profits, an elevated lift inflation (above 3%) would cause serious dislocation in markets given the near zero yield of most bonds.

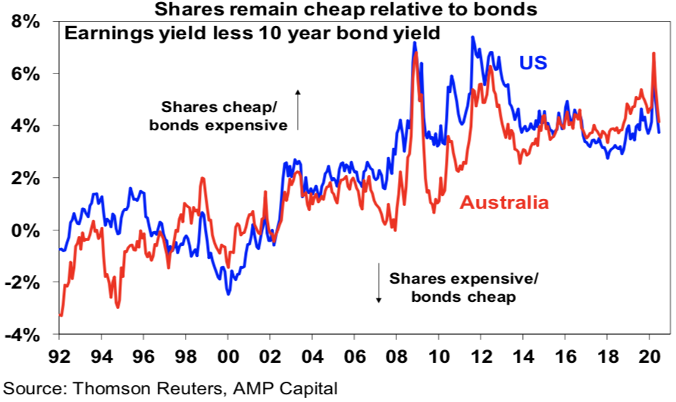

Our final chart shows that with low bond yields and a benign outlook for inflation, equities look reasonable value, especially when compared with low yielding bonds. Of course, this is simply one valuation measure amongst many.

Our view is that SMSFs should stay exposed to growth assets if they are to achieve the return they require to meet their longer term pension liabilities. The exposure to growth assets (mainly equities and property) can be supplemented and balanced by a measured exposure to corporate debt securities. This strategy will encounter price volatility, but that volatility will be caused by short term price movements that have little to do with economic recovery and the predictable path back to a larger and growing economy.

Get investment insights from industry leaders

Liked this wire? Hit the follow button below to get notified every time I post a wire. Not a Livewire Member? Sign up for free today to get inside access to investment ideas and strategies from Australia’s leading investors.

Never miss an update

Enjoy this wire? Hit the ‘like’ button to let us know.

Stay up to date with my current content by

following me below and you’ll be notified every time I post a wire

John has 35 years experience in funds management and corporate advisory services. Prior to establishing Clime, John’s roles included ten years at NRMA Investments as the head of equities.

Clime is a management and advisory business for mainly SMSFs.

4 topics

John has 35 years experience in funds management and corporate advisory services. Prior to establishing Clime, John’s roles included ten years at NRMA Investments as the head of equities. Clime is a management and advisory business for mainly SMSFs.

John has 35 years experience in funds management and corporate advisory services. Prior to establishing Clime, John’s roles included ten years at NRMA Investments as the head of equities. Clime is a management and advisory business for mainly SMSFs.

Comments

Comments

Sign In or Join Free to comment