Are the supermarkets a better bet than their landlords?

Both areas of the market offer reasonable yields, the Supermarkets are fully franked, the landlords aren’t however the main question should be around earnings and importantly, the outlook for those earnings over the foreseeable future.

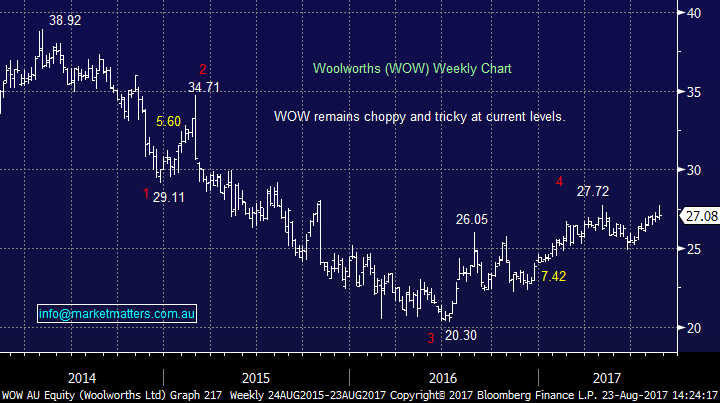

This morning Woolworths (WOW) reported numbers that were a tad light on in aggregate, however there were some swings and roundabouts. Divisionally, the food and liquor business (69% of earnings) did really well in terms of growth with top line revenue up by 5% and the critical like for like sales (LFL) number up by a very strong 6.4% in 4Q17 (above market expectations of 5.5%), continuing the accelerating trend of the last 3 quarters (1Q +1.7%, 2Q +3.1%, 3Q +4.5% 4Q +6.4%). That said, this growth is clearly coming at the expense of margins which were down from 4.6% to 4.2% as aggressive price reductions start to bite. Woolies have clearly addressed their growth issues, and are getting customers through the door, which is a positive however it gets harder from here. We have no interest in WOW at current levels

Woolworths Weekly Chart

Last week it was Wesfarmers (WES) that delivered an overall result that was in line with market expectations, however Coles is obviously the dominate area of that business accounting for 36% of earnings (followed closely by Bunnings contributing 28%). The Coles result was actually good with like for like sales growth of 1.2%, snapping 4 straight quarters of declines (Q1 2.8%, Q2 1.8%, Q3 0.9%, Q4 0.7%) – importantly the result was better than market expectations of 0% to 1.0% however Coles margins continued to be under pressure from continued price reductions – down from 4.7% to 4.1%.

This is the conundrum faced by both supermarkets at the moment as competition increases. Hold prices to maintain margins and get lower sales, or cut prices, reduce margins and get good growth – clearly it’s a balancing act. We hold Wesfarmers in MM Income portfolio from lower levels and picked up the dividend yesterday. On 15.5 times and a yield of 5% this looks reasonable, however with competitive pressures building, an outlook that was typically vague and non-committal (as usual), we’re not high conviction holders of WES at this juncture. A move up towards $45 and we’d be likely sellers.

Wesfarmers Weekly Chart

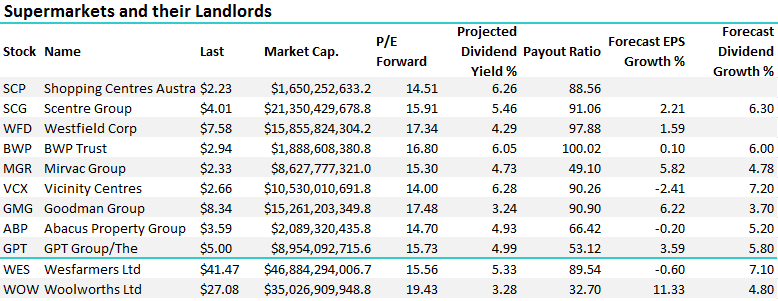

The landlords on the other hand have mostly reported strong numbers during recent results,better than the market feared with many forecasting reasonable growth to come in FY18. In terms of our universe, below is a quick snapshot of the stocks we track that have exposure to Supermarkets in some capacity, although it must be acknowledged that the majority do have diverse exposures in many areas of the property spectrum.

Source; Bloomberg / Shaw and Partners

Taking a step back in time for a moment, investors will most likely remember the sector as one that felt some serious pain during the GFC, with a number of companies going broke (think Centro). They first starting getting the wobbles in 2007, when trusts in the sector fell an average of 8.4%, which was the sector's first negative year in eight years however in 2008 selling really kicked in – and they dropped 55%. You could be excused for righting off the sector since that time.

Gearing was the key issue going into the GFC - the average level of gearing jumped from about 15% in the 1990s to a peak of close to 45% in 2006 and 2007. Combine that with falling asset prices and the debt markets which effectively froze, some managers were simple unable to refinance. Fast forward to now, gearing in the sector is now a reasonable 27%, so clearly not stretched however asset values have also risen. After a good run for many since the GFC, the outlook now is less certain and some the REITS have declined – some substantially, in the last 12 months or so. Below is our take;

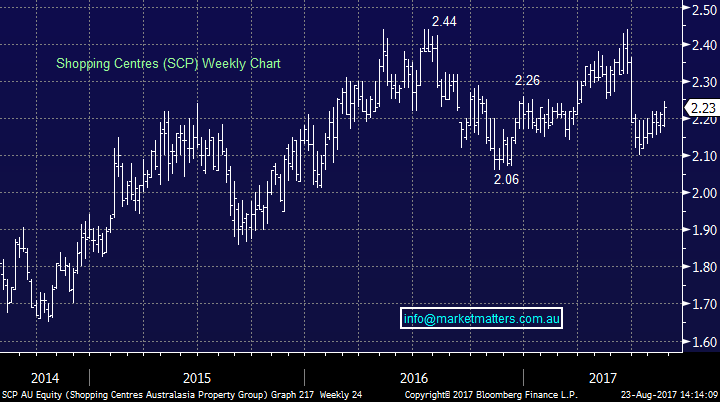

SCA (SCP) is focused on investment in neighbourhood and sub-regional shopping centres operating properties across Australia. Tenants are mostly non-discretionary retailers, anchored by long term tenants of Woolworths and Coles (WOW contributing 34% of gross rent and Coles 10%) . In their recent results, they showed pretty high occupancy in its portfolio and is still generating positive rental growth as well as sales productivity despite the challenging retail environment. Good yield, reasonable valuation however it’s hard to get excited about regional exposures at this stage. Technically, we can see an eventual test of ~$2

SCA Property Weekly Chart

Scentre Group (SCG) is a retail developer and landlord born from 2014 restructure of Westfield, SCG manages over 11,500 retail outlets within the 39 Westfield shopping centres it owns in Australia and New Zealand. With another 7 developments in the pipeline, SCG is betting big on the longevity of instore retailing. We liked it technically as it came back over $4.10 but would probably now be stopped out….no signals here

Scentre Group Weekly Chart

Westfield (WFD) is an international based landlord/developer focussed on US shopping centres, or malls as they call it, with assets in the UK/Europe and developments around the world. With reporting done in USD and most of Westfield’s earnings coming from the US, WFD is heavily exposed to the USD. We’ve been bearish WFD and called this a SELL nearer $11 however on 17x, a yield of 4.29% and exposure to a US economy that will feel the brunt of higher interest rates in the months ahead, there is very little to like about WFD here. Interestingly, and obviously this is US centric, they showed overall rental growth of 9.1%, with 10.6% growth in its flagship portfolio (cities) and 1.3% in its regional portfolio – the US is ahead of Oz in the cycle and we think this trend is a good read through for the regionally exposed REITs. Remains bearish

Westfield Weekly Chart

BWP’s 80 assets are large format retail sites, predominately leased to Bunnings Warehouse along with some smaller retail space on some sites. Clearly BWP’s assets are targeted to a specific type of retailer and a different play on the REIT space. Looking forward BWP expects to maintain its DPS at least at 17.51¢ in FY18 - possibly assisted by the distribution of capital profits from asset sales. Technically bearish.

BWP Weekly Chart

Vicinity Centres (VCX) run a direct investment portfolio owning a number of neighbourhood convenience based shopping centres, alongside an external FUM business that manages close to $10bil of assets for 3rd parties. While the portfolio is similar to SCA, the FUM business adds a reasonably secure income stream to VCX. There are some concerns in the market about their asset quality, which we don’t agree with, and importantly, we don’t think the mkt is ascribing much value (if any) to their funds business. This is a cheap stock and is a key pick for those wanting exposure here. Technically, VCX can be bought here with stops under $2.45.

Vicinity Centres Weekly Chart

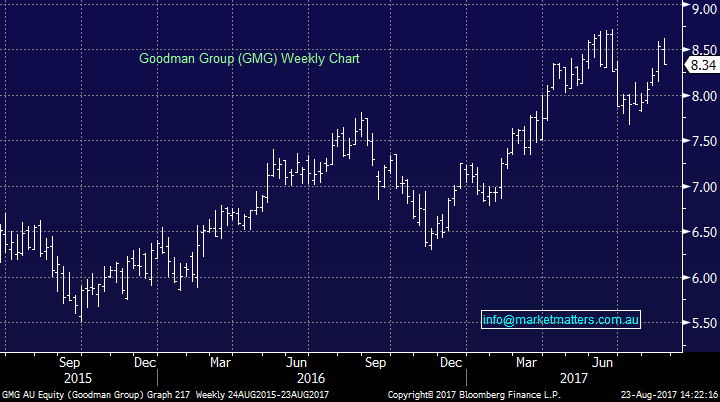

Goodman Group (GMG) is a global integrated property group that have operations across 4 continents within four property divisions – Investment, FUM, Services and Development. GMG is a dominant player in the REIT market but is currently shifting from development to property management focussed business. GMG is extremely well capitalised (2.1bn in cash) so has plenty of options for future growth, probably more so by attracting external FUM. We are neutral here

Goodman Group Weekly Chart

Abacus (ABP) has a diversified property portfolio across Australia’s office, retail, industrial/logistics and self-storage space. ABP is more focussed on the office and self-storage businesses with no new retail developments and around 25% of the ABP portfolio in retail space. A cracking recent result and the stock is performing on the back of it. Nice breakout….could be long with stops under $3.40

Abacus Weekly Chart

GPT Group (GPT) has a similarly diversified portfolio to ABP, with a higher skew towards retail leasing. With centres like Norton Plaza in Leichardt, most properties have a long term supermarket tenant alongside discretionary retailers. We are neutral here

GPT Weekly Chart

Mirvac (MGR) another diversified property group that manages assets in the major cities in Australia. Many of the Mirvac developments combine office, retail and residential space to help maintain occupancy – and supermarkets have a place in this, however their exposure to residential development means we have little interest. Technically, MGR looks strong with stops under $2.15, however it is at top of the range

MGR Weekly Chart

Conclusion (s)

Neither supermarkets or their landlords are attractive from a thematic standpoint. Rising interest rates will hurt property stocks and rising competition and reduced spending power will clearly hurt the supermarkets.

We own Wesfarmers in the income portfolio and inclusive of the dividend we are sitting on a nice 6% profit. Although this is a solid exposure, we see little scope for long term growth in the dividend given competitive pressures. We will look to sell WES nearer the top of its trading range ~$45

In the ‘landlord space’ we like Vicinity Centre (VCX) on most metrics, while Abacus (ABP) is also worth considering.

Never miss an update

Enjoy this wire? Hit the ‘like’ button to let us know.

Stay up to date with my current content by

following me below and you’ll be notified every time I post a wire

James is Director & Lead Portfolio Manager at Market Partners - a collective of highly experienced investment professionals, operating independently, managing discretionary portfolios for wholesale investors.

James is also Portfolio Manager & primary author at Market Matters, a digital advice & investment platform with over 2500 members that offers real market intel & six portfolios open for investment.

1 topic

10 stocks mentioned

James is Director & Lead Portfolio Manager at Market Partners - a collective of highly experienced investment professionals, operating independently, managing discretionary portfolios for wholesale investors. James is also Portfolio Manager &...

Expertise

James is Director & Lead Portfolio Manager at Market Partners - a collective of highly experienced investment professionals, operating independently, managing discretionary portfolios for wholesale investors. James is also Portfolio Manager &...

Expertise

Comments

Comments

Sign In or Join Free to comment

most popular

Investment Theme

If 24 LICs ran the Melbourne Cup, which ones would we back?

Affluence Funds Management