Central banks rising as one? Not quite...

Alex Joiner

IFM Investors

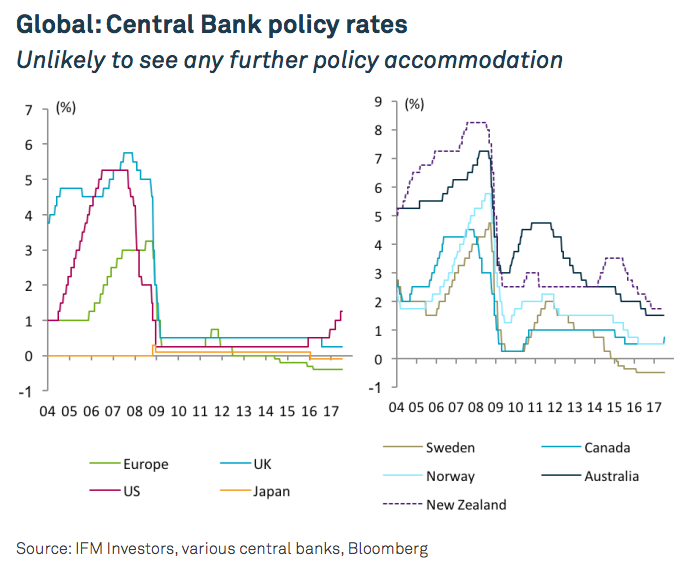

The Fed is clearly well out in front in reducing monetary policy stimulus. Its stance was demonstrated again in June as the FOMC (Federal Open Market Committee) increased the Federal Funds Rate by 25bp. As a result, the target rate rose to 1.00- 1.25%, while the Committee noted that the “labor market has continued to strengthen and that economic activity has been rising moderately so far this year”. Economists remain of the view that there will be one more rate hike this year, based on the data flow, particularly growth and solid labour market performance. The improved growth will come despite what are now increasing concerns, from economists and the Fed alike, that the softer pace of inflation may persist.

Across the border the Bank of Canada (BoC) raised interest rates for the first time in seven years (September 2010) this month. The hike was in line with market expectations and saw the policy rate rise 25bp to 0.75%, in what was described as a “removal of stimulus”. The move was driven by the BoC’s confidence in its outlook for “above potential growth” for at least the remainder of 2017 and into 2018. Although equally it recognised the softness of inflation recently as it remains in the bottom of the target range. Yet this has been attributed to temporary factors and Governor Stephen Poloz noted that it takes 18 to 24 months for a monetary policy action to have its full effect on inflation. Poloz added that central banks must “target future inflation by anticipating future deviations from target”.

Central bankers in Australia and New Zealand will be keenly examining the impact of Canada’s hike. Not only on its booming property market, but, as the BoC statement notes, the economy may be “more sensitive to higher interest rates than in the past, given the accumulation of household debt. We will need to gauge carefully the effects of higher interest rates on the economy.” Exactly the same can be said for household sectors in Australia and New Zealand.

Across the Atlantic, the BoE is seemingly in two minds about whether or not to raise policy rates. The Monetary Policy Committee (MPC) was divided at its June meeting, voting by a majority of 5-3 to maintain its policy rate at 0.25%. The three members of the MPC in favour of raising rates included, as it transpired, the BoE’s Chief Economist – putting him somewhat at odds with a more measured view from Governor Mark Carney. Andrew Haladine’s and others more hawkish tone came as inflation becomes an increasing concern, with the MPC’s minutes noting it could rise above 3% by the autumn, “and is likely to remain above the target for an extended period” as sterling’s depreciation continues.

On the continent, the ECB became somewhat more optimistic, both during its press conference after its recent monetary policy decision and at an ECB Central Bank conference in Sintra, Portugal. ECB President Mario Draghi was broadly upbeat, if not hawkish, when suggesting that the threat of deflation are gone and “reflationary forces” are at play as the region’s economic recovery continues. He did try to subsequently soften his remarks, but it nonetheless remains clear that further interest rates cuts are now unlikely. Draghi refused to be drawn on the issue of tapering asset purchases, noting the ECB will be in the market “for a long time”. Indeed, he noted purchases could be increased should the economy soften. As it stands, there is an expectation that the ECB will communicate a tapering of this program towards the end of the year

The Bank of Japan is the laggard of the major central banks, displaying no current desire to relax its policy of accommodation. Governor Haruhiko Kuroda refused to be drawn recently on any specific discussion of an exit strategy, and its policy stance will therefore remain unchanged. Negative interest rates and its ongoing commitment to keep the 10-year bond rate at 0% will remain for the foreseeable future (despite some speculation that this target may rise in line with global yields). This is as GDP growth is around potential, but the inflation pulse is unambiguously weak. As such policy will likely continue to be set “with a view to maintaining the momentum toward achieving the price stability target”.

"if the RBA’s forecast were to come to pass then eight 0.25 percentage point tightenings over the course of 2018 and 2019 were “distinctly possible"

The RBA also remains on hold with a cautiously neutral stance. This has been maintained up until its July meeting, at least, despite some speculation that it may start to share the slightly more hawkish sentiment of global central banks. Speculation was fuelled by comments made by long-serving former Board member John Edwards (his term ended July 2016) who suggested with regard to interest rate increases that “the time is coming to get back to normal”, and adding: “It’s possible the tightening could start earlier.” He went further still to suggest that if the RBA’s forecast were to come to pass then eight 0.25 percentage point tightenings over the course of 2018 and 2019 were “distinctly possible”…

For the full IFM Investors June Economic update, please click here.

Never miss an update

Enjoy this wire? Hit the ‘like’ button to let us know.

Stay up to date with my current content by

following me below and you’ll be notified every time I post a wire

Alex is IFM Investors’ Chief Economist and has well over a decade of experience in the field. He is responsible for the firm’s economic, financial market and policy analysis and forecasting and is also a member of IFM’s Investment Committee. @IFM_Economist

3 topics

Alex Joiner

Chief Economist

IFM Investors

Alex is IFM Investors’ Chief Economist and has well over a decade of experience in the field. He is responsible for the firm’s economic, financial market and policy analysis and forecasting and is also a member of IFM’s Investment Committee....

Expertise

Alex Joiner

Chief Economist

IFM Investors

Alex is IFM Investors’ Chief Economist and has well over a decade of experience in the field. He is responsible for the firm’s economic, financial market and policy analysis and forecasting and is also a member of IFM’s Investment Committee....

Expertise

Comments

Comments

Sign In or Join Free to comment