Credit Suisse hoses down recession forecast

Looking at news headlines, there seems to be a growing consensus of an impending recession by 2020. To support this view, many have pointed towards a flattening yield curve. But James Sweeney, chief economist at Credit Suisse says otherwise. “My view is that we're not likely to have a new recession any time soon”, and that “a more careful look at the yield curve would suggest we probably shouldn't be so sure about this conclusion because it's not so much a flat yield curve that leads to a recession”.

In his presentation at the Credit Suisse Global Perspectives Forum, James makes the case for where the market is getting it wrong on the yield curve, and the key signal you should look out for preceding a recession. I have summarised some highlights below:

On when we will see a recession:

“My view is that we're not likely to have a new recession any time soon. We actually have a consensus right now in the market that a US recession is likely in the next two or three years. I spoke at the ABS East finance conference in Miami a few weeks ago, and 70% of the audience expected a recession within the next few years”.

The biggest question investors should be asking:

“A US recession. I think it's the elephant in the room. The fact the market believes a US recession will come reasonably soon is a big deal. And if we look at the yield curve in the US, we can see why the market has this view”.

Why is an impending recession a popular view?

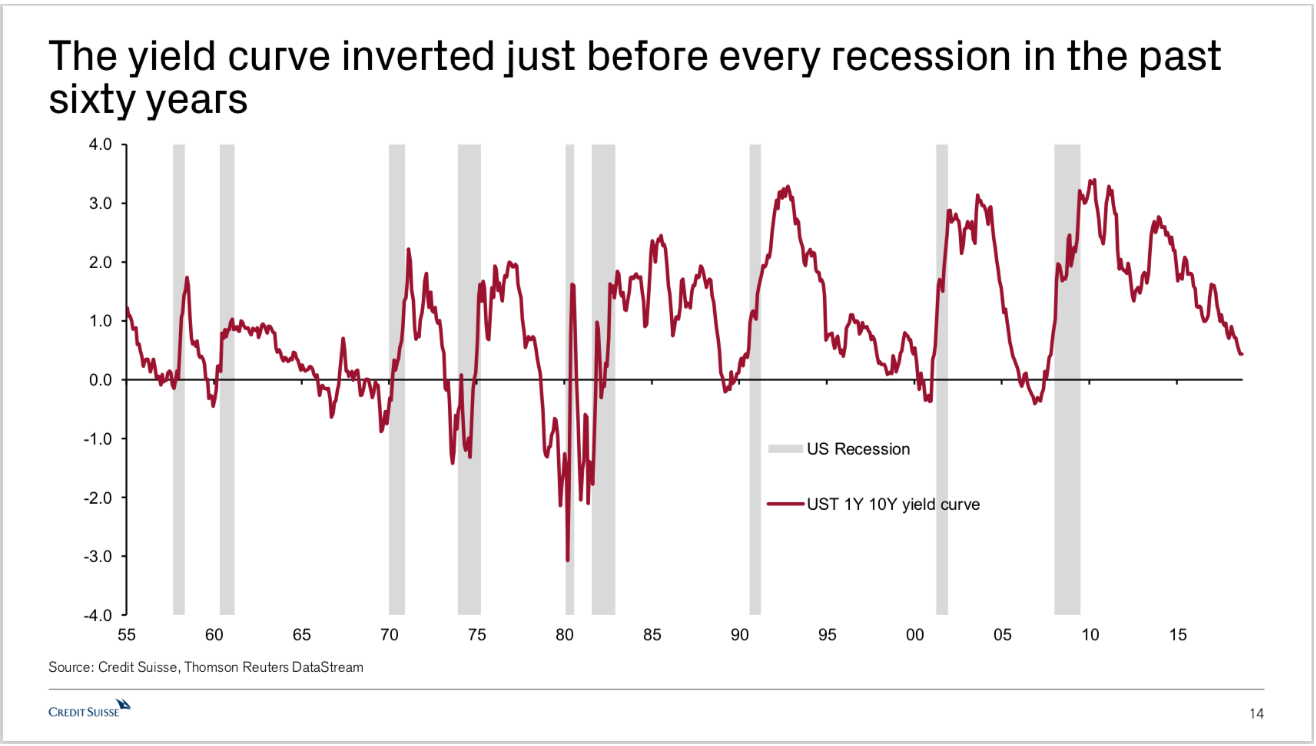

“There are some very simple patterns that markets have followed in the past. So if you look at the yield curve going back to 1955, you can see a very clear pattern. Right before every recession, the yield curve steepens sharply, the yield curve inverts, it then steepens in recession. It steepens again early in the recovery, and then it basically flattens until it's inverted again, and then you get the next recession. And actually, if you look at every recession you have the same pattern again and again. And if you look at where we are now, the yield curve looks to be evolving and continuing to flatten on trend and then, therefore, some people say, "Aha! This recession is coming".

So will a flattening yield curve signal a recession?

“I think this is interesting, but I think the more careful look at the yield curve will suggest that we probably shouldn't be so sure about this conclusion because it's not so much that a flat yield curve leads to recession. Look at the 1990s where the yield curve got to be about where it is now. Then by 1996, it took years before you actually had a recession. Look at the 1960s; you were bouncing around for years. So you can have very long periods of a very flat curve before you actually get a recession. It doesn't tell you a recession is coming.

I actually think the interesting thing about the relationship between the yield curve and recessions is that we've never had a recession when the curve is very steep. So maybe that means when the curve is very steep early in an expansion, it tells you that monetary policy is very easy. And when you have an easy policy, you're less likely to get into trouble.

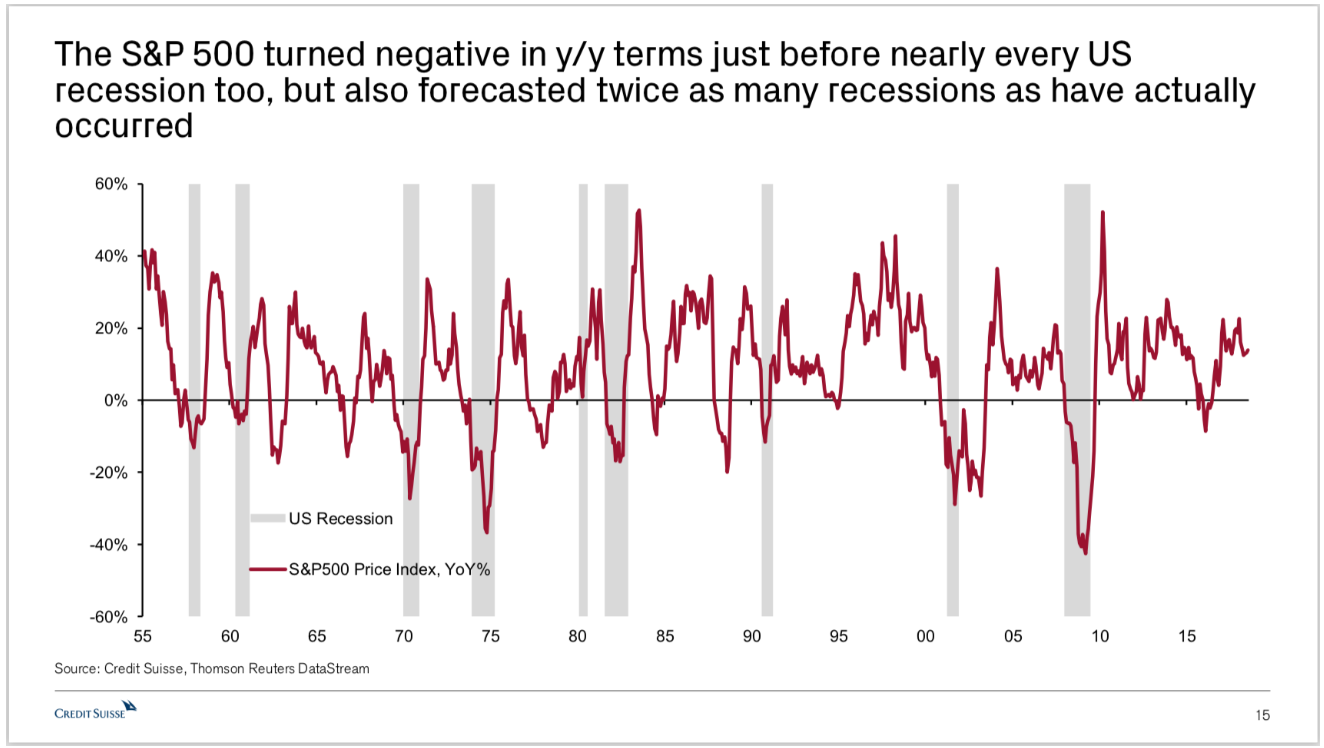

Now monetary policy is getting less easy, so the vulnerability is a little higher, but it doesn't mean the problem is eminent. If you look at the yield curve since 1986, against the year over year change in the S&P, yes, the yield curve was inverted before each recession, but right as the recession was happening, immediately before the recession the same thing happens each time which is that the yield curve suddenly steepens and the stock market suddenly goes down sharply at the time.

What's happening there? What's happening, is the market is saying, "Oh no, earnings are going to be bad." Sell stock and so the stock market is going down, and the bond market is saying, "Oh no, the stock market is going down, earnings are going to be bad, the economy is slowing, we should price for cuts in the Central Bank rate," and so the curve steepens”.

The signal preceding a recession

“So in other words, if you want to forecast a recession, you don't want to just look at the yield curve and observe that it's flat, you want to say, "What's the moment when suddenly earnings expectations are going to fall and policy cuts are going to be priced in?" Because that moment precedes a recession”.

“We're trying to forecast this recession by determining when the market starts pricing in cuts and starts to sharply lower earnings expectations. Our view is that we're not close to that right now”.

So how is Credit Suisse positioned?

John Woods, Asian CIO from Private Banking at the same forum mentioned:

- They remain overweight equities

- The current dip in global markets has presented some attractive opportunities, especially within the technology sector. These companies have “massive cash piles and are less vulnerable to higher interest rates” (technology is more than 5 stocks!)

- They have bumped up fixed income to neutral from underweight

- They don’t see an inflation shock. If you want to hedge against rising interest rates, “back financials”

Never miss an update

Enjoy this wire? Hit the ‘like’ button to let us know.

Stay up to date with my current content by

following me below and you’ll be notified every time I post a wire

Livewire Exclusive brings you exclusive content from a wide range of leading fund managers and investment professionals.

3 topics

Livewire Markets

Livewire Exclusive brings you exclusive content from a wide range of leading fund managers and investment professionals.

Expertise

Livewire Markets

Livewire Exclusive brings you exclusive content from a wide range of leading fund managers and investment professionals.

Expertise

Comments

Comments

Sign In or Join Free to comment