Competitive advantages of Australia's tech titans

Networks are one of the most powerful competitive advantages a business can possess. Strong network effects make it difficult for businesses to be replicated, enabling long-term pricing power. Businesses without networks often have a harder time defending against competitive forces which in some instances leads to return erosion through price-led competition. Here, we outline a framework for assessing network strength and how various network advantages in ECP’s portfolio of companies measure up, as well as some that could emerge through time.

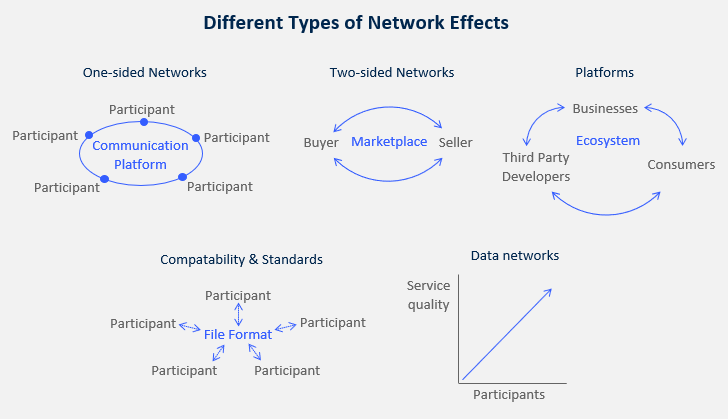

A network effect occurs when a product or service becomes more valuable as participants join the network. The classic example is the telephone, a service which saw its utility increase exponentially with the number of users.

Networks come in many forms. There are one-sided networks such as communication platforms (WhatsApp), two-sided networks which are commonly marketplaces (Realestate.com.au), and platforms such as social mediums (Facebook) which experience both one-sided networks (consumer-to-consumer relationships) and two-sided networks (consumers and developers).

Further, there are compatibility and standards in the IP world (Microsoft Office or Adobe PDF file types), and data networks whereby more users drive increases in data and improved content curation for all users (Google Search or Waze GPS).

Network effects are desirable as they can result in expanding economic returns as latent pricing power is unlocked, and new ecosystem layers are built — deepening a company’s competitive advantage and creating new revenue opportunities.

However, not all networks lead to sustainable competitive advantages. Networks that create sustainable returns require captive participants and a structure which benefits from increasing scale, making replicating either side of the network a taxing objective.

Network Strength

The strength of a network’s competitive advantage can be measured by analysing (1) the degree of participant captivity, and (2) the scale benefits of a network.

Participant captivity measures how ‘sticky’ the user is to the network. Several traits of users can be analysed to determine captivity: Multi-housing is the tendency of users to sit across multiple networks, indicating the network is readily substitutable, whereas Bypass risk is the ability and incentive of users matched in a network to maintain an on-going relationship outside that network.

When we consider food delivery applications such as UberEats and Deliveroo, both restaurants and consumers will happily sit across multiple applications. Unless a company dominates a market early on, competing new entrants can exploit multi-housing tendencies and obtain a foothold.

Where multi-housing exists, building a dominant captive audience is possible but often requires significant brand leadership early on. Australian real estate online classifieds is a case in point whereby both agents and buyers exhibit multi-housing tendencies, yet despite this, Realestate.com.au has a significantly larger franchise than Domain.

Bypass risk is a problem experienced by labour and freelancing marketplaces which often fail to monetise the on-going business relationship it originates as participants frequently bypass the network to avoid marketplace fees.

Scale benefits of a network determine how difficult it is for competitors to penetrate its structure. An extensive network (e.g., global or national) where each node is essential to all network participants has a more durable competitive advantage than an accumulation of localised networks (e.g., cities) that are valuable at the micro-level. The accumulation at the macro level provides limited incremental benefits to network participants.

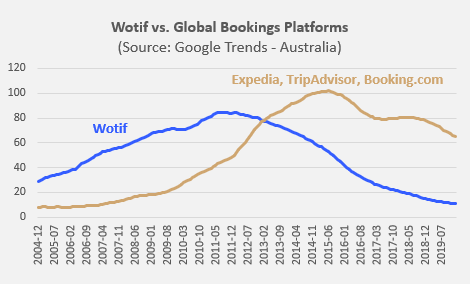

Consider Uber’s network scale benefits compared to hotel aggregators such as Expedia, TripAdvisor or Booking.com. For Uber, strength in the supply of drivers benefits the network predominately at a city level. The majority of commuter activity is within their home city, and therefore the depth of the driver network in neighbouring cities or countries matters little to the commuter. Uber’s global network is, therefore, an aggregation of micro-networks, making it vulnerable to localised competition seeking to carve out city-level niches.

In contrast, leisure travel is often a global experience for consumers, while major hotel chains have multi-national footprints. Both these factors give hotel aggregators increasing relevance with global scale — a much more complicated model for new entrants to replicate. This was a key driver behind the decline of Wotif.com, a once-popular Australian-based booking platform whose national scale was displaced by global hotel aggregators.

Through this lens of participant captivity and network scale, we can assess the increasing strength of network effects in our portfolio companies. We then extend this framework to various enterprise software companies with an opportunity to layer network competitive advantages on to their businesses through time.

Established Network Advantages

Afterpay is building a global two-sided network between consumers and retail merchants. Attracted to its free and simple instalments solution, its highly engaged customer base is funnelled through the platform as retail leads, creating a new merchant channel.

Afterpay’s two-sided network has substantial scale benefits. While consumer relationships are mostly constrained to national boundaries (although cross border eCommerce capability does exist), many critical enterprise-grade merchants have a global footprint, making the ability to serve them with retail leads a global opportunity.

Customer captivity is ultimately dependent on having the highest utility for consumers. In the short-term, this is achievable by having the most use cases (signed merchants), but over time the proposition must grow to maintain high customer captivity. As other businesses have (shamelessly) copied Afterpay’s model, its strategic imperative remains to drive consumer captivity and prevent competitors from building an audience which could offer meaningful retail leads to prospective merchants.

Increasing captivity is achieved through customer incentives that prevent ‘multi-housing’ across multiple instalment fintechs. Afterpay has recently launched a loyalty program designed to incentivise consumers to focus their retail volume through Afterpay to obtain ‘pulse’ status and enjoy loyalty benefits. This has the potential to consolidate the strength of Afterpay’s consumer franchise relative to competing instalment lenders, thus widening its competitive position.

Long-term spending patterns and creditworthiness data on a broad audience of captive consumers presents a valuable (latent) opportunity that can be tapped into by Afterpay, leveraging this asset and expanding its financial relationship with consumers. It could, for example, launch (directly or via third parties) higher value credit products (i.e., car loans, mortgages) linked to an ‘Afterpay credit score’ and offered only to the top quartile of creditworthy consumers.

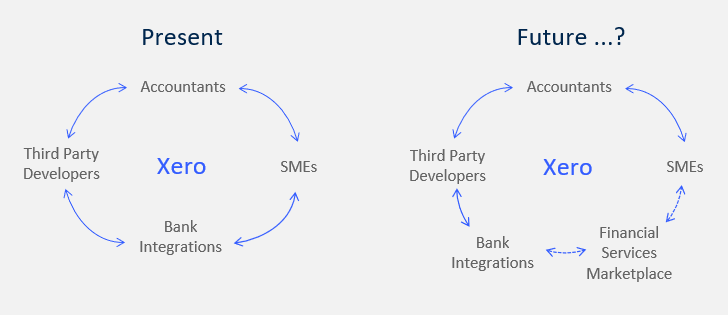

Xero is a two-sided accounting ledger which sits between accountants and SMEs, streamlining the process of maintaining financial records for regulatory and tax purposes. While not a network in the traditional sense, growing penetration of Xero increases the ‘switching cost’ for accountants whereby changing software would not just impact business processes, but also the client relationship.

Xero’s software has direct integrations with ~200 bank and financial service partners; and, is open to developers to build third-party applications for sale in its marketplace, with 800 and counting. This creates a two-sided network between developers and accountants (e.g., practice management software) as well as SMEs (e.g., inventory management).

As accountant and SME participants grow, it attracts more developers to build niche applications and more financial services to build direct integrations, increasing participant functionality and captivity, without the additional capital cost for Xero.

Xero’s scale benefits are significant. Multi-housing is typically lower in B2B than consumer software, whereby it is inefficient for accountants to operate out of multiple applications over time. While an accountant’s SME clients are (likely) grouped at a sub-state level, bank integrations, third party developer marketplace investment and Xero brand awareness efforts require national scale.

Xero is central to SME financial management, providing unique insights into their underlying cash flows. As its global platform matures, its network effect amplifies monetisable opportunities, such as an SME financial services marketplace, internalisation of payments tools and SME financing.

Global Emerging Networks

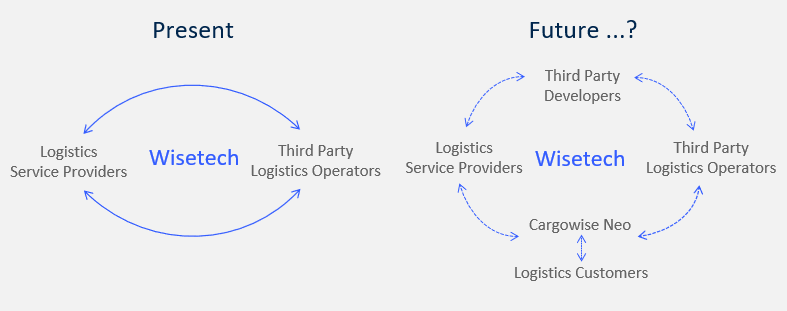

Wisetech is building and deploying enterprise software for cross border logistics management through its flagship product, Cargowise One. The existing network of users is two-sided, whereby existing logistics customers (freight forwarders) encourage service providers (land, sea and air freight operators) to integrate with the software, more readily enabling the management of cargo transport. Utility increases for both sides of the network as participation increases.

Historically, enterprise software evolutions has led to an amalgamation of point solutions pulled together by customers to manage various software needs. Efficiencies are unlocked by migrating to a single platform solution, giving leading software vendors an opportunity to benefit from enterprise software consolidation (see our previous article on these structural trends here).

In Wisetech’s case, Cargowise One’s leadership in core systems software for cross-border logistics presents an opportunity to become a global platform for logistics. Its network structure is large with cross-border logistics resulting in a far more complex network compared to domestic logistics software.

As Wisetech expands into domestic logistics IP, a robust cross-border logistics platform could encourage a more complete global IP roll-out by service providers, such as DHL, as they reduce multi-housing and seek a single global logistics platform.

Over time, Wisetech plans to launch Cargowise Neo which will act as a two-sided interface between service providers (e.g., DHL) and their end clients by which booking, scheduling, finance and visibility of cargo is managed — similar to Xero’s interface for SMEs to engage with accountants. Depending on the degree of utility, this interface would encourage a customer lock-in to service providers utilising Cargowise One, which encourages more providers to switch to Wisetech as they compete for tenders.

Longer-term, Wisetech could increase network depth toward ‘platform status’ by opening up its software to third-party developers, similar to the Xero marketplace. Developers would be able to build niche applications for industry or geographic verticals, building on the Cargowise One core applications, increasing utility for all service providers at the developer’s expense.

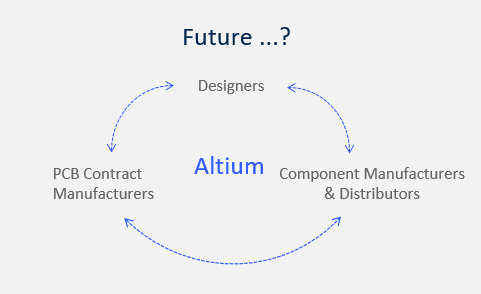

Altium is a leader in software used by electrical engineers to design printed circuit boards (PCB). It is taking market share by offering leading functionality at a lower price. Historically, Altium’s design software has not exhibited network effects, however, the company has indicated strategic ambitions to move along this path.

With the launch of its collaboration interface, Altium 365, the company’s shift to the cloud provides design accessibility to multiple external stakeholders (PCB component distributors and manufacturers) which allows supply chain collaboration on (in progress) design projects. Assuming this new mode of design proves efficient for all stakeholders, it will be the first step toward building network characteristics.

Altium’s longer-term vision is to create a platform in which PCB design, component procurement, and manufacturing orders are centrally completed. If this vision is realised, a three-sided network will be created between designers, manufacturers, and distributors.

Typical of network platforms, early adopters would join for their own competitive advantage (e.g., PCB manufacturers winning volume to fill unutilised production capacity), and late adopters would be compelled to join to avoid the competitive disadvantage of missing out on new business opportunities.

Scale advantage of the network would be substantial, given the global fragmentation of the electronics supply chain. At the same time, Altium file types would strengthen participant captivity as they become the compatibility standard.

Quality Compounds

Businesses with emerging network effects not only have latent pricing power but also retain the potential to build future ecosystem layers which can both deepen a firm’s competitive advantage and create new revenue opportunities. Here lie the beginnings of a quality franchise.

Investors who seek to analyse how a company’s competitive advantage evolves through time are well-positioned to capture superior investment performance. Once a strong network effect has been identified, the superior economic rents achieved by these investments compound through time.

At ECP, we seek to invest in exceptional businesses expanding their economic footprint. For us, considerable time is spent assessing a firm’s competitive advantage and is one of the six pillars of a Quality Franchise. Forensic research surrounding a firm’s competitiveness is vital when evaluating the merits of a Quality Franchise, and is central for any stock to earn a place in our portfolio.

Not already a Livewire member?

Sign up today to get free access to investment ideas and strategies from Australia’s leading investors.

Never miss an update

Enjoy this wire? Hit the ‘like’ button to let us know.

Stay up to date with my current content by

following me below and you’ll be notified every time I post a wire

Damon Callaghan is a Partner at ECP Asset Management, which manage a concentrated portfolio of high quality franchises expanding in the growth phase of their lifecycle.

........

The article has been prepared by ECP Asset Management Pty Ltd (ECP). ECP is a funds management firm based in Sydney, Australia. For further information, visit www.ecpam.com.

This material has been prepared for informational purposes only, and is not intended to provide, and should not be relied on for financial advice. ECP and the analyst own shares in Afterpay Ltd, Altium Ltd, Wisetech Global Ltd and Xero Ltd. ABN 26 158 827 582, AFSL 421704, CAR 44198.

5 topics

4 stocks mentioned

Damon Callaghan is a Partner at ECP Asset Management, which manage a concentrated portfolio of high quality franchises expanding in the growth phase of their lifecycle.

Expertise

Damon Callaghan is a Partner at ECP Asset Management, which manage a concentrated portfolio of high quality franchises expanding in the growth phase of their lifecycle.

Expertise

Comments

Comments

Sign In or Join Free to comment