As a decade of ‘easy money’ draws to a close, is it time to refocus attention on sovereign credit risk?

Over the last decade highly accommodative monetary policy has allowed governments around the world to sustain increasing debt levels without too many issues. With the world gradually moving away from a decade of ‘easy money’ it may be time for investors to refocus on the risks associated with sovereign debt.

Types of sovereign credit risk

When considering sovereign credit risk it is worth distinguishing between two types of sovereign default risk. Firstly, legal default whereby the sovereign issuer seeks to alter the terms of the original contract through either a rescheduling or repudiation of financial obligations. Ultimately a legal default results in a reduction in the nominal returns earned by creditors through the realisation of capital losses. The alternative form of default can be referred to as ‘economic default’. This is where the sovereign issuer pursues actions/policies with the aim of reducing the real return earned by creditors through either inflation, currency depreciation or some other form of financial disadvantage.

It is the potential for ‘economic default’ which results in sovereign credit risk having similarities with corporate credit risk but importantly not being identical. Critically there are a range of factors rather than just the level of debt which ultimately determines whether a sovereign default actually occurs. These can be divided broadly into factors determining the ‘ability to pay’ and the ‘willingness to pay’. This highlights a distinction between the credit risk of corporates versus sovereigns. The assessment of corporate credit risk is largely focused on ‘ability to pay’. This arises as default for a corporate bond is usually more clearly defined with trust indentures and general legal principles setting out criteria that assist in defining not only what constitutes a ‘legal default’ but also creditors rights. By comparison, as creditors have only limited legal redress against governments, a government can default selectively on its obligations even when it possesses the capacity for timely debt service. As such, sovereign risk reflects both the ability and, potentially more importantly, the willingness of the sovereign issuer to meet its obligations to individuals or groups of creditors.

Why is this important now?

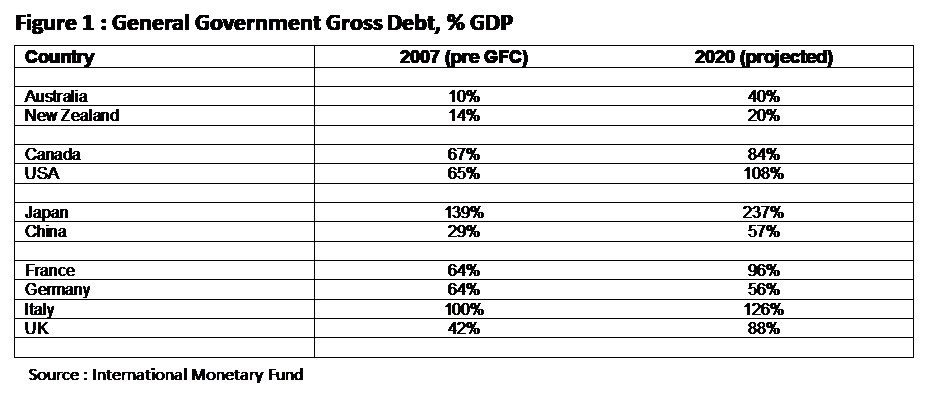

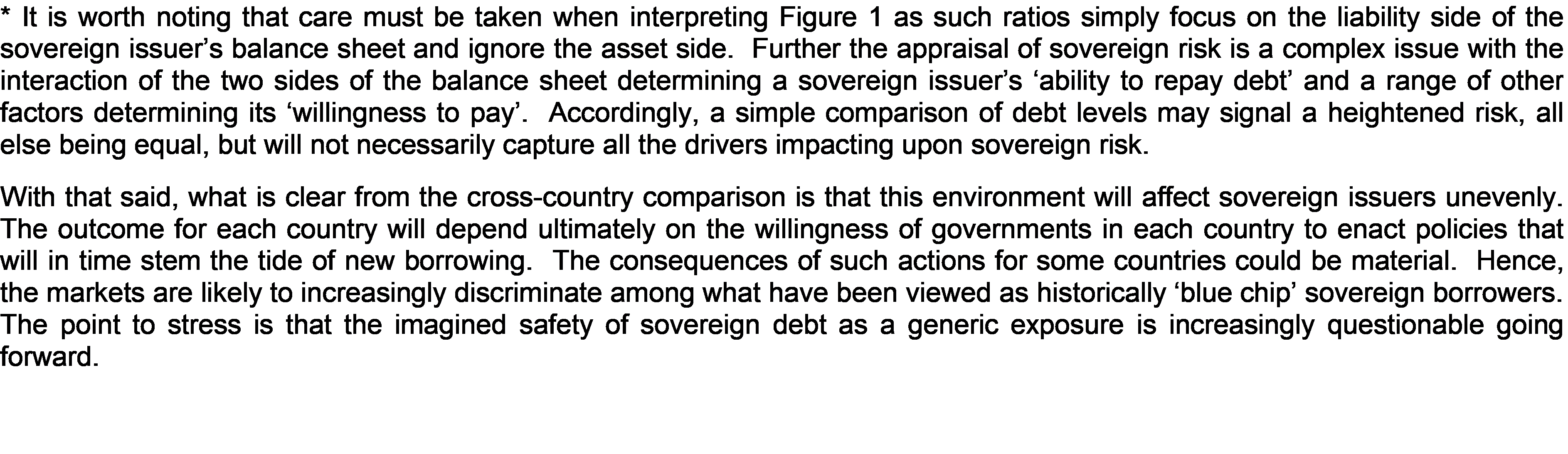

The decade post the Global Financial Crisis in 2008 has resulted in governments materially increasing the level of borrowings. While overall debt to GDP has grown for all countries it hasn’t been consistent with countries such as Australia and New Zealand remaining materially below other developed countries (see Figure 1).

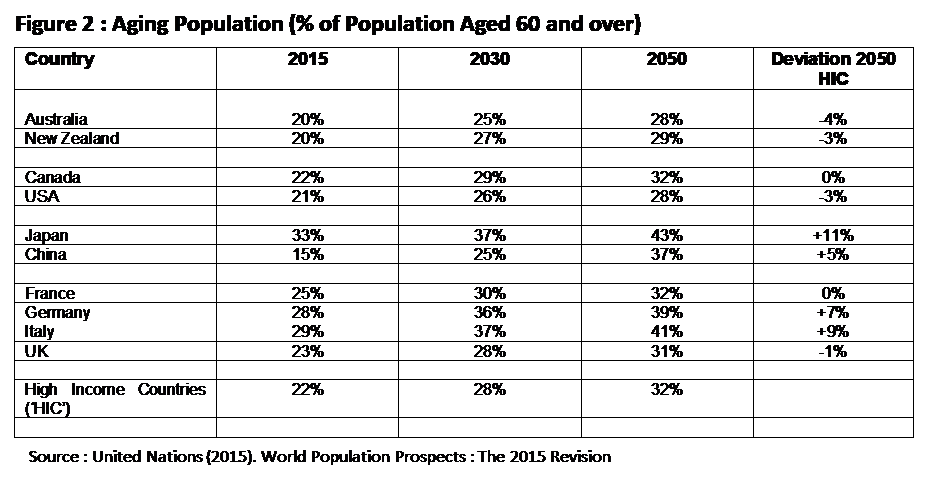

On the back of easy global liquidity conditions and relatively solid economic growth the ability to service such debt levels has not proven to be a material issue to date. The concern is that the decade of easy money is likely to be drawing to an end which may not only slow economic growth but will also increase funding costs. This dilemma is even more acute due to demographics. Not only are populations aging in general, thereby putting greater pressure on unfunded government liabilities, arising from pension and health care costs, but this is occurring at different rates across countries (see Figure 2). How the costs of adjustment are spread among the various constituents remains the key uncertainty going forward which augments sovereign risk *.

Implications for Investors

As the world moves on from the decade of easy money investors are increasingly likely to focus upon the sovereign credit risk associated with countries dealing with the rising debt levels and the evolving fiscal implications of an aging population. Though many of these factors may be ‘slow burn’ in nature there are several key points which investors need to keep in mind going forward when considering sovereign bonds:

- Though ‘legal default’ for well rated sovereigns is still unlikely, the more important risk is that of ‘economic default’ as sovereign issuers seek ways to ‘more fairly’ distribute the costs associated with reducing the level of debt. In this situation measures such as allowing higher inflation or currency depreciation are just as real an enemy to the effective returns earned by bond investors over time as ‘legal default’.

- Certain countries stand out as maintaining materially better fiscal and demographic positions than others. Such differences in risk characteristics should be explicitly considered by investors when deciding how much of their assets to allocate to domestic versus global sovereign assets. Greater caution should accordingly be exercised by investors who may be reallocating from domestic sovereign markets which exhibit relatively strong fundamentals to foreign sovereigns which may exhibit materially weaker characteristics.

- Where investors have global sovereign exposures the ability to pro-actively manage these exposures as events evolve becomes an increasingly important tool to assist in the preservation of the value of their investments in both nominal and real terms.

Increasingly the ability to assume that sovereign risk for developed countries is a generic low risk exposure will come under pressure. This has implications for investors when determining not only the relative attraction of exposures to domestic versus global bond markets but also whether the composition of any global exposures remain consistent with their investment objectives. Going forward, as government finances face growing headwinds, investors will need to be more selective regarding the type of government exposures assumed to maintain the low risk characteristics historically associated with this asset sub class.

Never miss an update

Enjoy this wire? Hit the ‘like’ button to let us know.

Stay up to date with my current content by

following me below and you’ll be notified every time I post a wire

By

Clive Smith,

Clive Smith is an investment professional with over 35 years experience at a senior level across domestic and global public and private fixed income markets. Clive holds a Bachelor of Economics, Master of Economics and Master of Applied Finance degrees from Macquarie University and is a CFA ® charterholder.

1 topic

Clive Smith is an investment professional with over 35 years experience at a senior level across domestic and global public and private fixed income markets. Clive holds a Bachelor of Economics, Master of Economics and Master of Applied Finance...

Expertise

Clive Smith is an investment professional with over 35 years experience at a senior level across domestic and global public and private fixed income markets. Clive holds a Bachelor of Economics, Master of Economics and Master of Applied Finance...

Expertise

Comments

Comments

Sign In or Join Free to comment