Big news: Melbourne house prices are rising again...

In the AFR today I write that I am delighted to deliver big news: despite Melbourne's horrifically long lockdown, home values are increasing again alongside the price of bricks and mortar in every other city across the country. This is being helped by the fact that debt serviceability is the best it's been in about 19 years. Excerpt enclosed:

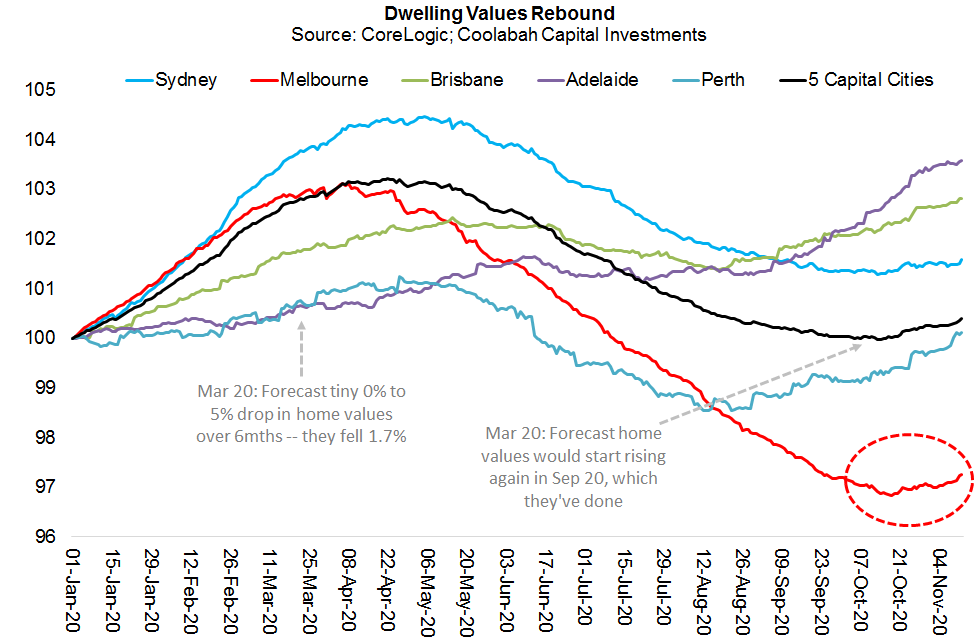

Based on CoreLogic’s daily hedonic index, the Melbourne residential property market bottomed on October 18. Since then, dwelling values in the southern city have appreciated by a solid 0.44 per cent.

In the first 12 days of November, they climbed 0.22 per cent, outperforming Sydney, Brisbane and Adelaide, although lagging stronger growth in Perth (0.40 per cent).

This reconciles with impressive auction clearance rates on what have been healthy volumes: CoreLogic estimates the clearance rate in Melbourne last weekend was 68 per cent on a total of 607 auctions.

Across the five largest cities, the low watermark for national home values looks to have been October 13, almost exactly six months after prices started declining.

This accords with our March 2020 projection for a mild 0 per cent to 5 per cent six-month correction, following which we argued prices would start appreciating again.

The official record is that across all metro- and non-metro regions, house prices declined just 1.7 per cent during the COVID-19 shock. Within the eight capital cities, the peak-to-trough loss was a similarly modest 2.8 per cent.

Needless to say, the resilient Australian housing market has once again called into question analysts’ (and investors') forecasting abilities, comprehensively burying the many hyperbolic bears who during this incredibly mild downturn have whipped themselves up into an apocalyptic lather.

The nascent recovery has been gradual, with no hint whatsoever of a bubble brewing, although we project that it will pick up at a nontrivial pace in 2021 with total capital gains in the next phase of the cycle of at least 10 per cent to 20 per cent.

The good news for regulators is that house prices have not registered a net increase in four years. Debt serviceability is also the best it has been in a long time.

According to the Reserve Bank, interest repayments on residential mortgages as a share of total household incomes are just 5.3 per cent, which is the lowest they’ve been since March 2002.

In New Zealand, the central bank has indicated it may roll out macro-prudential constraints once again on higher-risk lending if the housing market gets ahead of itself.

The Australian Prudential Regulatory Authority and the RBA will do the same here if there is any sign of a bubble brewing. And they now know with high conviction that these macroprudential controls work: APRA’s efforts to dampen exuberance in Australian housing ultimately triggered a 10 per cent correction in prices between 2017 and 2019.

There are reports that non-bank lenders want to access the same funding costs as Australia’s highly regulated and overcapitalised banks.

Supposedly the non-banks would like the Treasury to offer them the same, ultra-low 0.1 per cent cost of capital banks can capitalise on via the RBA’s $200 billion Term Funding Facility.

This is a silly suggestion. If a non-bank wants to be treated by the government on the same terms as a bank, it should become one. The non-banks have every opportunity to apply for a banking licence with APRA. But they typically do not because of the huge regulatory and capital burden that a coveted banking licence carries.

There is a reason why we have historically avoided the illiquid bonds issued by non-banks, including their residential mortgage-backed securities (RMBS): relative to what we see inside the banks, it is hard to get comfortable with the credit risk assessment processes of these lightly-regulated entities that originate loans to then sell (or securitise) them.

If you hold a loan on your balance sheet, as banks do, until its maturity – rather than offloading it to investors – you tend to be far more focused on the long-term risk of that loan going into default. That was certainly the lesson bequeathed by the GFC vis-a-vis the originate-to-securitise model.

Not already a Livewire member?

Sign up today to get free access to investment ideas and strategies from Australia’s leading investors.

Never miss an update

Enjoy this wire? Hit the ‘like’ button to let us know.

Stay up to date with my current content by

following me below and you’ll be notified every time I post a wire

Chris co-founded Coolabah in 2011, which today runs over $8 billion with a team of 40 executives focussed on generating credit alpha from mispricings across fixed-income markets. In 2019, Chris was selected as one of FE fundinfo’s Top 10 “Alpha Managers” based on his risk-adjusted performance throughout his career across. He previously worked for Goldman Sachs in London and Sydney, the Reserve Bank of Australia, and founded the award‐winning research/investment group, Rismark. He has regularly advised governments, developing unique policy proposals. Chris graduated with the University Medal (Economics & Finance) from Sydney University. He studied in the PhD program at Cambridge University in 2002/03, leaving to set up his funds business.

........

Investment Disclaimer

Past performance does not assure future returns. All investments carry risks, including that the value of investments may vary, future returns may differ from past returns, and that your capital is not guaranteed. This information has been prepared by Coolabah Capital Investments Pty Ltd (ACN 153 327 872). It is general information only and is not intended to provide you with financial advice. You should not rely on any information herein in making any investment decisions. To the extent permitted by law, no liability is accepted for any loss or damage as a result of any reliance on this information. The Product Disclosure Statement (PDS) for the funds should be considered before deciding whether to acquire or hold units in it. A PDS for these products can be obtained by visiting www.coolabahcapital.com. Neither Coolabah Capital Investments Pty Ltd, EQT Responsible Entity Services Ltd (ACN 101 103 011), Equity Trustees Ltd (ACN 004 031 298) nor their respective shareholders, directors and associated businesses assume any liability to investors in connection with any investment in the funds, or guarantees the performance of any obligations to investors, the performance of the funds or any particular rate of return. The repayment of capital is not guaranteed. Investments in the funds are not deposits or liabilities of any of the above-mentioned parties, nor of any Authorised Deposit-taking Institution. The funds are subject to investment risks, which could include delays in repayment and/or loss of income and capital invested. Past performance is not an indicator of nor assures any future returns or risks. Coolabah Capital Institutional Investments Pty Ltd holds Australian Financial Services Licence No. 482238 and is an authorised representative #001277030 of EQT Responsible Entity Services Ltd that holds Australian Financial Services Licence No. 223271. Equity Trustees Ltd that holds Australian Financial Services Licence No. 240975.

Forward-Looking Disclaimer

This presentation contains some forward-looking information. These statements are not guarantees of future performance and undue reliance should not be placed on them. Such forward-looking statements necessarily involve known and unknown risks and uncertainties, which may cause actual performance and financial results in future periods to differ materially from any projections of future performance or result expressed or implied by such forward-looking statements. Although forward-looking statements contained in this presentation are based upon what Coolabah Capital Investments Pty Ltd believes are reasonable assumptions, there can be no assurance that forward-looking statements will prove to be accurate, as actual results and future events could differ materially from those anticipated in such statements. Coolabah Capital Investments Pty Ltd undertakes no obligation to update forward-looking statements if circumstances or management’s estimates or opinions should change except as required by applicable securities laws. The reader is cautioned not to place undue reliance on forward-looking statements.

3 topics

Chris co-founded Coolabah in 2011, which today runs over $8 billion with a team of 40 executives focussed on generating credit alpha from mispricings across fixed-income markets. In 2019, Chris was selected as one of FE fundinfo’s Top 10 “Alpha...

Expertise

Chris co-founded Coolabah in 2011, which today runs over $8 billion with a team of 40 executives focussed on generating credit alpha from mispricings across fixed-income markets. In 2019, Chris was selected as one of FE fundinfo’s Top 10 “Alpha...

Expertise

Comments

Comments

Sign In or Join Free to comment