Australia in 2019/2020: Recession likely, rates heading to zero

Excess in the Australian housing market has been widely discussed by investors and commentators for a number of years. Underpinned by cheap money, house prices have risen significantly resulting in extreme valuations (house prices are nearly 9x average incomes).

Other signs of a housing bubble have also emerged:

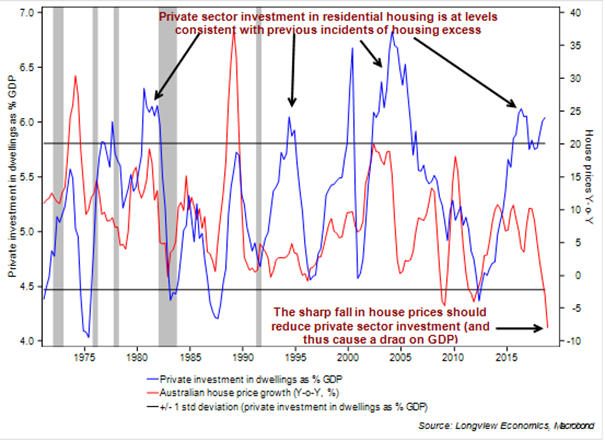

- Investment in housing is extreme (fig 3);

- the percentage of people employed in construction is close to bubble-like levels (i.e. similar to those of Spain and Ireland ahead of the GFC);

- the household debt to GDP ratio is one of the highest in the world (121.3%);

- and mortgage debt has grown almost twice the pace of GDP in the last 10 years.

Fig 3: Private investment in dwellings (as % of GDP) vs. house prices (Y-o-Y, %)

With house prices and housing activity now declining sharply, those excesses have begun to unwind and key leading indicators point to ongoing weakness:

- Building permits, for example, are down 19% Y-o-Y1 (and tend to lead house price growth by ~3 months).

- In addition, transactions are down 32% Y-o-Y,

- While growth in mortgage lending is contracting at the fastest pace in 8 years (both transactions and mortgage lending lead house price growth).

Recession is likely

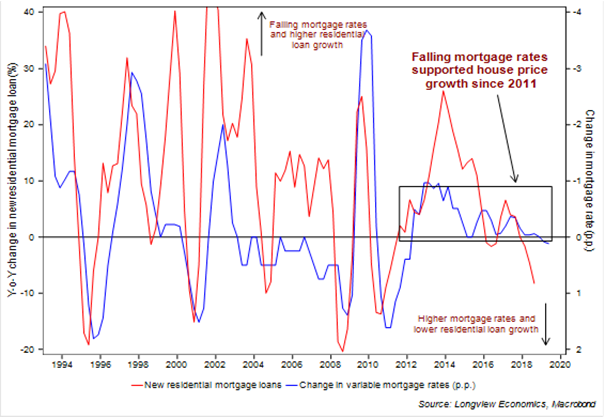

Whilst it is impossible to be certain a bubble has burst/is bursting ex ante, there is strong evidence that this is the case in Australia. Bubbles tend to burst when money becomes expensive. In that respect, rising pressure on commercial bank funding costs will continue to feed through into the housing sector via higher mortgage rates (fig 2) and should result in further house price weakness.

Fig 2: New residential mortgage loans (Y-o-Y, %) vs. change in variable mortgage rates (INVERTED & advanced 6m, p.p.)

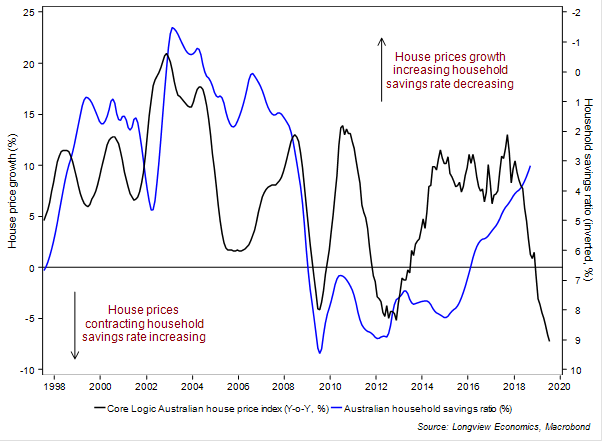

As the wealth effect from rising house prices reverses, households should continue to deleverage and their savings rate should start to pick up (as is typical during housing downturns, fig 1). This will, in turn, result in weak/contracting household consumption growth (i.e. the primary component of GDP), and should result in a recession later this year or early next year.

Fig 1: House price growth (adv. 6m) vs. household savings rate (9m smoothed, inverted)

Rates headed to zero

Whilst a series of RBA rate cuts is therefore likely (beginning in the latter half of this year), that policy response is probably too late, given that policy works with lags and downward momentum in housing is already underway. We expect the RBA to cut rates to zero and potentially use other policies, e.g. QE.

In the event of a systemic banking crisis (not our base case – 20-25% probability), it is also likely that significant government intervention would take place to recapitalise Australian banks.

The full report

You can view a copy of the full report here: (VIEW LINK)

Never miss an update

Enjoy this wire? Hit the ‘like’ button to let us know.

Stay up to date with my current content by

following me below and you’ll be notified every time I post a wire

Longview Economics, founded in 2003 by Chris Watling, is an independent research house based in London, providing three distinct yet interrelated groups of research products: Short and medium term market timing; Long term global asset allocation advice; and Global thematic, macro and commodities research.

3 topics

Longview Economics, founded in 2003 by Chris Watling, is an independent research house based in London, providing three distinct yet interrelated groups of research products: Short and medium term market timing; Long term global asset allocation...

Expertise

Longview Economics, founded in 2003 by Chris Watling, is an independent research house based in London, providing three distinct yet interrelated groups of research products: Short and medium term market timing; Long term global asset allocation...

Expertise

Comments

Comments

Sign In or Join Free to comment