CBA’s dividend can’t stop a new high (WTC, WES, VOC, CWN)

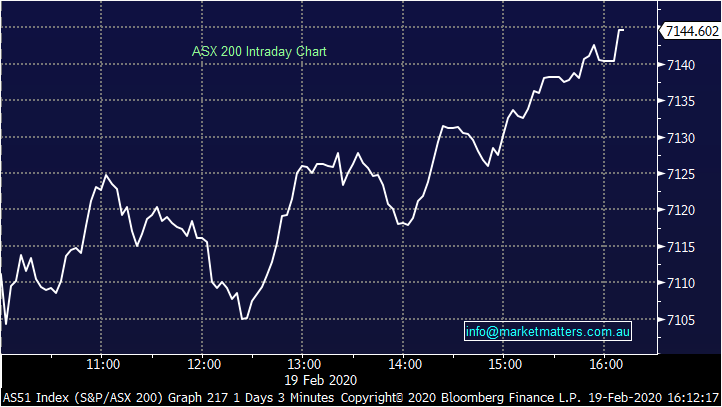

A reasonable day for the index today despite the heavyweight CBA going ex-div for $2. The biggest bank took 14pts off today but was little resistance to the broader market which set a (marginal) new all-time high for the close. Strength came from healthcare in particular, where CSL and COH both hit all-time highs. Consumer discretionary names were dragged higher by great results out of Wesfarmers and Dominoes. Tech slumped despite the broad rally as Wisetech tumbled more than 25%.

Reporting schedule available here: CLICK HERE

Overall, the ASX 200 rose 30pts / +0.43% today to close at 7144. Dow Futures are trading up +87pts/+0.30%

ASX 200 Chart

ASX 200 Chart

CATCHING MY EYE

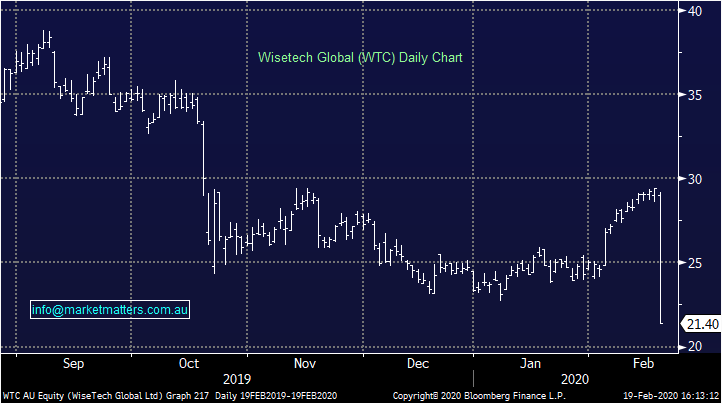

Wisetech (WTC) -27.31%: today’s biggest loser was logistics tech company Wisetech which missed at their half year results and came in below consensus for full year guidance as corona impacts global supply chains. At the half year, revenue came in at $205.9m dropping down to NPATA of $33.5m. EBITDA margins tightened by 1bp as costs ran ahead of revenue with a number of new rollouts happening in the half. Their main product, CargoWise, delivered organic growth of 24% as customers increase their use, new features are integrated, and new customers come online. The big concern for the market though was the downgrade to guidance. Revenue guidance for the full year was dropped to $420-450m from $440-460m, while EBITDA is now expected in the range of $114-132m down from $145-153m. consensus was sitting above guidance for revenue and near the top end for EBITDA, so it was a 6.5% & 18.9% miss to the street respectively.

Wisetech (WTC) Chart

Wesfarmers (WES) +2.87%: first half result for Wesfarmers reasonably close to market’s expectations, however the stock was bid up one some signs the slowdown in Bunning’s sales growth may be behind it. Revenue and earnings were both up around 6% on a comparable basis. Bunnings, which now accounts for around half of the earnings, saw EBIT rise around 3% while same store sales grew 4.7% for the half. This compares to +4.0% in 1H19 and +3.8% in 2H19 with the company attributed the good result to improvements both in store and online. Kmart Group, which includes Target, saw revenue up 7.6% which was all driven by a standout half from Kmart, while Target slipped with the company not expecting a rebound any time soon. The last retail brand is Officeworks which added 4% to EBIT in the half to beat expectations.

Wesfarmers smaller chemicals, energy & fertilizers and industrials & safety units continue to track higher. They continue to splash cash here to diversify their earnings, acquiring lithium name Kidman Resources in the half. Interestingly, alongside the announcement Wesfarmers sold part of their stake in Coles (COL) a day after their result. The 4.9% stake represents around a third of the holding and was sold at $16.08 – Coles closed the day down 4.24%, a small discount to the deal.

Wesfarmers (WES) Chart

Vocus Communication (VOC) +8.36%: A good day for the telco after delivering their 1H20 results this morning which carried the headline ‘Clear progress on Vocus Turnaround’. They reported EBITDA growth of 11% on the back of 6% revenue growth. In terms of guidance, they flagged underlying EBITDA for the group in the range of $359-$379m, which implies a small ~2% upgrade to current market expectations of $363m, while progress on debt reduction was also a positive. The underlying tone of this morning’s update implies the business is turning after a tough period, a good outcome today for VOC.

Vocus (VOC) Chart

Crown (CWN) -0.34%: A weaker than expected 1H20 result for Crown today with mixed operating conditions across their properties. They saw overall growth in Perth gaming, Melbourne was flat on the period, while VIP took a big hit down by 34% relative to the prior year, however the fewer VIP gamblers that were playing had worse luck (Crowns benefit) therefore underpinning an actual rise in VIP revenue. All in all, not a great half for CWN although a lot of bad news currently in the price.

Crown (CWN) Chart

Elsewhere in reporting:

Lovisa (LOV) +2.91%: jewellery retailer’s global push helped lift first half profits ahead of expectations, opening 35 stores adding 22% to global revenue. Warnings around a corona virus impact didn’t stop the market enjoying the result.

Fortescue Metals (FMG) +0.72%: Good / inline result, dividend 76cps was big, market was at 61cps however our analyst bullish at 90cps. At 76cps, that’s 6.79% FF yield for the half. Rallied early but pullback hard showing how bullish the market was here.

Corporate Travel (CTD) +0.12%: Downgraded due to coronavirus however they were tracking towards the lower end of previous forecasts all the same. They now expect FY20 underlying EBITDA of $125-150m, the market was previously at $167m. That’s a 17% downgrade but the stock managed to close marginally higher on the day. Baffling.

Domino's (DMP) +9.64%: Great result, same store sales growth of +4.1% for the half was strong while they also say for the start of the 2H they are printed SSS growth of 6.3%, that’s the key for DMP

Cleanaway (CWY) +16.67%: Strong beat at the profit line, mkt looking for 1H NPAT of ~$65m and they printed $76.2m, the integration of Tox Free was a concern in the mkt however they say that is on track. FY20 EBITDA guidance of ~$515-525m, market was sitting at $505m, a 3% upgrade. We hold Bingo (BIN) in the Platinum Portfolio, they report tomorrow.

Stockland (SGP) +1.63%: Resides in the income portfolio, and delivered a decent result plus reconfirmed guidance for full year of funds from operations (FFO) growth of ~1%. NTA increased 2% to $4.12, dividend inline at 13.5cps for the half based on 84% payout ratio.

Pact group (PGH) +1.63%: No capital raise = positive, earnings okay, gearing heading in the right direction. The market has low expectations, stock should trade higher from here.

Tabcorp (TAH) -5.69%: Soft, NPAT at $213.5m v $221m exp, half year dividend 11cps fully franked, below the 12cps expected

EML Payments (EML) -13.51%: 1H EBTIDA up 42% to nearly $20m, with guidance at $39.5m-$42.5m for the full year, represents an 11% miss to market

Stay on top of Reporting Season with live updates

Market Matters publishes daily market reports and sends SMS alerts when we transact on our portfolio. To get our latest market views and hear when we take new positions, trial Market Matters for 14 days at no cost by clicking the 'CONTACT' button bellow.

Never miss an update

Enjoy this wire? Hit the ‘like’ button to let us know.

Stay up to date with my current content by

following me below and you’ll be notified every time I post a wire

James is Director & Lead Portfolio Manager at Market Partners - a collective of highly experienced investment professionals, operating independently, managing discretionary portfolios for wholesale investors.

James is also Portfolio Manager & primary author at Market Matters, a digital advice & investment platform with over 2500 members that offers real market intel & six portfolios open for investment.

........

Any advice provided is of a general nature only

1 topic

4 stocks mentioned

James is Director & Lead Portfolio Manager at Market Partners - a collective of highly experienced investment professionals, operating independently, managing discretionary portfolios for wholesale investors. James is also Portfolio Manager &...

Expertise

James is Director & Lead Portfolio Manager at Market Partners - a collective of highly experienced investment professionals, operating independently, managing discretionary portfolios for wholesale investors. James is also Portfolio Manager &...

Expertise

Comments

Comments

Sign In or Join Free to comment

most popular

Investment Theme

If 24 LICs ran the Melbourne Cup, which ones would we back?

Affluence Funds Management