Afternoon Note: ‘Old School’ stocks lead the gain as the ASX hits new post CV-19 highs

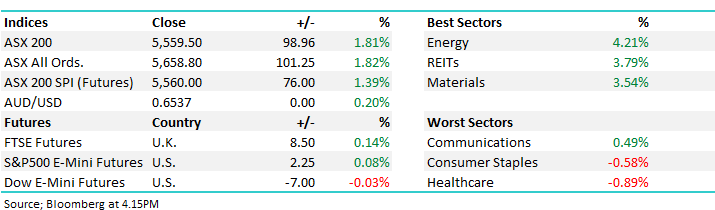

WHAT MATTERED TODAY

A good session for the local stocks buoyed by the +900pt rally on the Dow overnight, however rallies in US stocks of that magnitude haven’t necessarily translated to strong / sustained gains for the local bourse in recent times. We seem to be leading rather than following the US, although they do generally trump the magnitude of our moves on the upside.

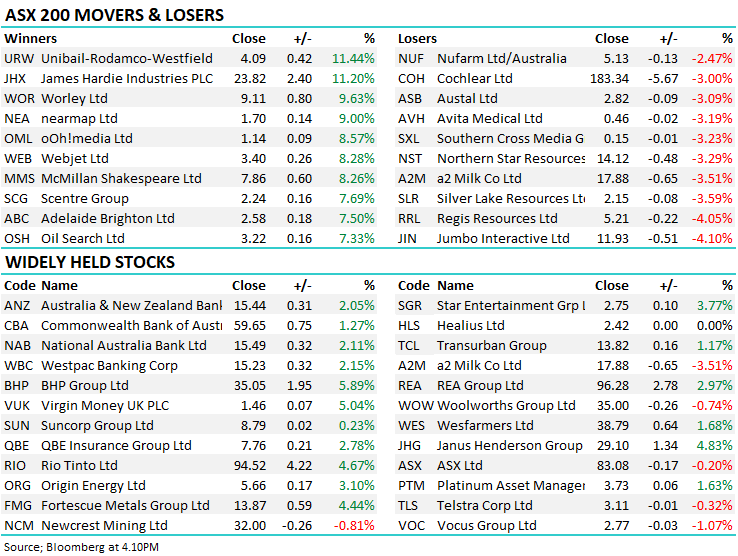

Still, today was a reasonable session, we gave back a touch of the early optimism (-46pts from the morning highs) however some sectors kept their foot to the floor. Energy led the way adding +4.21% while we’re also starting to see ‘Aussie Economy’ stocks doing well, by that I mean building materials (Adelaide Brighton +7.5%), construction (Lendlease +4.95% ), construction / mining services (NRW Holdings +5.25%), property (Stockland +6.03%) and even the retail landlords (Vicinity +6.92%, and Scentre Group +7.69%) all doing well. Materials were also strong led by Iron Ore miners RIO +4.67%, Fortescue +4.44% & BHP +5.89%, the latter obviously benefitting from its exposure to oil which has rallied strongly, the talk of storage capacity and negative futures pricing banished from the headlines.

We’ve been discussing the theme of growth v value in recent notes and the potential for the focus to swing back into the more boring value orientated stocks, the theme showing some signs of playing out overnight (Dow Jones +3.85% v Nasdaq +1.96%) and the same played out today, Afterpay (APT) -0.73% versus old school packaging business Pact Group (PGH) +5.39%. Growth has had a phenomenal run and its understandable why, however as we often say, elastic bands can only stretch so far and we might be seeing the early signs of exhaustion.

I was in the office today and traffic is starting to build back up in Sydney, the trip from Nth Beaches to the city at 6am was getting close to usual traffic + there was more people around about the city today as we move slowly back towards normality, schools back full time in NSW on Monday will be a big change, my youngest can’t wait, my eldest can.

Overall, the ASX 200 added +99pts / +1.81% today to close at 5559 - Dow Futures are trading down -7pts/-0.03%.

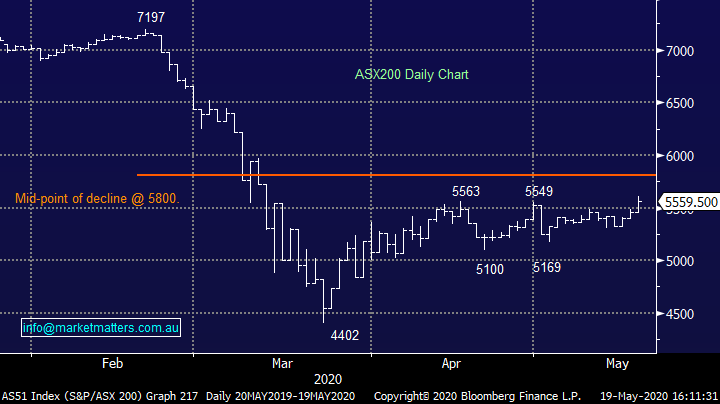

ASX 200 Chart

ASX 200 Chart

CATCHING MY EYE:

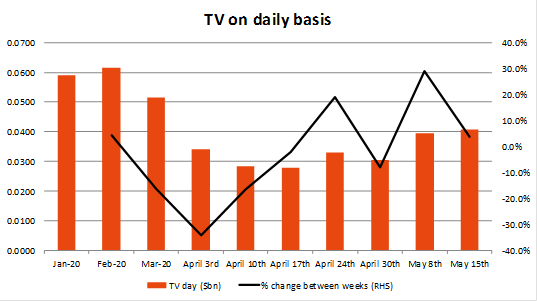

Tyro Payments (TYR) -2.29%: I missed putting this in yesterday however below is the weekly payment stats from the payment provider we’ve been using / writing about as one indicator that was signalling a bottoming / recovery in spending and last week saw more improvement. As we spoke about last Monday the turning point was in the week of April 17th and payment volumes are now 47% higher than that period. Tyro is one of the fastest growing technology terminal businesses in Australia with the bulk of their transactions in the hospitality and tourism space, hence is a good raw indicator of trends here.

Key takeout’s from our tech analyst at Shaw Jono Higgins.

· May 15th weekly TV of $409m a day, up 4% on the week prior and up 47% on same period last month;

· YoY growth now -20% in April, versus a low of -43% in April. Decline still there at ~-40-50% on previous growth rates YoY. However delta is positive; and

· Expect positive traction into EOFY. This is likely to be broadly supportive of businesses with a structural change and speciality retail/omni channel experiences.

Source: Shaw and Partners

James Hardie (JHX) +11.2%: Reported full year results today that were a bit better than expectations in terms of revenue and inline in terms of underlying operating profit (~$353m), however the commentary was upbeat. Hardies talked up the strong 12 months just gone and good momentum that continues, they said March volumes were good, cost outs going well and they were ultimately a lot more upbeat about the COVID-19 slowdown. They provided no guidance and scrapped the dividend however the underlying tone of the update was on the positive end of the spectrum. The market is bearish this stock, consensus implies a decline in earnings for FY21 of ~20% and it simply didn’t feel like the company was experiencing such weakness.

James Hardie (JHX) Chart

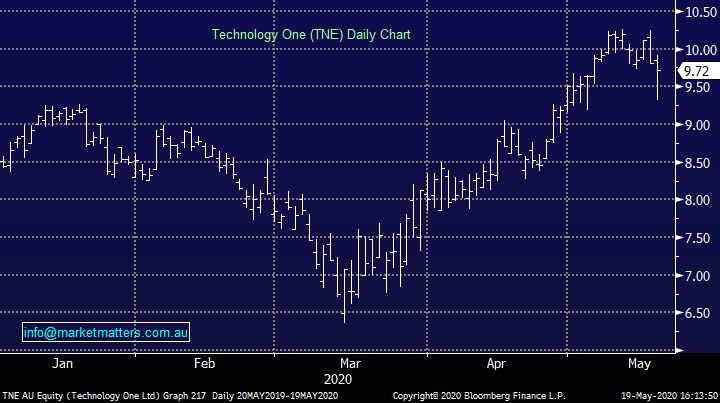

Technology One (TNE) -0.92%: the software as a service (SaaS) business announced first half results today with profit up 6% to $19.1m after tax, helping lift the interim dividend 10%. The company builds business processes software for a range of corporates, government divisions and education providers to name a few. The ongoing subscription like fees collected for their offering generates more than 85% of revenues helping maintain the stability of earnings through the pandemic. With their software enabled for a work-anywhere approach, the Chairman making key mention of the streamlined nature of the set up highlighting the benefits of a “true digitally enabled solution.”

The push into the UK is the main growth frontier for TNE at this stage, with the new geography posting a small loss for the period of $800k, though this was down from a bigger loss in the 1st half last year. Given the evolving situation, the company guided to pre-tax profit growth of 8-12% with the market already pricing in the top end of the range. TNE offers a great product in an industry with years of growth ahead of it. The stock looks a little punchy here, though one to keep an eye on into any weakness.

Technology One (TNE) Chart

Appen (APX) +0.20%: hosted a technology day today, inviting the market for a closer look at the company’s AI offering and the opportunities that exist for it. Back in April, APX re-confirmed EBITDA guidance for the full year of $125-130m though they sighted a key factor that would boost the performance could be a weak AUD. Since then the Aussie battler has moved higher and looks set to press on if the commodity tailwind remains. Back to Appen though, the company didn’t announce anything new to the market, more just an education day for investors talking to the basics of building out a data set through to the scalability of the technology. A great company, but may struggle in the face of a higher Aussie dollar as well as slowing digital marketing spend or reduced interactions lowering the rate of data-collection.

Appen (APX) Chart

BROKER MOVES:

- Perseus Raised to Buy at Citi; PT A$1.40

- Dacian Gold Raised to Speculative Buy at Canaccord

- Ramsay Health Cut to Sell at Morningstar

- Elders Cut to Hold at Morgans Financial Limited; PT A$10.20

Major Movers Today

Have a great night

James

Never miss an update

Enjoy this wire? Hit the ‘like’ button to let us know.

Stay up to date with my current content by

following me below and you’ll be notified every time I post a wire

James is Director & Lead Portfolio Manager at Market Partners - a collective of highly experienced investment professionals, operating independently, managing discretionary portfolios for wholesale investors.

James is also Portfolio Manager & primary author at Market Matters, a digital advice & investment platform with over 2500 members that offers real market intel & six portfolios open for investment.

........

Any advice provided is of a general nature only.

14 stocks mentioned

James is Director & Lead Portfolio Manager at Market Partners - a collective of highly experienced investment professionals, operating independently, managing discretionary portfolios for wholesale investors. James is also Portfolio Manager &...

Expertise

James is Director & Lead Portfolio Manager at Market Partners - a collective of highly experienced investment professionals, operating independently, managing discretionary portfolios for wholesale investors. James is also Portfolio Manager &...

Expertise

Comments

Comments

Sign In or Join Free to comment