“Anything can happen, at any time.”

“Anything can happen, at any time.” - Joseph Goldstein, Buddhist teacher and author

So far this year, avoiding the torrent of events in public health, economies, geo-politics and financial markets has been like trying to stay dry under Niagara Falls by dodging water. We have all had a brutal reminder that, “Anything can happen, at any time!”

For investors today, one of the biggest problems is that the world is awash with uncertainty. What makes things worse is that the usual signals are sending out mixed messages.

For example, stock markets are up strongly from the lows even as we are seeing the negative consequences of the lockdown. An equity index may not be the real world, but the current disconnect between plunging economic indicators and rising share prices seem extraordinary.

The good news is that history has repeatedly shown that things will improve, and that this improvement will incorporate a more consistent relationship between financial markets and economies. However, blind optimism helps no-one, and between now and any resolution there will be some dangerous moments.

One immediate challenge is that money supply in the US is about to peak and will largely be offset by fiscal issuance of debt.

As I have discussed elsewhere, broad US equity indices like the S&P 500 and the Nasdaq Composite are expensive and rely disproportionately on the performance of a few equities such as the trillion-dollar stocks Apple, Microsoft, Alphabet and Amazon. How these indices will behave as the liquidity tap is tightened is far from clear.

In the third quarter, we will start to see how consumer behaviour is actually affected as government measures to help employees taper or come to an end. JobSeeker in Australia, direct cheques in the US and the furlough system in the UK, for example, have been instrumental in supporting consumer demand. With little clarity on the appetite for hiring versus firing, it is difficult to know how big the impact of these schemes’ coming to an end will be.

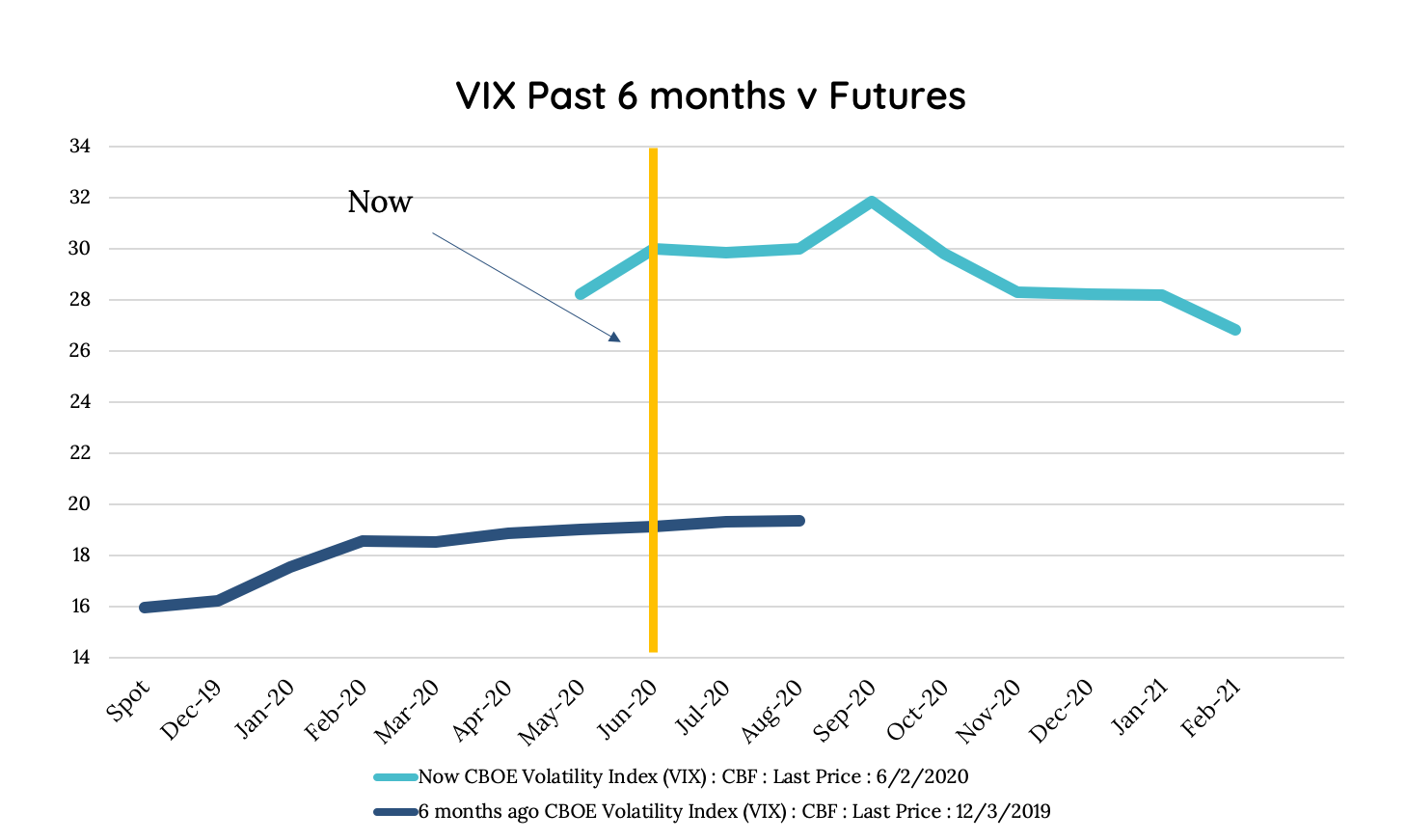

In addition, there is uncertainty over further waves of the Coronavirus, US-China trade relations, the US elections, the state of the crude oil market, and so on, which has seen a spike in the Volatility Index (VIX) futures.

Perhaps the biggest question of all is who is going to fund the government debt that is being raised to counter the pandemic. The scale of issuance is eye-watering, with the Treasury asking for buyers for over a trillion US dollars of bonds at depressed yields – and that’s just this year!

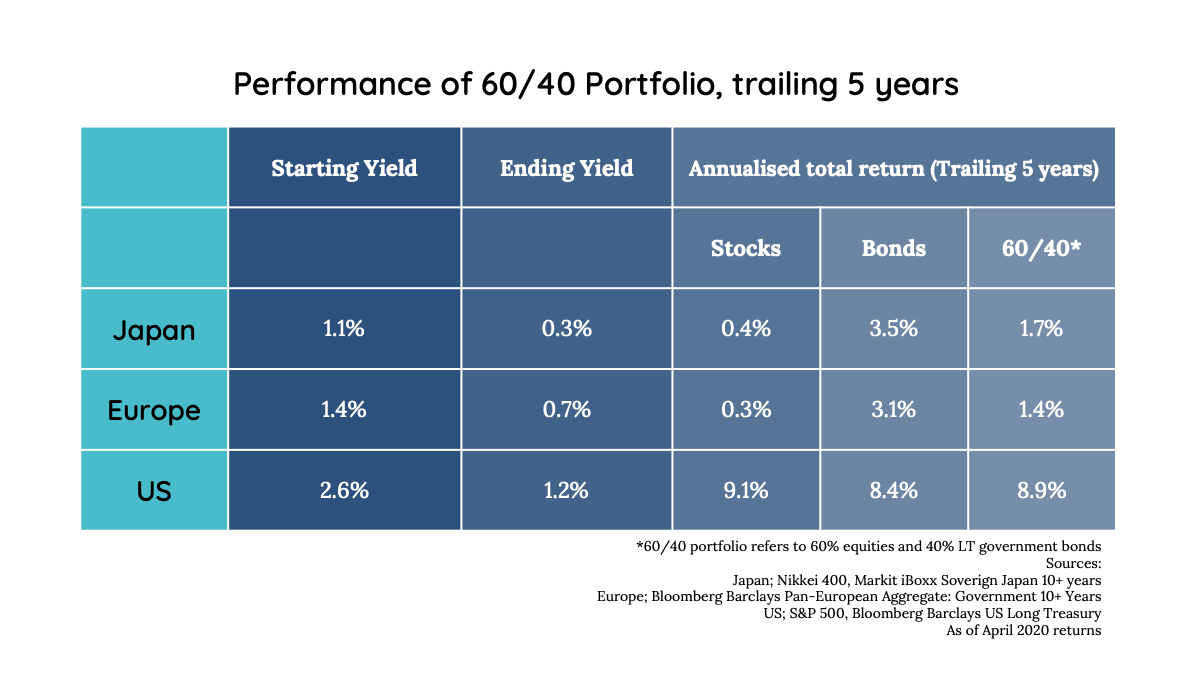

For investors, the outlook for US long bonds, also known as Treasuries, is crucial given the prevalence of the 60/40 portfolio, which has been fundamental to the savings of retirees for years. This structure puts 60% of a portfolio in equities and 40% in bonds.

Treasuries have more than played their part.

For example, over the last five years, the annual total return from Treasuries has kept up with US equities and outshone equities and bonds in Europe and Japan (table below). Yet it would seem brave to assume that US bonds can continue punching above their weight, as yields are at historical lows, and with so much supply on the way, that’s unlikely to change for some time.

So one way out for retirees and other investors lies in a different approach. They should consider funds with strategies that use equity options to provide outcomes that are not reliant on corporate dividends or government bonds, but still provide reliable income and exposure to the inevitable upturn.

Investing in good companies with strong balance sheets creates greater certainty to withstand future shocks, while getting paid a premium to enter the stock trade via put options locks in income.

This way, while anything can happen at any time, investors can have more certainty about their futures...and the journey there.

Never miss an update

Enjoy this wire? Hit the ‘like’ button to let us know.

Stay up to date with my current content by

following me below and you’ll be notified every time I post a wire

Chad is the Co-Chief Investment Officer and co-founder of Talaria Asset Management. He has more than 21 years of experience in the financial services industry in the UK, South Africa and Australia. Talaria's investment strategy seeks to increase the certainty of global equity returns for investors through its:

> Unique and structurally lower-risk investment approach that combines capital growth and income generation to deliver a more consistent return profile (smoothing).

> Portfolio of up to 45 large, globally listed companies.

> Internationally experienced and personally invested leadership team.

www.talariacapital.com.au

........

The information in this article is general information only and is not based on the objectives, financial situation or needs of any particular investor. In deciding whether to acquire, hold or dispose of the product you should obtain a copy of the current Product Disclosure Statement (PDS) for the Fund and consider whether the product is appropriate for you.

Wholesale Units in the Talaria Global Equity Fund (the Fund) are issued by Australian Unity Funds Management Limited ABN 60 071 497 115, AFS Licence No. 234454. Talaria Asset Management Pty Ltd ABN 67 130 534 342, AFS Licence No, 333732 is the investment manager and distributor of the Fund. References to “we” means Talaria Asset Management Pty Ltd, the investment manager. A copy of the PDS is available at australianunity.com.au/wealth or by calling Australian Unity Wealth Investor Services team on 13 29 39. Investment decisions should not be made upon the basis of the Fund’s past performance or distribution rate, or any ratings given by a rating agency, since each of these can vary. In addition, ratings need to be understood in the context of the full report issued by the rating agency itself. The information provided in the document is current at the time of publication.

5 topics

Chad is the Co-Chief Investment Officer and co-founder of Talaria Asset Management. He has more than 21 years of experience in the financial services industry in the UK, South Africa and Australia. Talaria's investment strategy seeks to increase...

Expertise

Chad is the Co-Chief Investment Officer and co-founder of Talaria Asset Management. He has more than 21 years of experience in the financial services industry in the UK, South Africa and Australia. Talaria's investment strategy seeks to increase...

Expertise

Comments

Comments

Sign In or Join Free to comment

most popular

Equities

The Magnificent Seven can’t carry the market forever

Pzena Investment Management