Don’t look for the needle in the haystack. Just buy the haystack.

Passive investing is becoming increasingly popular as more investors come to appreciate the liquid and cost-effective exposure it can offer in their portfolios and question the costs and performance of other active styles.

The word ‘passive’ is, in some ways, a misnomer for this style of investing. While passive implies something static and average, passive investments can be flexible and dynamic for a range of investors in building their portfolios for their goals.

What is passive investing?

Generally, investing falls into two areas – passive or active. It can be easiest to explain it in terms of the comparison between the two.

Passive investments follow rules or a methodology to automatically replicate an index or benchmark. For example, one rule might automatically select companies of a certain size (market capitalisation) or in a particular sector. This rules-based approach is generally cheaper to run, in turn meaning it is often lower cost for investors. These are also highly transparent to investors – you know exactly what you have at any given moment. Passive investments were originally designed to simply ‘match the market’ but have since expanded to include a range of targeted, smart-beta strategies. An example of a traditional passive investment is an ETF following a broad-based index like the S&P/ASX 200. A smart-beta ETF still tracks an index but uses tailored filters in the form of fixed selection and eligibility criteria to target objectives such as high yield, low volatility, or alternate weighting methods.

By contrast, active investments are discretionary, meaning investments are made based on a fund manager’s research and philosophy. These can be more labour intensive to run and therefore often have higher costs for investors. The complete holdings are usually not publicly available as they form part of the manager’s intellectual property. Active investments have traditionally been managed funds on platforms where the investment manager might invest based on their view of the economy or based on opportunities for individual companies. Active investments are, generally, designed to ‘beat the market’, aiming to outperform.

The earliest passive investments were mutual funds, with exchange traded funds (ETFs) a more recent innovation in the passive world.

A mutual fund is a professionally managed fund where investors’ money is pooled to purchase assets and the portfolio is managed as a whole. The purchase arrangement is between the fund and the investor, with pricing set at the end of the day and investments or redemptions made by application. Mutual funds can be actively invested or passively invested. They typically have a minimum investment requirement, which can be a barrier to entry for some investors.

ETFs are effectively the same as passive mutual funds with the additional feature that their units can be bought or sold on the stock market in the same way you might buy company shares. They are open-ended, which means there is no limit to the number which can be bought or sold based on investor demand. They don’t have a minimum investment requirement, meaning investors can buy as little as one unit. Traditionally, ETFs were purely passive investments, but more recently, active strategies have become available.

More than one way to track an index

Passive investments can track their index or benchmark in either of two ways: physical replication or synthetic replication.

- Physical replication is the traditional format and involves investing in the securities or assets of the index or benchmark. Full replication involves holding all the securities of the underlying index in the exact same proportions, for example, holding shares in all 200 companies from the S&P/ASX 200. Sampling replication is where only a sample of the underlying securities are held. Sampling can be a more cost-effective and efficient method in situations where the index universe is particularly large, or where the top holdings in an index represent the majority of the portfolio. An example of this might be where the index comprises of 1000 companies, but the bottom 300 companies only represent 1% of the index. The cost v benefit of holding those 300 companies might be higher than excluding them.

- Synthetic replication aims to replicate the benchmark or index performance without holding the underlying securities. Instead it will use derivatives, usually in the form of swap agreements in an aim to generate similar returns. A swap is a type of agreement where two parties agree to exchange cash based on the future value of an asset such as share indices, commodities, interest rates or foreign currencies.

Passive investments (and indices) usually construct their holdings in either of two ways – using alternative weighting, such as equal weighting, or using market capitalisation.

- In market capitalisation weighting, the value of each holding corresponds to the market capitalisation of the company and the contribution to overall performance will be most influenced by the largest companies. The largest company would represent the largest portion of the portfolio and the smallest company at the other end of the spectrum. The S&P 500 and the S&P/ASX 200 are both constructed based on market capitalisation.

- Alternatively weighted investments use different measures to create the composition of the portfolio. For example, based on equal weight, yield or volatility. In equal weighting, each holding makes up the same portion of the portfolio and therefore contributes equally to overall performance. For example, in a portfolio with 10 holdings such as ETFS FANG+ ETF (ASX code: FANG), each holding represents 10% of the total value of the portfolio at the time of each rebalance. This is illustrated in the diagram below.

Equal weighting compared to market capitalisation weighting

Source: ETF Securities

Why use passive investments?

Passive investments are popular for a range of reasons.

Cost tends to be a foremost consideration.

Since passive investments are a rules-based approach, they tend to be less expensive to run, for example, not needing research and simply replicating an index. This means that management fees tend to be lower. Costs to invest can vary further based on the investment type used, but still tend to be lower compared to active options.

For example, minimum investment requirements for passive unlisted investments might be a barrier to entry, compared to using listed investments like ETFs with no minimum investment. Investors in listed investments like ETFs will also need to consider brokerage fees.

Investors have grown more conscious of what they invest in over time, and particularly after the global financial crisis. Passive investments are generally transparent allowing investors oversight of exactly what they hold and the portion of the investment this represents.

Another part of the appeal of passive investments is diversification across a number of companies rather than a smaller more concentrated portfolio if you invested directly or via an active fund. A simple way to think of this is the S&P/ASX 200 Index. If you had $100 to invest, you may only be able to buy shares in a few companies compared to if you invested that same $100 in an ETF giving you exposure to all 200 companies in the index.

Depending on the investment vehicle used, investors may also find passive investing can be flexible and accessible, such as using ETFs which can cover a wide range of styles, assets, sectors and countries.

The steps to start using passive investments depends on the investment product you choose to use. For ETFs, it requires as little as an online trading account to begin.

The history of passive investing

One of the first indices to track market performance was created by Dow & Company in 1885 (1) but it wasn’t until the 1970s when interest in investing based on the index started to increase. Any efforts prior would have needed to be done individually and manually.

Technically, the first index mutual fund was launched by Wells Fargo in 1971 and was an equal weight strategy tracking the New York Stock Exchange (NYSE) for institutional investor Samsonite Luggage (2). This was followed by an S&P 500 tracker in 1973 (3). The first retail index mutual fund was launched by John Bogle from Vanguard in 1976 (4).

Index investing became more accessible again to individual investors with the advent of ETFs.

The first ETF to be listed was the Toronto 35 Index Participation Fund (TIPs) on the Toronto Stock Exchange in 1990, followed by the SPDR S&P 500 ETF (SPY) on the New York Stock Exchange in 1993 (5). Both still trade, with SPY being the largest ETF in the world holding $392bn in assets under management (6).

Australian investors first had access to ETFs on the Australian Securities Exchange (ASX) in 2001. The Australian ETF market is now valued at $56.63bn across 212 products (7), a small fraction of the global $6tr industry (8) with 6,970 products (9).

The theory behind passive investing

The genesis for passive investing stems from the Efficient Markets Hypothesis, developed by Eugene Fama in 1965.

Efficient market theory assumes that companies are correctly priced based on all known information at all times, which means that it’s not possible to consistently outperform the market using fundamental research (10).

Research indicates efficient market theory is true to an extent - the true value of investments does typically win out in the long term – but it’s still possible to find short term patterns and opportunities to help generate higher returns (2).

There can be a time and financial cost to identifying and acting on the short-term. According to Warren Buffett, most average long-term investors would benefit from simply using passive investments (11). While he has been a highly successful ‘value’ investor, his faith in passive investments is such that he has instructed his estate to be invested in 90% passive investments after his death (12).

John Bogle took a similar view in his efforts to develop a retail index mutual fund. His view was that as the economy grows, the market grows, so for most people, being invested in the market will be sufficient (13). To quote him,

“Don’t look for the needle in the haystack. Just buy the haystack.”

When average is not what you think – historic performance

A common criticism of passive investments is that they just receive ‘average’ returns because they are designed to replicate the performance – gains or losses – of the index or benchmark they follow. It is part of human psychology to not want to be average, but average is not always the negative we think (14). Reframing it can help.

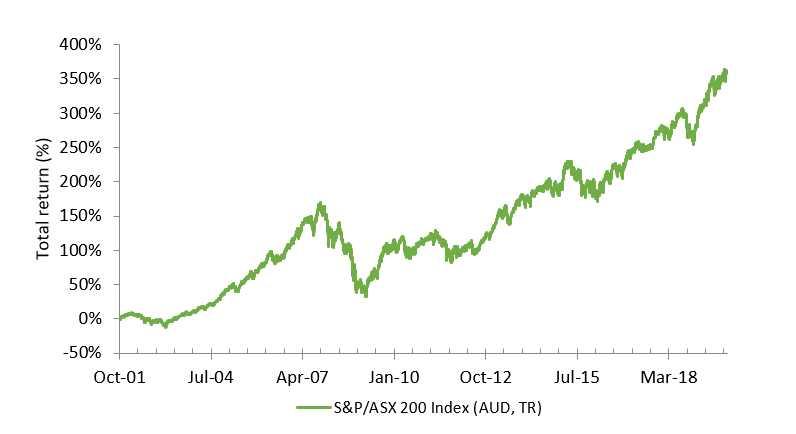

Take the S&P/ASX 200 for example.

If you had invested $10,000 in a passive investment tracking the S&P/ASX 200 like the SPDR S&P/ASX 200 Fund (ASX code: STW) on 24 October 2001 (its launch), it would have been worth $44,270.24 at 30 December 2019 (15) assuming you had reinvested any dividends or other income paid by the fund.

Performance of the S&P/ASX 200 from 24 October 2001 – 30 December 2019

Source: Bloomberg

Warren Buffett famously bet in 2007 that an index fund based on the S&P 500 would offer better returns than a basket of hedge funds over the coming decade – he won this bet in 2017. The index fund gained 125.8% compared to 36% in the hedge funds (16).

This is not to say that the performance of passive funds will always be positive, after all, they are designed to track an index or benchmark. When the S&P/ASX 200 or S&P 500 fall, so too will the investment products tracking them. Should an investor need to sell at that particular point, then they will also crystallise those losses, but it is worth remembering that losses equally occur in other styles of investments and are not exclusive to passive investing.

Active funds aim to outperform their benchmarks – that is, be above the ‘market average’, which is part of their appeal to investors. That doesn’t mean they will succeed.

Standard & Poor’s annual research found that that 83.9% of active Australian equity general fund managers underperformed the S&P/ASX 200 over the ten years to 30 December 2019 on an absolute return basis (17).

Over 2019, the S&P/ASX 200 recorded a total return of 23.4%, while Australian large-cap equity funds recorded a total return of 21.9% (equal weighted strategies) and 21.8% (asset-weighted strategies). Across all asset classes over 10 years, only 58.7% of active funds had not been merged or liquidated.

How to use passive investments in an investment portfolio

While passive investing has traditionally been a buy and hold approach, some investors have started to use it in a more dynamic way to access patterns or opportunities in the short-term. Such investors take an active approach to building their portfolios in terms of risk management, asset allocation and investment selection – but use passive investments to express those decisions.

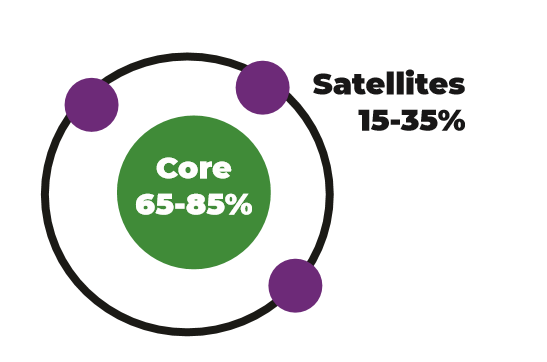

A core-satellite approach to portfolio construction is one option investors may use to invest in passive investments, with an active overlay.

Core-satellite investing is a two-pronged approach to portfolio construction, where the core is made up of passive exposures to major asset classes (mainly equities and fixed income) and the satellite investments are more opportunistic and designed to seek specific growth outcomes, sometimes at higher levels of risk. These might typically be actively managed funds, but could also be investments in individual companies, real estate or one of a growing number of more-targeted passive ETFs. Generally, the core might be 65-85% of the portfolio, depending on the investor’s goals, investment horizon and risk tolerance, while satellites tend to represent 15-35% (18).

Core-satellite investing is a flexible approach and the core will look different according to the individual investor. A high growth strategy might have a core with a higher proportion of ‘riskier’ assets like equities, while a defensive strategy might focus more on assets like gold or fixed income. Investors should consider the core as where they set their strategic asset allocation – where the long-term targets are set for the investment composition to meet your goals, needs and views. By contrast, the satellite is for tactical asset allocation – for shorter-term investments based on market and world conditions that are likely to be more temporary.

Whether a particular investment classifies as core or satellite is also down to the individual investor. For example, an investor with a focus on high growth and a long term view on consumer and technology trends may use an investment like ETFS FANG+ ETF (ASX code: FANG) within their core, whereas an investor with a focus on balanced returns but still a desire for some exposure to these trends might use the same ETF as part of an opportunistic tilt in their satellite investments instead.

In practice, how a core-satellite investment portfolio might look follows.

Investors focused on yield might include exposures to Australian and international shares in their core and then use their satellite component to proactively switch to defensive or growth tilts to bolster their core investments based on market conditions. For example, in volatile conditions similar to those seen during the COVID-19 pandemic, income-focused investors might consider including infrastructure assets which tend to be less vulnerable to market cycles, and can generate income through ETFs like ETFS Global Core Infrastructure ETF (ASX code: CORE). Pending their market view, these types of investments could also form part of the enhanced core portion of the portfolio instead of the satellite.

A growth focused investor by contrast may choose to use the satellite portion of their portfolio to tilt towards themes like technology or emerging markets through passive investments like ETFS Morningstar Global Technology ETF (ASX code: TECH) or ETFS Reliance India Nifty 50 ETF (ASX code: NDIA). Or alternatively, the same investor in a period of market volatility may choose to incorporate additional defensive assets to cushion volatility in other parts of their portfolio, such as via an investment like ETFS Physical Gold (ASX code: GOLD).

Common myths about passive investments

1. Passive investing is a ‘passive’ activity

Choosing to invest in passive investments requires active decisions.

Before choosing an investment, investors need to consider a range of factors such as their goals and financial situation, then in turn, a strategy that might be suitable and investments to fit that strategy. Passive investments come across asset classes, regions, sectors and themes, with varying benchmarks even in the same sector. Investors will also need to consider which replication method for the passive investment is more appropriate for their needs in deciding which product to use.

Some investors may also choose to ‘actively’ manage their passive investments by adjusting them according to market events or opportunities they see.

2. Passive investments only track indices

While many passive investments track indices, they can also track other areas based on tailored benchmarks. They can track commodities, fixed interest, currencies and indices based on sectors or themes, such as climate change or the growth of the middle class in Asia.

3. Passive investing/indexing could cause a liquidity crash, trapping investors

As passive investments, in particular ETFs, have become more popular concerns have been raised as to their ability to withstand periods of extreme volatility and some have questioned whether they may cause or exacerbate market crises. The reasoning is that because the largest ETFs hold a large number of individual securities, when investors liquidate their portfolios they are effectively spreading their selling across an entire market and potentially cause a contagion effect.

To counter this argument, it is firstly worth noting that although the ETF industry is large and growing, it is still only responsible for a small portion of total market trading activity and is dwarfed in size by the overall funds management industry.

Secondly, ETFs now cover such a wide range of different exposures and are cut across many different segments of the market, in a similar way to active funds, making the idea that all ETFs are going to be selling the same securities at the same time overly simplistic.

Thirdly, ETFs have been well stress-tested during real-life events and have mostly behaved as designed. During the global financial crisis, almost no ETFs closed to trading even though many had the ability to do so. Similarly, during the recent COVID-19 market volatility the ETFs that made headlines for being the most under stress were junk bond funds, where the underlying bonds themselves were under stress. ETFs won’t reduce the risks of underlying investments, but there is little evidence to suggest that they exacerbate them either.

4. Low fees = low quality and returns

The old adage is that to get quality and better returns, you need to pay for it, but this isn’t necessarily true when it comes to investing. Paying higher fees doesn’t guarantee a better return, it simply reflects that there may be more activity involved in managing that particular investment, such as through research and analysis, or it reflects a level of profit the fund manager wants to achieve. By contrast, passive investments are rules-based which can require less intervention and research, and therefore, cost less to run.

In fact, Standard & Poor’s annual research found that that 83.9% of active Australian equity general fund managers underperformed the S&P/ASX 200 over the ten years to 30 December 2019 on an absolute return basis (19).

Passive investing may have been traditionally viewed as the “boring” option, but its increasing sophistication and range through the expansion of the ETF market to cover a wide variety of sectors, markets and themes is seeing its popularity rise. Passive investing is becoming increasingly desirable for professional investors and retail investors alike for the ability to access diversified market exposure in a cost-effective package. Passive may sound static, but investors are finding passive investments are a dynamic and flexible way to build their portfolios.

Easy access to a range of opportunities

ETF Securities are Australia’s second oldest ETF provider and the only truly independent, wholly Australian owned ETF manager. For more information on our suite of ETF solutions, hit the contact button below.

References

(1) https://bebusinessed.com/history/history-of-the-stock-market/

(2) https://www.investmentnews.com/the-secret-history-of-index-mutual-funds-69099

(3) www.ft.com/content/807909e2-0322-11e9-9d01-cd4d49afbbe3/

(4) www.ft.com/content/807909e2-0322-11e9-9d01-cd4d49afbbe3/

(6) https://www.ssga.com/au/en_gb/individual/etfs/funds/spdr-sp-500-etf-trust-spy

(7) https://www.asx.com.au/documents/products/ASX_Investment_Products_March_2020.pdf

(8) https://www.statista.com/statistics/224579/worldwide-etf-assets-under-management-since-1997/

(9) https://www.statista.com/statistics/278249/global-number-of-etfs/

(10) Malkiel, Burton G. The efficient market hypothesis and its critics, Journal of Economic Perspectives, Vol 17, No 1, Winter 2003, pages 59-82.

(13) https://sundaybrunchcafe.com/passive-investing-best-thing-since-sliced-bread/

(14) https://www.livescience.com/26914-why-we-are-all-above-average.html

(15) https://www.ssga.com/au/en_gb/individual/etfs/funds/spdr-sp-asx-200-fund-stw

(16) https://money.cnn.com/2018/02/24/investing/warren-buffett-annual-letter-hedge-fund-bet/index.html

(17) SPIVA Australia Scorecard Year End 2019

(18) https://www.nasdaq.com/articles/case-using-coresatellite-portfolios-2016-06-30

(19) SPIVA Australia Scorecard Year End 2019

Disclaimer

This document is communicated by ETFS Management (AUS) Limited (Australian Financial Services Licence Number 466778) (“ETFS”). This document may not be reproduced, distributed or published by any recipient for any purpose. Under no circumstances is this document to be used or considered as an offer to sell, or a solicitation of an offer to buy, any securities, investments or other financial instruments and any investments should only be made on the basis of the relevant product disclosure statement which should be considered by any potential investor including any risks identified therein.

This document does not take into account your personal needs and financial circumstances. You should seek independent financial, legal, tax and other relevant advice having regard to your particular circumstances. Although we use reasonable efforts to obtain reliable, comprehensive information, we make no representation and give no warranty that it is accurate or complete.

Investments in any product issued by ETFS are subject to investment risk, including possible delays in repayment and loss of income and principal invested. Neither ETFS, ETFS Capital Limited nor any other member of the ETFS Capital Group guarantees the performance of any products issued by ETFS or the repayment of capital or any particular rate of return therefrom.

The value or return of an investment will fluctuate and investor may lose some or all of their investment. Past performance is not an indication of future performance.

The Morningstar® Developed Markets Technology Moat Focus IndexSM was created and is maintained by Morningstar, Inc. Morningstar, Inc. does not sponsor, endorse, issue, sell, or promote the ETFS Morningstar Global Technology ETF and bears no liability with respect to that ETF or any security. Morningstar® is a registered trademark of Morningstar, Inc. Morningstar® Developed Markets Technology Moat Focus IndexSM is a service mark of Morningstar, Inc.

The financial instrument is not sponsored, promoted, sold or supported in any other manner by Solactive AG nor does Solactive AG offer any express or implicit guarantee or assurance either with regard to the results of using the Index and/or Index trade mark or the Index Price at any time or in any other respect. The Index is calculated and published by Solactive AG. Solactive AG uses its best efforts to ensure that the Index is calculated correctly. Irrespective of its obligations towards the Issuer, Solactive AG has no obligation to point out errors in the Index to third parties including but not limited to investors and/or financial intermediaries of the financial instrument. Neither publication of the Index by Solactive AG nor the licensing of the Index or Index trade mark for the purpose of use in connection with the financial instrument constitutes a recommendation by Solactive AG to invest capital in said financial instrument nor does it in any way represent an assurance or opinion of Solactive AG with regard to any investment in this financial instrument. Solactive AG will not be responsible for the consequences of reliance upon any opinion or statement contained herein or any omission.

ETFS Reliance India NIFTY 50 ETF offered by ETFS Management (AUS) Limited or its affiliates is not sponsored, endorsed, sold or promoted by NSE INDICES LTD and its affiliates. NSE INDICES LTD and its affiliates do not make any representation or warranty, express or implied (including warranties of merchantability or fitness for particular purpose or use) to the owners of ETFS Reliance India NIFTY 50 ETF or any member of the public regarding the advisability of investing in securities generally or in the ETFS Reliance India NIFTY 50 ETF linked to the NIFTY 50 Index or particularly in the ability of the NIFT Y 50 Index to track general stock market performance in India. Please read the full Disclaimers in relation to the NIFTY 50 Index in the Product Disclosure Statement.

Source ICE Data Indices, LLC, is used with permission. “NYSE® FANG+TM” is a service/trade mark of ICE Data Indices, LLC or its affiliates and has been licensed, along with theNYSE® FANG+TM Index (“Index”) for use by ETFS Management (AUS) Limited in connection with ETFS FANG+ ETF (FANG) (the “Product”). Neither ETFS Management (AUS) Limited, ETFS FANG+ ETF (the “Trust”) nor the Product, as applicable, is sponsored, endorsed, sold or promoted by ICE Data Indices, LLC, its affiliates or its Third Party Suppliers (“ICE Data and its Suppliers”). ICE Data and its Suppliers make no representations or warranties regarding the advisability of investing in securities generally, in the Product particularly, the Trust or the ability of the Index to track general market performance. Past performance of an Index is not an indicator of or a guarantee of future results.

ICE DATA AND ITS SUPPLIERS DISCLAIM ANY AND ALL WARRANTIES AND REPRESENTATIONS, EXPRESS AND/OR IMPLIED, INCLUDING ANY WARRANTIES OF MERCHANTABILITY OR FITNESS FOR A PARTICULAR PURPOSE OR USE, INCLUDING THE INDICES, INDEX DATA AND ANY INFORMATION INCLUDED IN, RELATED TO, OR DERIVED THEREFROM (“INDEX DATA”). ICE DATA AND ITS SUPPLIERS SHALL NOT BE SUBJECT TO ANY DAMAGES OR LIABILITY WITH RESPECT TO THE ADEQUACY, ACCURACY, TIMELINESS OR COMPLETENESS OF THE INDICES AND THE INDEX DATA, WHICH ARE PROVIDED ON AN “AS IS” BASIS AND YOUR USE IS AT YOUR OWN RISK.

Information current as at 5 May 2020.

Never miss an update

Enjoy this wire? Hit the ‘like’ button to let us know.

Stay up to date with my current content by

following me below and you’ll be notified every time I post a wire

For more than a decade, our mission has been empowering investors with unexplored and intelligent solutions. Our ETFs span thematics, commodities, income, leveraged, international access and digital assets.

1 topic

4 stocks mentioned

Global X ETFs

For more than a decade, our mission has been empowering investors with unexplored and intelligent solutions. Our ETFs span thematics, commodities, income, leveraged, international access and digital assets.

Expertise

Global X ETFs

For more than a decade, our mission has been empowering investors with unexplored and intelligent solutions. Our ETFs span thematics, commodities, income, leveraged, international access and digital assets.

Expertise

Comments

Comments

Sign In or Join Free to comment