Aussie major banks look expensive

David Gallagher

Artesian

The recent volatility in global corporate bond markets has caused some long-standing pricing relationships to dislocate. In this piece we will highlight why a) US issuers eligible to be purchased by the US Federal Reserve (The Fed) look cheap in AUD, and b) why major bank senior spreads look expensive in AUD.

US issuers cheap in AUD

The Fed announced March 23rd 2020 that it would launch two credit facilities to provide support for its corporate bond market. There is a total of ~USD 10 trillion of corporate debt in the US ranging from bonds to loans.

The Fed adopted a two-pronged approach through its Primary Market Corporate Credit Facility (PMCCF) for new bond and loan issuances, and a Secondary Market Corporate Credit Facility (SMCCF) to provide liquidity for outstanding corporate bonds.

The Fed announced it will purchase corporate bonds that are investment grade (rated BBB- or higher) and or US-listed exchange-traded funds that hold similar securities, focusing on corporate bonds with less than 5yrs maturity. April 9th the Fed then announced that they will also consider buying junk bonds, securities rated BB+ or lower. The focus of this piece will be on the investment-grade market.

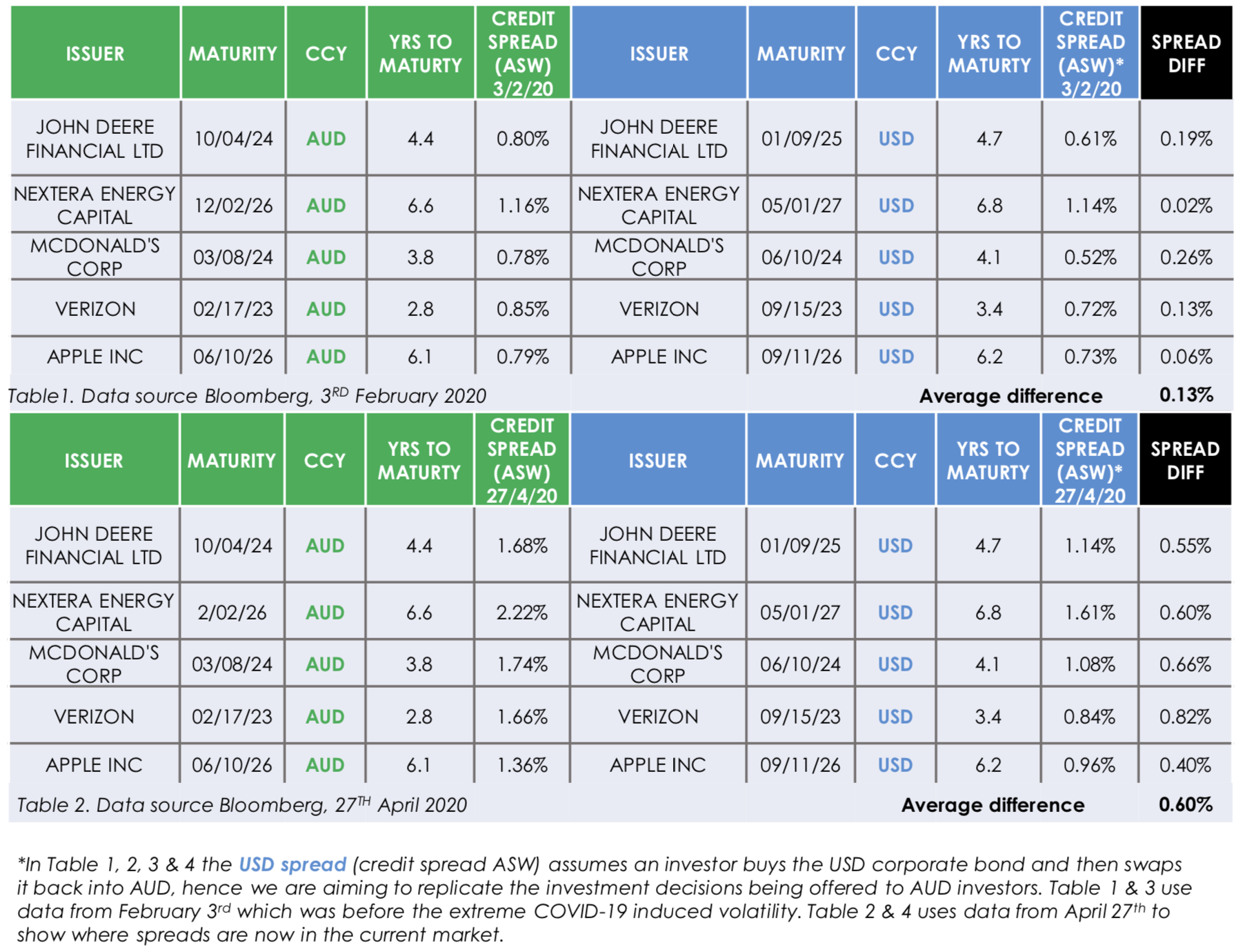

Unsurprisingly, the market took the news on March 23rd very well and USD corporate bonds reversed some of the weakness witnessed throughout March. That trend has continued, and corporate bonds eligible to be purchased by the Fed have outperformed corporate bonds ineligible to be purchased through the Fed’s PMCCF and SMCCF programs. What we are now seeing is a pricing dislocation in US issuers in AUD versus comparable bonds of a similar maturity in USD. Below we have highlighted a handful of US issuers who have AUD corporate bonds. In the far right column we highlight the spread difference between the two similar securities.

US issuers usually trade at a lower, tighter spread in USD because the USD market is more liquid and an illiquidity premium is attached to US issuers in AUD. Due to the increasing demand for Fed eligible securities, we are now starting to see an increase in demand for US eligible issuers in AUD. To be clear, the Fed’s program only includes USD corporate bonds, so we aren’t expecting the Fed to buy US issuers in AUD, however, on a relative value basis some US eligible issuers in AUD are now very cheap compared to their USD maturity equivalent bonds.

We expect over time for the spread differential in these corporate bonds to mean revert from the present April 27th average spread differential in Table 2 of ~0.60% to the average spread differential pre coronavirus of ~0.13%

Aussie major banks expensive in AUD

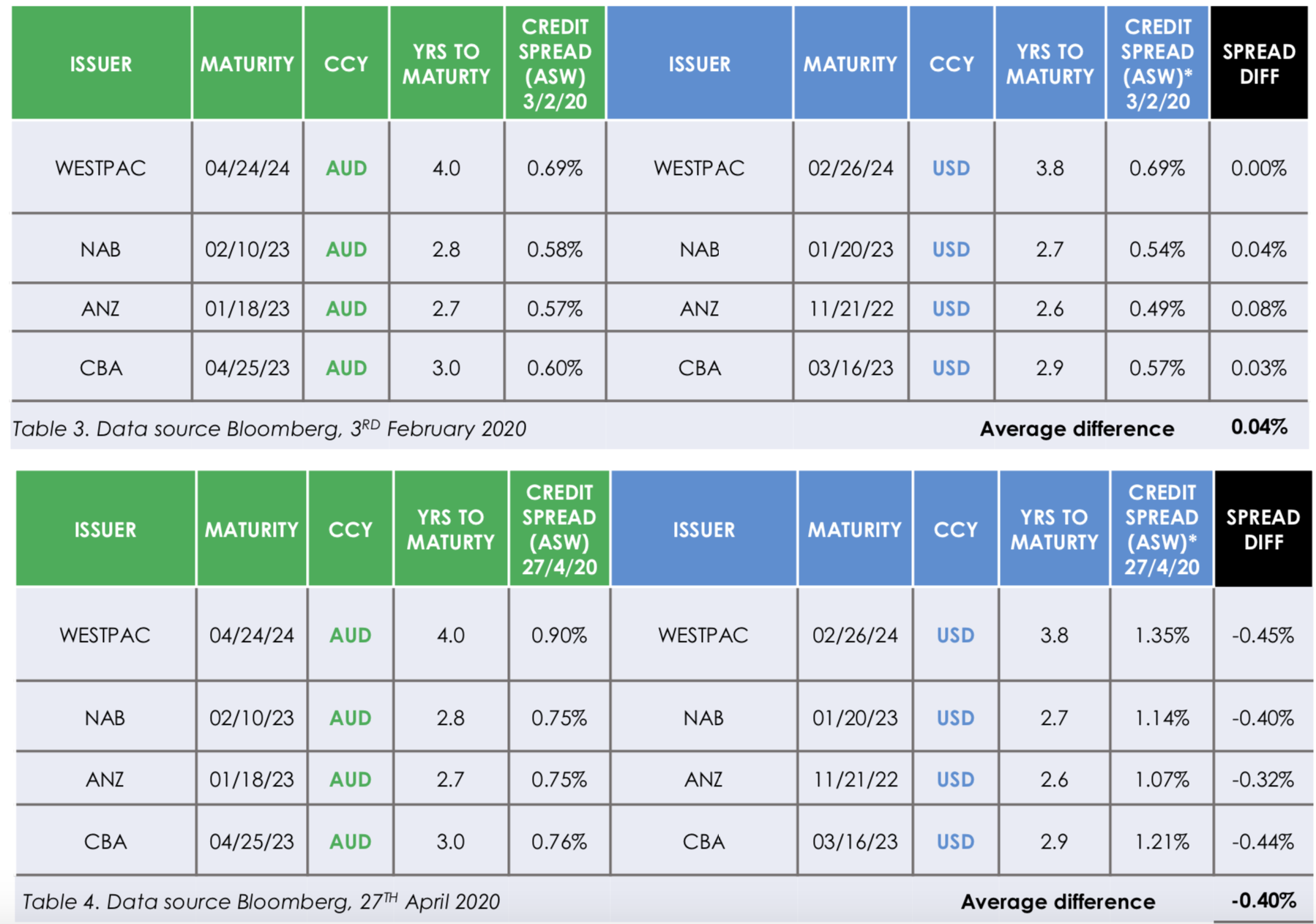

In the financials sector post COVID-19, Australian major bank senior credit spreads are starting to look quite expensive versus their equivalent spreads in USD. Prior to the COVID-19 volatility, Australian major bank spreads traded very close to the same spreads investors could expect if they bought a similar USD bond and swapped it back into AUD. Because AUD Australian major bank bonds are the most liquid corporate bonds in the AUD market, they don’t usually have an illiquidity premium like non-financial corporate bonds. Table 3 data sourced from Bloomberg February 3rd, shows us the average difference between the AUD and USD spreads (swapped back into AUD) was 0.04%.

Post COVID-19 highlighted in Table 4, major bank senior spreads are now trading ~40bps tighter than the USD equivalent bond. This is due to a few reasons, namely;

- New issuance volumes in AUD have fallen off a cliff since COVID-19, as major banks are the most liquid bonds in the AUD market, investors have been more comfortable buying major banks than they have other financials or non financial corporate bonds

- The RBA introduced the Term Funding Facility to Support Lending to Australian Businesses (TFF) on March 19th and major banks bonds along with many other ADI’s were eligible to be sold back to the RBA under a repurchase arrangement

- As the USD market is much larger and more liquid, financials and non-financials trade at spreads which represent a closer fair value spread relative to their peers, therefore investors aren’t overpaying for the liquidity premium attached to major banks in AUD

Therefore, when the AUD market normalizes and historical spread relationships begin to mean revert, owning major bank senior bonds right now (other than for liquidity purposes) seems expensive.

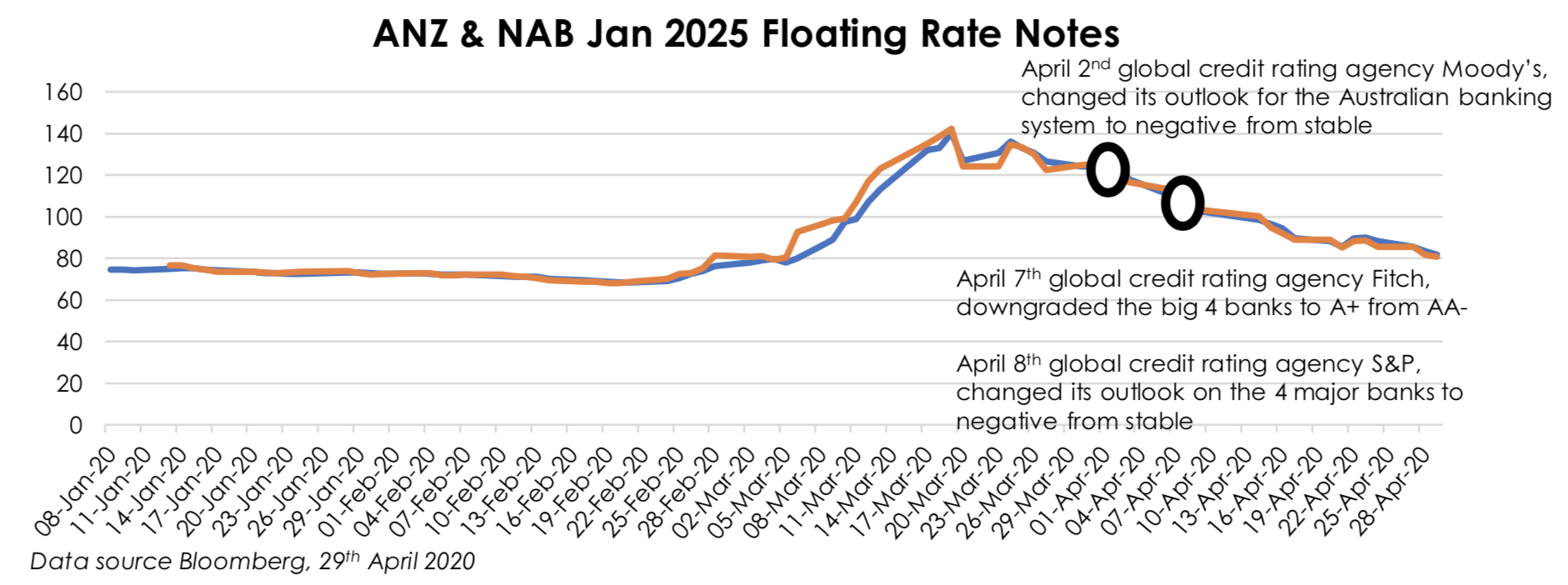

In January 2020, ANZ issued a 5yr FRN at BBSW +76bps and NAB issued a 5yr FRN at BBSW +77bps. Both of these bonds are still considered the “on the run 5yr” major bank senior bonds because none of the big 4 have issued since January. The graph uses data from Bloomberg which is their daily closing prices. The daily closing price is compiled from a quorum of prices and doesn’t necessarily reflect where these bonds may have actually traded on any given day. That information is not given to Bloomberg. We did see these bonds being quoted in the BBSW +160bps to BBSW +180bps region and a market maker told us he was aware they traded at BBSW +200bps.

Where are they now? Basically unchanged from where they were pre COVID-19! A lot has happened since then!

Some of the recent news reported in response from the banks in relation to the COVID-19 impact;

- Westpac will take a $2.2 billion provision for bad debts and COVID-19 related charges

- NAB will take a $807 million provision for bad debts and COVID-19 related charges

- ANZ is expected to take a $1.5 billion provision for bad debts and COVID-19 related charges hit when it releases its half-yearly numbers on Thursday

In addition, global rating agencies have either begun downgrading the major banks or putting them on negative watch. The outlook for the major banks is challenging, yet the real impacts and longevity of COVID-19 related charges are unknown.

What we do know, is that the market is pricing major bank senior debt as if COVID-19 never happened.

Conclusion

Elevated volatility inevitably creates opportunities for investors willing to take a long term view on asset prices. Based on our analysis, largely because of the liquidity/illiquidity premium, the AUD market is currently trading expensively in major bank senior bonds and cheaply in non-financial corporate bonds – especially those that are Fed eligible.

Patient investors focused on long term fundamentals rather than short term technicals, are able to capture this mis-pricing with a medium to long term view. For these long-standing spread relationships to mean revert, we need to see an increase in new AUD corporate bond issuance so that price discovery is possible. Primary market activity will lead to more secondary market activity and subsequently (all things being equal), buy and sell spreads will tighten.

Never miss an update

Enjoy this wire? Hit the ‘like’ button to let us know.

Stay up to date with my current content by

following me below and you’ll be notified every time I post a wire

David joined Artesian in 2013 and is the Portfolio Manager of the Artesian Corporate Bond Fund and the Artesian Green & Sustainable Bond Fund. Prior to joining Artesian, David spent 9 years in the United Kingdom working for Deutsche Bank and RBS. David has extensive investment and PM experience.

........

Artesian Corporate Bond Pty Ltd (ACN 618 342 895) has been appointed as the investment manager in respect of the Fund. Artesian Venture Partners Pty Ltd ABN 58 112 089 488 holds an AFS license no.284492 and has appointed the Investment Manager as its authorised representative (number 001260177). Equity Trustees Limited (‘EQT’), ABN 46 004 031 298, AFSL 240975, is the Responsible Entity for the Fund . This information has been prepared to provide you with general information only. Some of the information in this document may be derived from third parties. We do not express any view about the accuracy or completeness of information that is not prepared by us and no liability is accepted for any errors it may contain. It is not intended to take the place of professional advice and you should not take action on specific issues in reliance on this information. Past performance should not be taken as an indicator of future performance. In preparing this information, we did not take into account the investment objectives, financial situation or particular needs of any particular person. You should obtain a copy of the product disclosure statement before making a decision about whether to invest in this product. Copies of the product disclosure statement can be obtained by visiting www.eqt.com.au/insto or request a copy by emailing the Investment Manager at bondoperations@artesianinvest.com, visiting www.artesianinvest.com or calling +61 3 9288 9444. Distribution of this information to anyone other than the original recipient and that party’s advisers is unauthorised. Any reproduction of these materials, in whole or in part, or the divulgence of any of its contents, without the prior consent of Artesian is prohibited. Any securities recommendation or comments (including an opinion) contained in this document is general advice only and does not take into account your personal objectives, financial situation or needs. Artesian and EQT are not acting in a fiduciary capacity. Recommendations or statements of opinion expressed may change without notice. You should not act on a recommendation or statement of opinion without first considering the appropriateness of the general advice to your personal circumstances. Nothing in this document should be construed as Artesian or EQT providing an opinion, statement or research dealing with the creditworthiness of a body or the ability of an issuer of a financial product to meet its obligation under the product.

2 topics

4 stocks mentioned

David Gallagher

Portfolio Manager of the Artesian Corporate Bond Fund and the Artesian Green & Sustainable Bond Fund

Artesian

David joined Artesian in 2013 and is the Portfolio Manager of the Artesian Corporate Bond Fund and the Artesian Green & Sustainable Bond Fund. Prior to joining Artesian, David spent 9 years in the United Kingdom working for Deutsche Bank and RBS....

Expertise

David Gallagher

Portfolio Manager of the Artesian Corporate Bond Fund and the Artesian Green & Sustainable Bond Fund

Artesian

David joined Artesian in 2013 and is the Portfolio Manager of the Artesian Corporate Bond Fund and the Artesian Green & Sustainable Bond Fund. Prior to joining Artesian, David spent 9 years in the United Kingdom working for Deutsche Bank and RBS....

Expertise

Comments

Comments

Sign In or Join Free to comment