Avita Therapeutics: A bright future, and 50% off to boot

It hasn’t been a good year for Avita Therapeutics (ASX:AVH). The med-tech stock is the worst performer among Livewire readers’ 10 most-tipped small caps, down nearly 50% this year.

But the long-term potential is good and just got better, says Bell Potter senior analyst John Hester. He believes the market is too fixated on the spray-on skin maker's short-term sales hit from COVID-19, pointing out the company - which Hester has covered since 2017 - has pulled forward clinical trials that could boost its market ten-fold.

"We think the reason the stock price has fallen so much is primarily because of COVID – the fundamentals of the company are 100% in place. The company is trading at around $7 now, so there is a lot of upside. We think it will recover a lot of value, particularly as we get more data emerging from clinical trials."

In the following wire, Hester defines exactly what Avita does, picks the highlights of its FY 20 results and discusses Bell Potter’s latest share price target.

Can you give new investors a crash course on Avita Therapeutics?

Avita’s technology came to prominence initially in 2001 during the Bali Bombings. The technology was developed by Dr Fiona Woods who now works at the Royal Perth Hospital. She developed this technology which we know today as ‘spray-on-skin’ and it was used to treat victims of the bombings.

The standard of care for the treatment of large burns is skin grafting. This involves the grafting of skin from an unaffected area of the body and surgically attaching the graft to the burn. The issue with this is that the process of grafting can be more painful than the actual burn itself and it creates severe scaring, both at the site of the wound and the donor site. Further, the skin colour and texture can appear vastly different when reapplied to another area of the body. For these reasons, patient outcomes are generally poor hence the need for a better solution.

Dr Woods developed the spray-on-skin technology and the surgical procedure (known as RECELL) as an alternative to grafting or to be used in conjunction with grafting. In a nutshell:

- The surgeon takes a much smaller graft of the patient’s skin which is soaked in a proprietary solution;

- After a short period, the sample is disaggregated into its individual cellular components (being melanocytes, keratinocytes, fibroblasts and others) while fatty tissue and hair follicles are removed. The remaining cells are mixed into a cell solution that is sprayed across the entire wound bed;

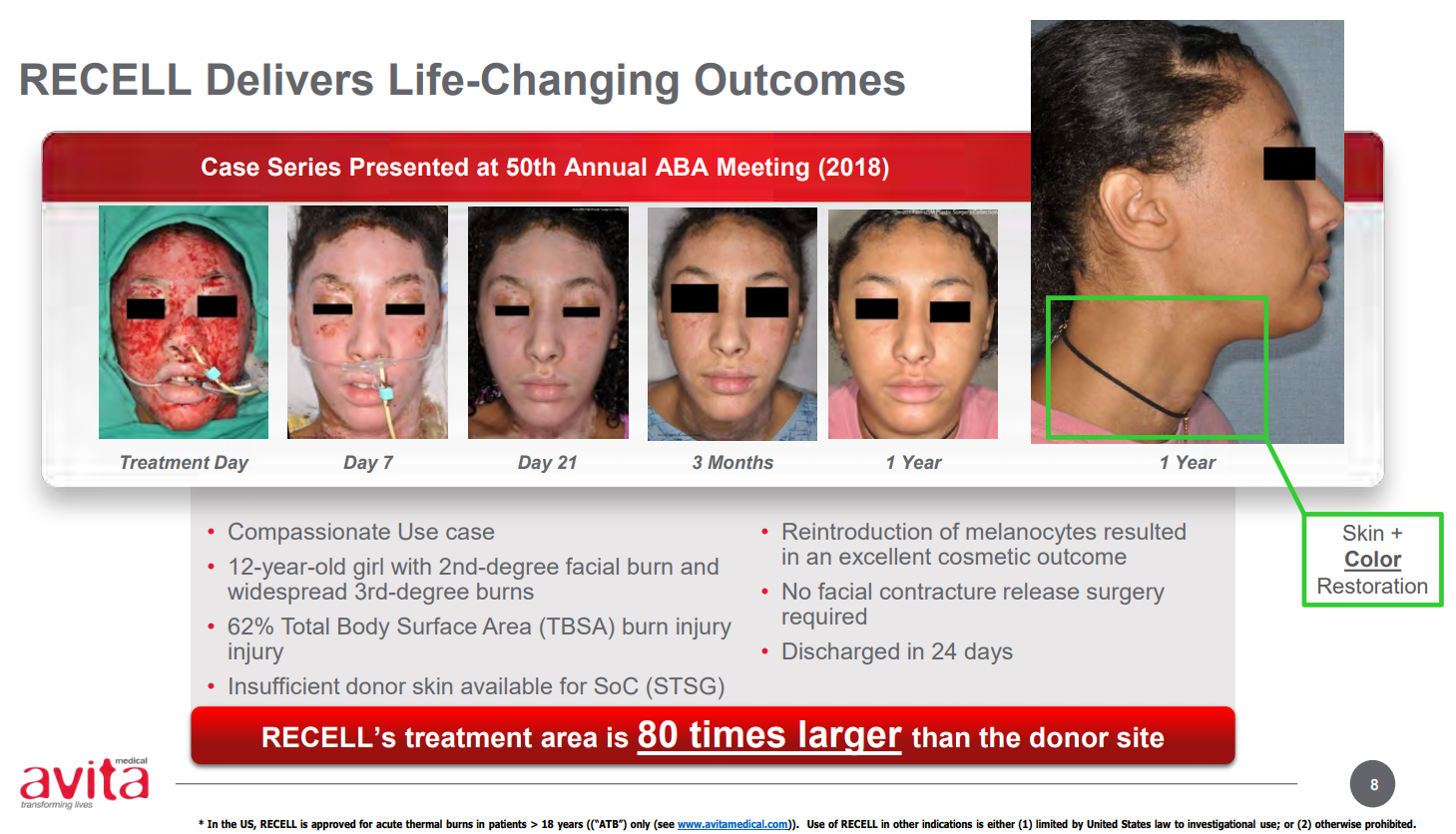

- The big advantage is the donor site sparing - a credit card size graft can be used over a person’s whole back, as an example. On average the treatment area is 80-times the donor area;

- Because the patient’s own skin is the source of the graft - known as an autologous graft - there is no chance of graft rejection. New tissue proliferates across the entire surface area of the wound bed resulting in stunning wound healing results for many patients.

- RECELL was approved in the United States in September 2018, following an extensive clinical trial program in the treatment of burns requiring admission to hospital.

It is important to note that the technology will only work where there is some dermis left. The example Avita often shows in its presentations is the case of a 12-year-old African American girl who suffered severe burns all over her face and neck (see below). If she had undergone grafting the scarring would have been horrendous. If you look at the latest pictures, there is no scarring and her pigmentation has returned, so it looks very natural.

Click to enlarge

The financials of this product are incredible – the gross margin is better than 90% and the total addressable market (TAM) in burns is estimated at US$200 million. The company is conducting clinical trials in adjacent indications which it believes may expand its use into markets with TAM of up to US$2 billion.

How long have you covered the stock and what attracted you to it?

We have been covering the stock since 2017 when we were introduced to the CEO Dr Mike Perry. We thought his background and career history at Novartis and in private equity at Bay City Capital amongst other achievements was very impressive.

RECELL is completely innovative – there is nothing like it in the market. We could see from an ethical standpoint it is a great product and has potentially vastly superior outcomes for patients in numerous categories. It’s also fair to say that prior to the involvement of Dr Perry and the current Board, the company lacked proper corporate diligence and this was one of the reasons why it had not achieved commercial success.

RECELL was first approved in Europe and Australia in approximately 2005, but a lack of data from randomised clinical trials had been a key barrier to widespread adoption. Commercialising any new medical technology requires good data from clinical trials and supporting health economics. Once these issues had been addressed, the likelihood of success was vastly improved, hence our decision to back the company.

RECELL received a Pre Market Approval in September 2018 and the product was launched in the US the following January. With extensive intellectual property protection from patents and other instruments, it should be many years before a superior competing technology emerges.

What were the key points of the recent result?

Avita was starting to build on the success of commercialising RECELL and had ongoing growth in quarterly revenues. Then COVID hit in late February/March. Revenues were building in the first three quarters of the year and the product was getting broad adoption among surgeons, but then because of COVID, they were guiding anywhere between flat to a 20% reduction in volumes. It turned out that the June quarter was flat with March, which is what we expected.

But what investors should really know is that the company raised US$120 million in capital last year and they’re really starting to expedite clinical trials into adjacent indications. The adjacent indications are:

- Paediatric burns – the current label does not include children. There are two clinical trials underway in the US for the treatment of paediatric scalds.

- Trauma wounds - including various injuries such as roadrash, surgical scars, gunshot wounds, skin cancers and other abrasions.

- Vitiligo – an immune system disease resulting in severe skin discolouration where the melanocytes (the cells which give the skin its pigment) are dysfunctional. Management expects to recruit the first vitiligo patient to a clinical trial in September 2020.

- Outpatients - RECELL is currently limited to the treatment of inpatients. The company is investigating reimbursement for the use of Recell in the treatment of outpatients burns.

How did the results compare with your expectations? And those of the broader market?

The market liked the result and sent AVH up nearly 11% last Friday. The only thing that surprised me was the large non-cash charge for share-based remuneration which is dilutive. But that is going to be an ongoing thing to expect as they are effectively an American company now since their primary listing was redomiciled into the NASDAQ.

What is your rating and price target on the stock?

We’re maintaining a buy with a price target of $15, down from $16 due to the share-based remuneration factor which I mentioned.

The company is trading at around $7 now, so there is a lot of upside. We think it will recover a lot of value, particularly as we get more data emerging from clinical trials.

We think the reason the stock price has fallen so much is primarily because of COVID – the fundamentals of the company are 100% in place. AVH is well capitalised with around US$74 million in the kitty and annualised revenue of US$20 million. While they are spending a lot of cash on their clinical trials, we think that will be an important driver of further growth if those three indications I mentioned are successful: trauma wounds, vitiligo and RECELL on outpatients.

All that costs money, but if they get it, their TAM increases by a multiplier of 10 – pretty important stuff.

Want more earnings season Q&As like this?

Hit like so we know that you want more of this type of content.

Throughout August, my colleagues Patrick Poke, Bella Kidman, Glenn Freeman and James Marlay will also publish similar Q&As on Livewire readers' most-tipped big caps and small caps. Hit FOLLOW on our profiles to be notified when these wires are published.

Never miss an update

Enjoy this wire? Hit the ‘like’ button to let us know.

Stay up to date with my current content by

following me below and you’ll be notified every time I post a wire

I have over 15 years’ experience covering financial markets and property, with a particular interest in ETFs and personal finance. I split my time between Australia and Canada to bring a global perspective to my work.

........

Livewire gives readers access to information and educational content provided by financial services professionals and companies ("Livewire Contributors"). Livewire does not operate under an Australian financial services licence and relies on the exemption available under section 911A(2)(eb) of the Corporations Act 2001 (Cth) in respect of any advice given. Any advice on this site is general in nature and does not take into consideration your objectives, financial situation or needs. Before making a decision please consider these and any relevant Product Disclosure Statement. Livewire has commercial relationships with some Livewire Contributors.

4 topics

1 stock mentioned

3 contributors mentioned

I have over 15 years’ experience covering financial markets and property, with a particular interest in ETFs and personal finance. I split my time between Australia and Canada to bring a global perspective to my work.

Expertise

I have over 15 years’ experience covering financial markets and property, with a particular interest in ETFs and personal finance. I split my time between Australia and Canada to bring a global perspective to my work.

Expertise

Comments

Comments

Sign In or Join Free to comment