Buying time to sell − fixed income spreads come under fire

Fixed income is marketed to investors as a defensive asset class, as a general rule offering principal and income security combined with liquidity. That is the major trade-off for lower expected returns. The exposure helps to dampen portfolio volatility over time and should provide investors protection against cyclical economic and market downturns. From a “defend and protect’’ asset class such as fixed income, it also provides the liquidity that enables investors the flexibility to move quickly into risk assets when those valuations are appealing, such as the recent large decline in the ASX.

Sadly, for many investors, some fixed income managers have dropped the ball right in their time of need. By loading up on low quality or illiquid securities in the lead up to the current crisis, many fixed income investment managers have failed to defend investor portfolios. As a consequence, they have now added significant sell side spreads to their retail products, resulting in vastly weaker liquidity conditions and adding substantial additional costs to exit − right in their investors’ time of need. If investors can’t access perceived lower risk and liquid fixed income holdings in times of market stress, then what purpose does it actually serve?

Are investors getting their intended risk exposures?

For fixed income managers to say “we never saw this coming’’, is something we find baffling. This Coronavirus story has been steadily developing through February and into March, it was not a secret. Extreme market events and sell-offs are a constant threat and are sometimes difficult to foresee, such as the terrorism attack of September 11th. But this is crisis number 5 for our team with September 11th, the GFC, the Eurozone crisis, the Greek crisis and now Coronavirus (health and credit crisis) having all occurred throughout the portfolio management careers of our team.

This was most certainly not a plane hitting a building moment! Pre-crisis, economic growth was slowing, the US Treasury yield curve had inverted from May to October 2019 and corporate credit was showing signs of liquidity stress, signalling danger and the potential for recession. There was ample time for experienced fixed income managers to improve the liquidity profile of their portfolios and sell some of the low quality and illiquid assets that they had purchased in order to chase extra yield. Unfortunately, with other managers having not done so at the right time, this has left investors to pick up the pieces − as the performance of what should be the most defensive part of their portfolio suffers.

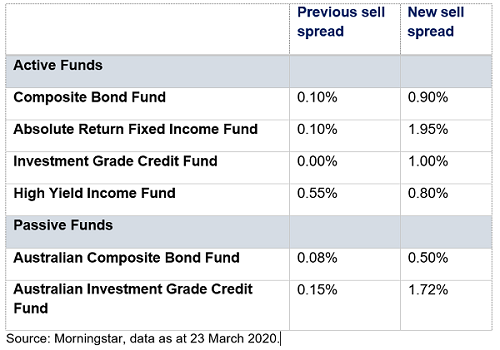

Table: Sell spread changes

An example of various fixed income funds (based on retail investment products)

In our opinion, the sell side spread widening is an alarming development and warrants some serious discussion. Investors should be looking underneath the bonnet and asking their fixed income managers just how much low quality credit their funds hold, have they strayed from the mandate, are they really ‘true to label’? One of the very reasons investors allocate to bonds is for portfolio stability. This allocation should be robust when investors need it the most.

Extreme market volatility offers investors a reminder: “quality counts”

Many recent articles on sell spreads have not mentioned any of the fixed income investment managers who had not changed their buy/sell spreads at all during this time and are functioning as promised − having not changed the goal posts mid game when their investors needed them most.

At JCB we have long advocated the role of fixed income in asset allocation as a way to protect and diversify portfolios. That said, it is important to understand that not all fixed income securities are created equal. Investors need to be wary of just how liquid and defensive their fixed income exposures are as it can have a substantial impact on performance, especially in times of market stress. JCB remains well positioned to service investor redemption requests and has done so over the month, despite the higher volatility environment, without penalising our investors with punitive sell spreads.

In times like these, asset quality and liquidity matters more than ever. High grade sovereign bonds have historically defended and protected when needed – we have seen that play out in previous sustained bear markets and we believe they will continue to be a genuine store of wealth in highly uncertain times. We firmly believe that the industry must address these “fit for purpose’’ questions around what is truly defensive in what has become the second major sequencing event in 12 years.

You can reduce risk without giving up too much return

During periods of market turbulence, global high-grade sovereign bonds can help offset riskier assets, helping to get the balance right between risk and return. Find out more here

Never miss an update

Enjoy this wire? Hit the ‘like’ button to let us know.

Stay up to date with my current content by

following me below and you’ll be notified every time I post a wire

Charles is a co-founder of Jamieson Coote Bonds (JCB) and oversees portfolio management of the Australian and Global High Grade Bond and Dynamic Alpha investment strategies. Prior to JCB, Charles forged a career as a seasoned bond investor from 2001 in New York, Tokyo, London and Sydney, with Merrill Lynch/Bank of America Merrill Lynch. Over his career, Charles has managed large Government Bond portfolios in key major currencies and derivative instruments. During this time, he has managed through the spectrum of financial market dynamics, including September 11, 2001, the Global Financial Crisis, Eurozone crises, the US credit rating downgrade and Chinese/Greek concerns.

........

This information is provided by JamiesonCooteBonds Pty Ltd ACN 165 890 282 AFSL 459018 (‘JCB’). Past performance is not a reliable indicator of future performance. This information should not be considered advice or a recommendation to investors or potential investors in relation to holding, purchasing or selling units and does not take into account your particular investment objectives, financial situation or needs. Before acting on any information you should consider the appropriateness of the information having regard to these matters, any relevant offer document and in particular, you should seek independent financial advice.

4 topics

Charles is a co-founder of Jamieson Coote Bonds (JCB) and oversees portfolio management of the Australian and Global High Grade Bond and Dynamic Alpha investment strategies. Prior to JCB, Charles forged a career as a seasoned bond investor from...

Charles is a co-founder of Jamieson Coote Bonds (JCB) and oversees portfolio management of the Australian and Global High Grade Bond and Dynamic Alpha investment strategies. Prior to JCB, Charles forged a career as a seasoned bond investor from...

Comments

Comments

Sign In or Join Free to comment