Dividend cuts - options to sustain income

Income is one of the most important considerations for retirees. Once the days of earning a salary have passed, replacing it with a steady stream of income is essential. Unfortunately, relying on income from cash or fixed interest is getting harder as interest rates have experienced a seismic shift over the last decade. Naturally, the search for yield has led retirees to seek more income from equities in recent years.

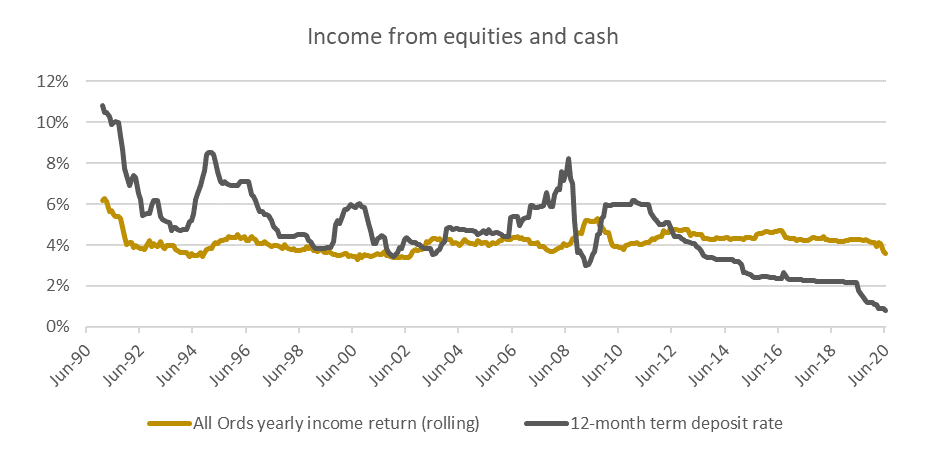

Australian stocks are a great place to invest for income. Over the last two decades the All Ordinaries (All Ords) has delivered an average income return of around 4%. And since 2012, the All Ords income return has been far superior to the 12-month term deposit rate.

Source: Iress, Reserve Bank of Australia

Dividends are not risk-free

While it seems like equities offer a relatively stable yield, retirees should keep in mind that it’s calculated off a very volatile capital base. For example, earning a 4% yield on a $100 capital base is very different from earning the same 4% yield after the capital base has collapsed to $70. Yield chasers learnt this the hard way during 2016 when the dividends of many resource companies were slashed. For example, BHP’s dividend collapsed by 70% in 2016 when its share price fell 48% over one year to its February 2016 low.

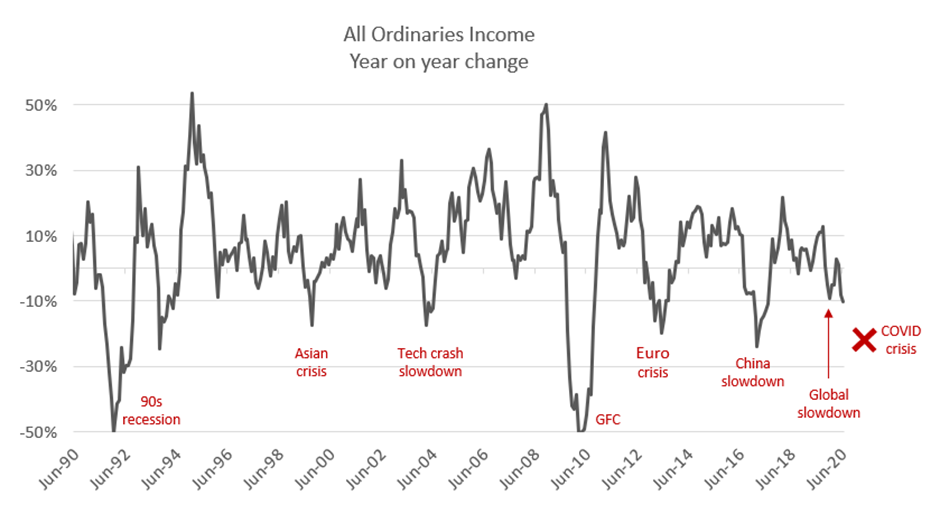

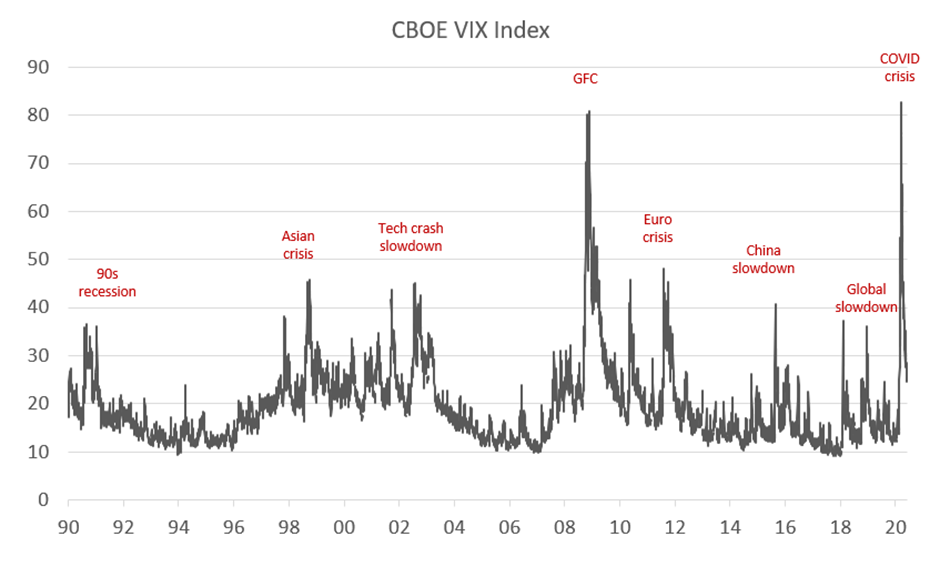

Dividends at certain times can be just as risky as stock prices. Stock prices typically collapse during periods when global growth slows as earnings are revised down. It is no surprise that yield traps often appear when company earnings are unable to support dividend payments during those chaotic periods.

The deepest dividend cuts of around 50% occurred during the 1990s recession and the Global Financial Crisis. However, back then interest rates were relatively high and offered an attractive alternative to the yield on equities. Today with greater allocation to equities in search of income (because interest rates have plummeted), the impact on retirees’ portfolio may be larger.

Source: Iress, Vertium

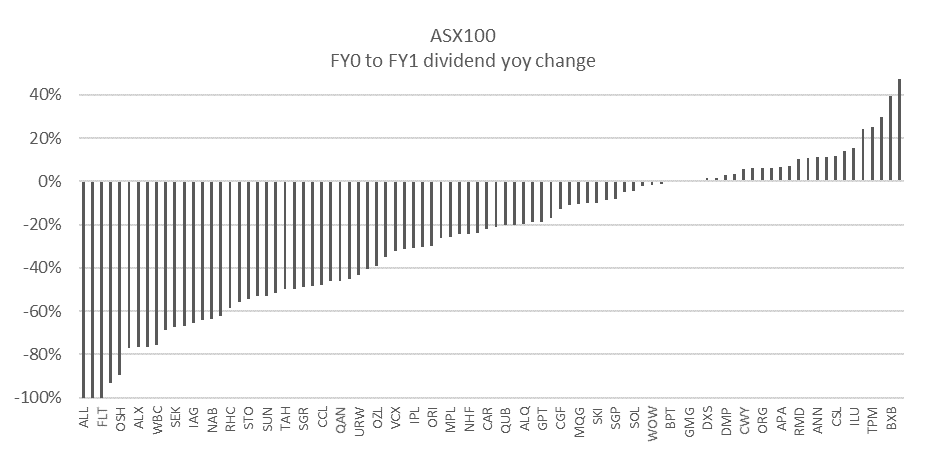

The COVID Crisis is a reminder that income from equities is not risk free. We estimate that the income return from the market is expected to fall by more than 20% over the coming year. The health and financial crises have not spared many sectors of the Australian economy. About two thirds of the ASX100 stocks are expected to have reduced dividends over the next financial year.

Source: FactSet

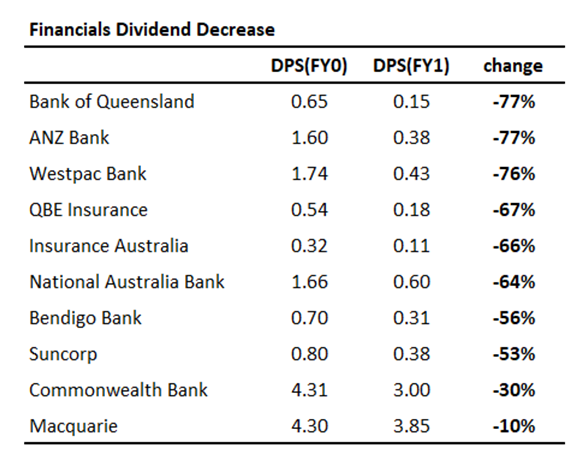

The biggest dividend cuts were experienced in the Travel, Leisure, Energy, and Financial sectors. About half of the decrease in market income was driven by the Financial sector given that it makes up a disproportionately large part (around 20%) of the index. The dividend cuts were encouraged by the Australian Prudential Regulation Authority despite Financial companies having stronger capital positions compared to the GFC – what is good for the financial system is not necessarily good for shareholders.

Source: FactSet

Boosting Your Portfolio with Option Income

Consistent income from equities may be elusive if retirees solely focus on dividends. However, there is a more sustainable way to derive income from equities. While dividends are cut in a crisis, there is another reliable source of income – option income.

At Vertium, we sell options as a core part of our strategy, with the goal of generating additional income for our portfolio. Selling options to generate income is not new. Selling call options on a stock allows the option seller to earn income and potentially forgo future capital upside. Alternatively, selling put options allows income to be earnt and potentially own a stock in the future.

Selling options is much like selling insurance to collect premiums. The key for option sellers is to understand how much capital to forgo on the upside (when selling call options) and how much risk to take on the downside (when selling put options). Like insurance companies having strong underwriting standards to minimise large capital losses, option sellers need to have a strong stock valuation framework to know when to sell options to successfully manage capital.

When option income is combined with dividends and franking, the yield universe in equities improves substantially. A rich yield universe means retirees do not have to chase dividends for income and can avoid yield traps. As a result, a retiree does not have to hold a disproportionately large part of their portfolio in banks just for the sake of generating income. In turn, this will also enable them to achieve better diversification, and hence lower portfolio risk.

There is another key benefit of option income. Market corrections often occur when company earnings are expected to come under pressure, which often lead to dividend cuts. However, during market corrections market volatility typically rises, and this leads to option prices increasing substantially. Hence, when dividends are slashed, increased income from options provides a very good offset during those times.

Source: Refinitiv

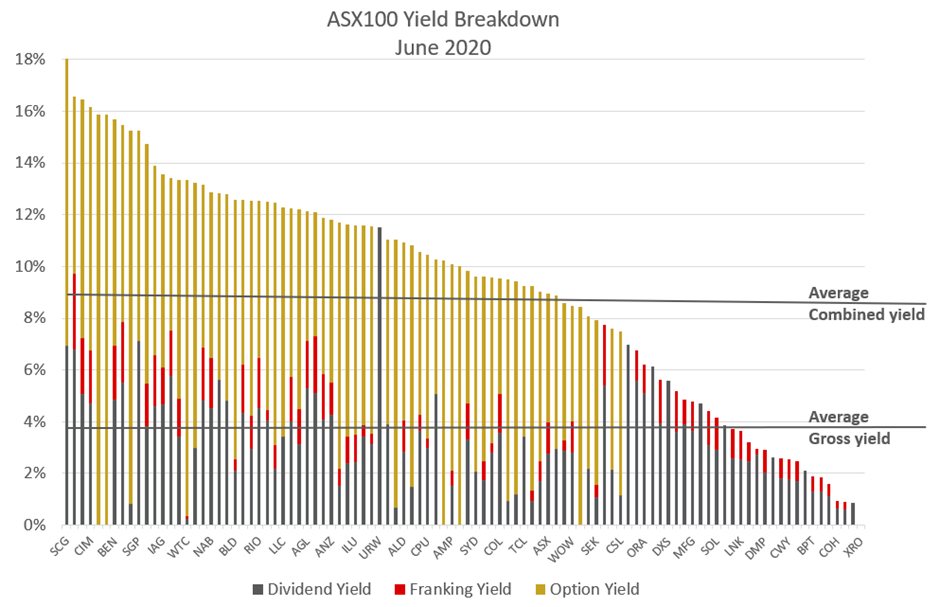

The COVID crisis is no exception. Despite large dividend cuts the combined yield (dividend and option income) universe still offers rich income opportunities. The following chart for the largest 100 ASX stocks highlights that income can be sustained during the COVID crisis when dividends are under pressure.

Note: Dividend yield = next twelve months dividend divided by share price; Franking yield = next twelve months franking from dividend divided by share price; Option yield = 3-month at-the-money option price divided by share price

Source: FactSet, Iress, Vertium

At the end of June 2020, the average dividend yield across the ASX100 is about 3.2% (3.9% grossed up with franking), which is quite low compared to historical standards. However, when option income is added the combined average yield increases significantly to 9.3%. Clearly, the yield potential is significantly enhanced with options. Even low dividend yield stocks such as CSL can generate close to 8% combined yield if options are sold.

Summary

Lower interest rates have driven more retirees to search for yield in equities. While dividends are a great source of income, they can be volatile. The COVID Crisis is a clear reminder that dividends may disappear when companies are under stress.

Income from equities does not just have to be about dividends and franking. Selling options provides another layer of yield that helps smooth the total income profile from equities. Extra income goes directly into the hands of the retiree, where every extra per cent of yield counts. If a high level of sustainable income is achieved, it goes a long way to provide a comfortable lifestyle for retirees.

Get investment insights from industry leaders

Liked this wire? Hit the follow button below to get notified every time I post a wire. Not a Livewire Member? Sign up for free today to get inside access to investment ideas and strategies from Australia’s leading investors.

Never miss an update

Enjoy this wire? Hit the ‘like’ button to let us know.

Stay up to date with my current content by

following me below and you’ll be notified every time I post a wire

Jason founded Vertium Asset Management in 2017 and has around 20 years’ Australian equity investment management experience. He leads Vertium’s investment team and is responsible for the firm’s investment philosophy, process and portfolio management.

5 topics

12 stocks mentioned

Vertium Asset Management

Jason founded Vertium Asset Management in 2017 and has around 20 years’ Australian equity investment management experience. He leads Vertium’s investment team and is responsible for the firm’s investment philosophy, process and portfolio management.

Expertise

Vertium Asset Management

Jason founded Vertium Asset Management in 2017 and has around 20 years’ Australian equity investment management experience. He leads Vertium’s investment team and is responsible for the firm’s investment philosophy, process and portfolio management.

Expertise

Comments

Comments

Sign In or Join Free to comment