Dull with a shiny side – the case for Alumina

Alumina Limited is an example of a company whose currently depressed earnings appear more cyclical than structural and which, given recent price weakness, we believe may offer attractive upside potential.

Before discussing the investment appeal of Alumina, some background knowledge of how aluminium is made will be useful. It all begins with the mining of bauxite, a reddish clay material comprised mainly of aluminium oxide, silica, iron oxides and titanium dioxide. (Bauxite is to aluminium what iron ore is to steel.) Once mined, the bauxite is refined using the Bayer Process. This involves heating the bauxite, together with caustic soda, in a pressure vessel in order to dissolve and separate the aluminium oxide (alumina) from the other compounds present. Alumina is later smelted using an energy intensive electrolysis process to produce pure aluminium metal.

As a rough rule of thumb, it requires four to six tonnes of bauxite (depending on grade) to manufacture two tonnes of alumina, which in turn produces one tonne of aluminium.

About Alumina and its sole asset

Alumina’s sole asset is its 40% joint venture interest in Alcoa World Alumina and Chemicals (AWAC). AWAC is one of the world’s largest miners of bauxite and refiner of alumina. It derives the vast majority of its earnings from selling alumina (which it produces from its own bauxite) to aluminium smelters around the world, including to Alcoa Corporation (Alcoa), who own the other 60% of AWAC. In addition to this, it also sells bauxite ore to alumina refineries that don’t have captive sources of bauxite, predominantly in China, and it produces a small amount of aluminium from the Portland smelter in Victoria. In 2020, it expects to produce 12.8 million tonnes of alumina, 6.5 million tonnes of bauxite for third party sales and close to 160 thousand tonnes of aluminium.

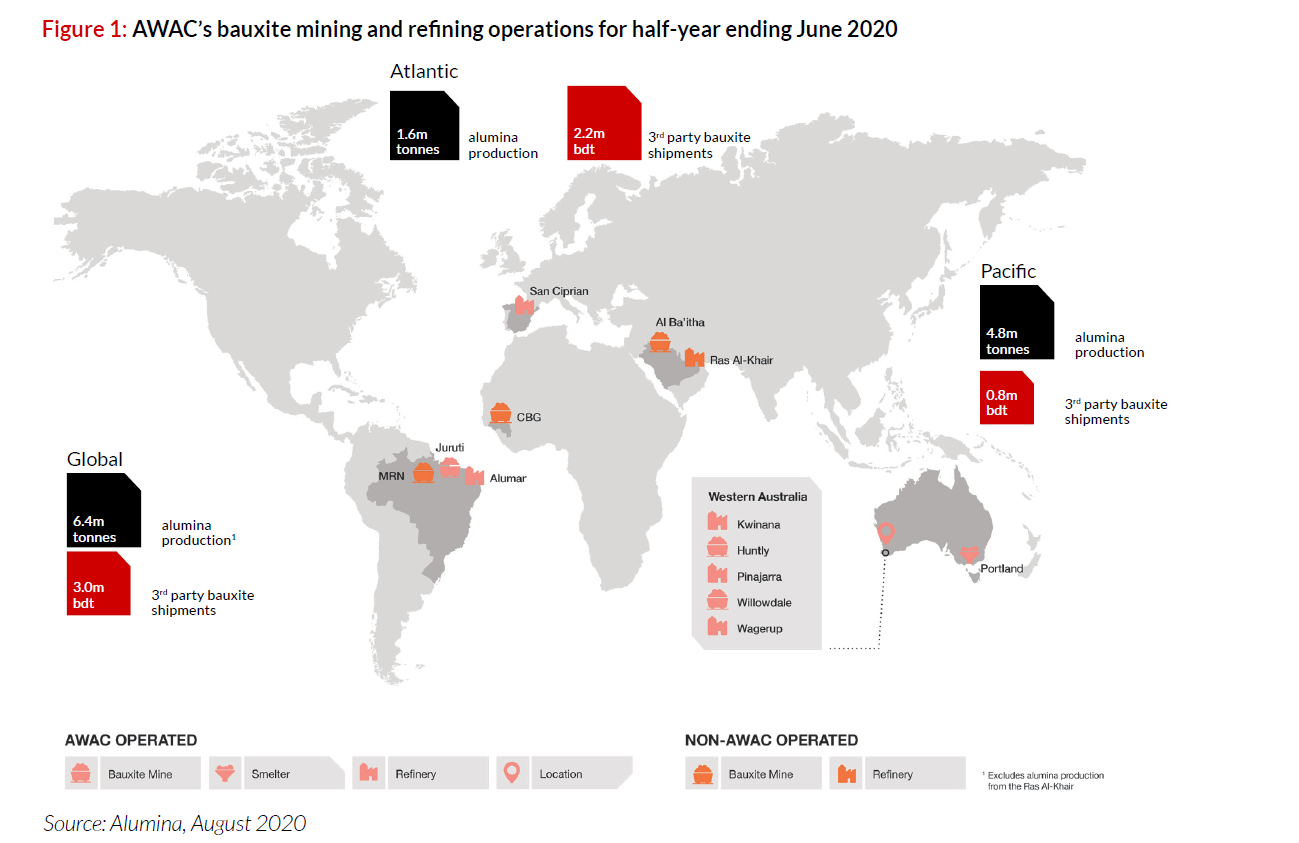

AWAC’s operations are geographically dispersed (refer to Figure 1) although its West Australian bauxite mines (Huntly and Willowdale) and refineries (Wagerup, Kwinana and Pinjarra) are among the lowest cost and most profitable in the world. Other assets include its share of the Juruti and MRN bauxite mines and Alumar refinery in Brazil, a 25.1% interest in the Ma’aden mining and refining operations in Saudi Arabia, refining assets in Spain (San Ciprian) as well as bauxite mining interests in Guinea.

Click to enlarge

AWAC’s competitive advantages

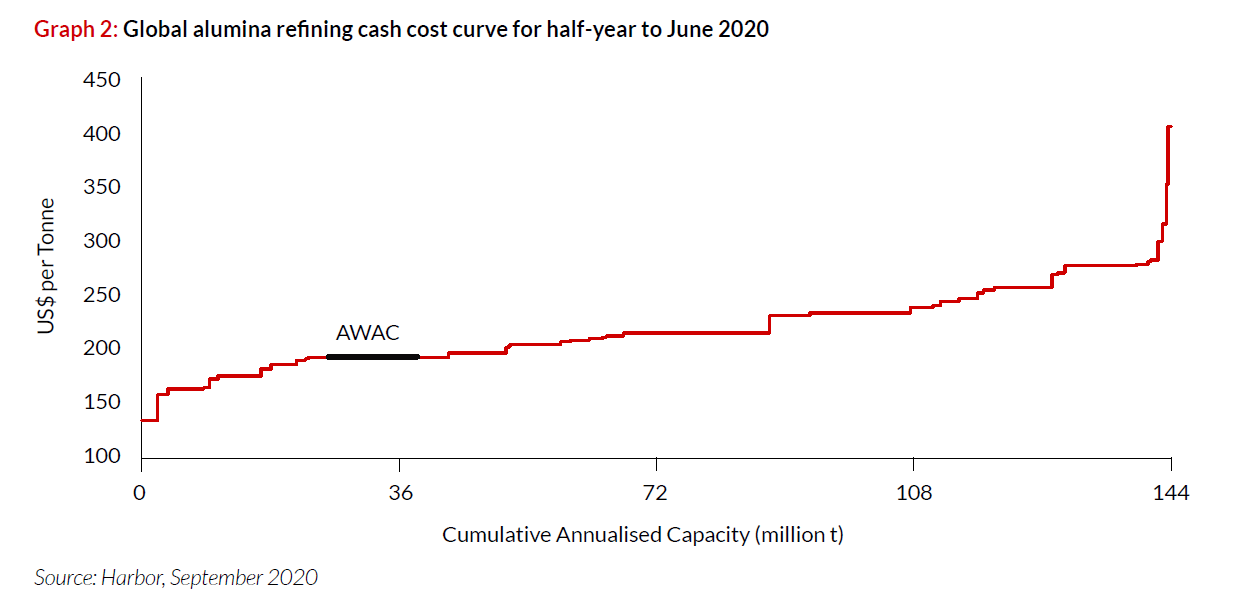

A number of attributes make AWAC’s refining operations among the lowest cost operations in the world (as depicted in the cost curve in Graph 2). Most notable are the location and properties of its bauxite. With a low level of reactive silica at AWAC’s Australian mines, it requires less caustic soda and less heat in the refining process, two significant cost components. Also, the co-location of its refining assets to these long-life bauxite reserves results in logistical savings. This and its low mining costs are also a source of competitive advantage. AWAC’s cash costs of production are below US$200 per tonne (/t) with total costs after all sustaining capital spending requirements approximately US$215/t. These costs put it within the first quartile of the industry cost curve.

Click to enlarge

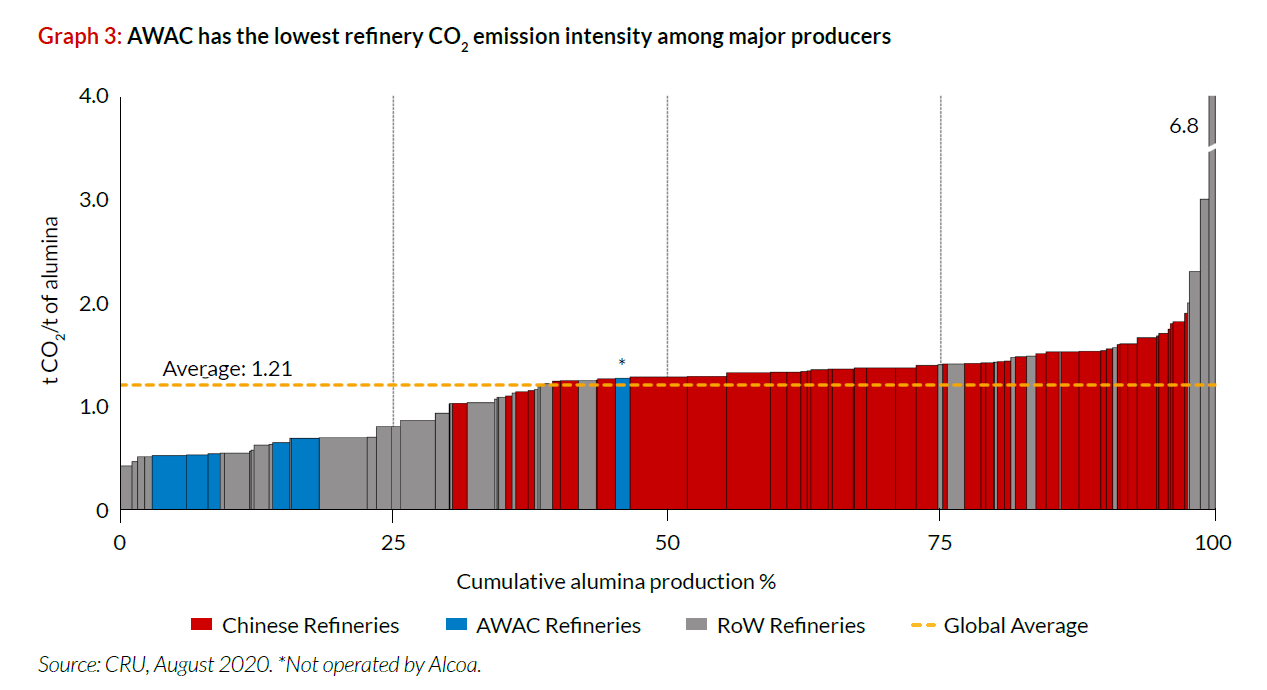

Importantly, these same attributes that make AWAC a low-cost producer (largely low temperature gas-fired refineries) also contribute to AWAC’s favourable emissions intensity relative to industry peers. As can be seen in Graph 3, AWAC emits on average around half the CO2 per tonne of alumina produced compared with the industry average. This complements its excellent track record in sustainably disposing of the red mud residue generated during the refining process.

Share price weakness and contributing factors

Alumina has underperformed the sharemarket by over 50% since its recent peak in October 2018. A number of factors have contributed to this weakness, none more so than today’s weak alumina prices and resulting depressed profits.

Early in 2019, the Brazilian Government removed production constraints it had earlier imposed at the Alunorte alumina refinery (the world’s largest refinery outside of China with production of close to six million tonnes per annum). This reversed a supply deficit that had caused prices to spike to over US$700/t. Prices quickly retreated from those lofty levels once Alunorte commenced operations in full again. In 2020, COVID-19 has significantly reduced demand for aluminium (and alumina) outside of China, adding further to excess alumina supply. Prices have fallen to about US$270 per tonne, 20% below the average over the past 10 years.

Adding to the price weakness, China, a large importer of alumina five to ten years ago, has also reduced its imports. This has exacerbated the excess supply outside China and depressed the ex-China alumina price. China’s alumina production has typically been significantly higher cost than that produced outside of China, largely due to its energy intensity and the amount of caustic soda required due to the high silica content of its bauxites. This competitive disadvantage has been reduced by the post-COVID-19 declines in energy and caustic soda prices which has not only seen the industry cost curve fall, but also flatten. Despite these falling costs, at least 20% of Chinese alumina refining (10% of world production) is still loss-making at current prices.

Alumina appears to offer compelling value

With a market capitalisation of just under US$3 billion and next to no debt, investors in Alumina pay US$600 per tonne of annual alumina production capacity. Despite the prevailing low alumina prices (US$270/t versus 10-year average price in the mid-US$300s) and after known increases in AWAC’s costs from new gas supply contracts coming on stream, we expect Alumina to generate margins of close to US$50/t of production.

Alumina trades at 17 times the resulting post-tax earnings and with a near 100% dividend payout ratio, trades on a fully-franked dividend yield of almost 6%. For a high-quality, long-life resource company, this would be attractive to us at the best of times, let alone in today’s low interest rate environment. But the real attraction is that earnings have the potential to increase significantly from here.

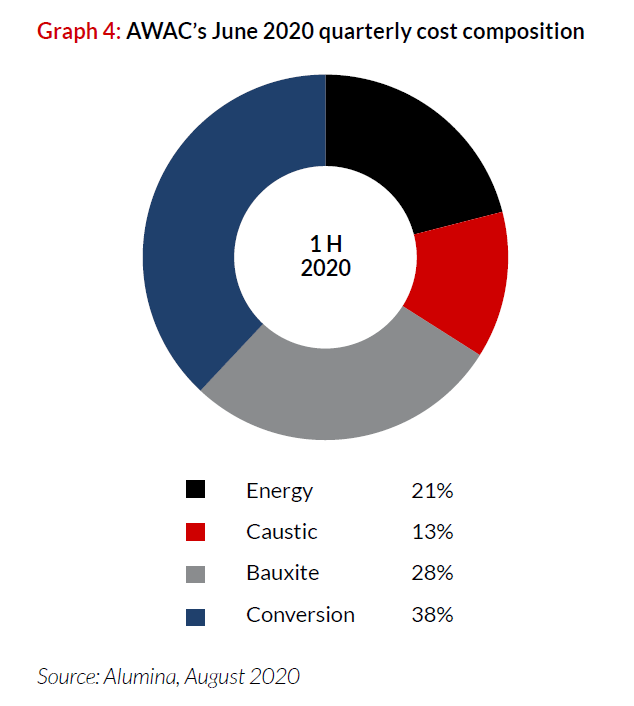

As already mentioned, approximately 20% of Chinese alumina refining (10% of world production) is already loss-making at current prices, an important backdrop for higher commodity prices. There are also significant cost pressures on the horizon. Prices for oil and coal, upon which much of China’s alumina production (and some of the production outside of China) depends, are low today. Vast swathes of world production are loss-making and any meaningful increase in these fuel prices will result in significantly higher input costs for those producers reliant on these fuel sources. Asian caustic soda prices are also at multi-year lows and unlikely to stay at these levels. Also, China is becoming increasingly reliant on costlier imported bauxite to feed its refineries. Energy, caustic and bauxite comprise 65% of AWAC’s refining cost base (as seen in Graph 4) and this is higher for other alumina refineries costs. It is likely that the cost base of alumina refining will increase significantly and, along with it, the alumina price.

AWAC is well positioned to benefit from this. AWAC’s energy needs are mainly met via long-term gas contracts; they will be less impacted from rising oil and coal prices upon which they are not reliant. While a rise in caustic prices will impact AWAC’s cost base, its low silica bauxite makes it less reliant on caustic than other alumina producers. And AWAC does not rely on third party bauxite, with its refineries mostly co-located with its own bauxite mining operations. Any rise in alumina prices to offset these cost imposts should therefore result in the cost curve steepening and AWAC remaining at the lower end. AWAC’s operating margins would therefore expand and with it, Alumina’s profits.

An alternative way to look at Alumina is with reference to replacement costs

It is also useful to compare Alumina’s price today to the cost to replace its 40% share of AWAC’s alumina production. The cheapest refineries in China cost about US$600 – US$800 per tonne of annual capacity to build. They are generally not integrated (i.e. they rely on third-party purchased bauxite, usually imported) and are therefore relatively high cost operators. Outside of China, refineries cost between US$1,000/t of annual capacity (e.g. Indonesia) and over US$2,000/t (Western world).

At US$600/t of capacity, an investor in Alumina today can buy refining capacity that ranks among the world’s lowest operating cost capacity for 30% to 60% of the cost to replace the same capacity outside of China. Alumina investors today buy low-cost, long-life capacity integrated with high quality bauxite for a similar amount to high-cost, non-integrated capacity in China!

What might go wrong?

Two obvious pushbacks to our thesis exist.

- The first pushback is that AWAC is the subject of a A$900 million transfer pricing tax dispute with the Australian Tax Office. Alcoa, the operator of the AWAC joint venture, appears to have a reasonable basis for its belief that the ATO’s claims have no merit. But even if they’re wrong, and taking into account Alumina’s 40% share of these claims, the outcome of this dispute does not appear to materially impact our thesis.

- The second pushback relates to the potential for a significant reduction in demand for aluminium (and alumina) given the COVID-19 induced economic downturn. This would further increase the excess alumina supply and cause alumina prices to fall from here. Were this to happen, Alumina would be well positioned relative to its industry peers, given its low-cost operations and near-zero financial leverage. Significant amounts of world production would be loss-making and long-term investors in Alumina, with its share of long-life reserves and strong industry position, could afford to wait out the storm.

It mustn’t be forgotten that the scenario above would also have far-reaching ramifications for industries unrelated to the aluminium supply chain and sharemarkets more broadly. When taking a long-term perspective, Alumina looks undervalued on almost all metrics and even with an extended weak economic backdrop, we believe that Alumina Limited is better positioned than the average company in our investment universe.

The

above wire is an extract from Allan Gray Australia’s September 2020 Quarterly

Commentary, which you can read in full here

Want to learn more?

Contrarian investing is not for everyone, however there can be rewards for the patient investor who embraces Allan Gray’s approach. To stay up to date with our latest thinking, hit the follow button below or contact us for further information.

Never miss an update

Enjoy this wire? Hit the ‘like’ button to let us know.

Stay up to date with my current content by

following me below and you’ll be notified every time I post a wire

Simon Mawhinney is the Managing Director and Chief Investment Officer of Allan Gray Australia, where he leads the company’s investment strategy and oversees the performance of its Australian equity and multi-asset portfolios. Simon joined Allan Gray in 2006 as an analyst, bringing with him a strong background in finance from previous roles at Alliance Bernstein, Macquarie Bank, and Deloitte & Touche. Simon holds a Bachelor of Business Science (First Class Honours) in Finance and Business Strategy, along with a Postgraduate Diploma in Accounting, from the University of Cape Town. He was a Chartered Accountant and is a CFA Charterholder. Known for his contrarian, long-term, value-driven investment philosophy, Simon speaks frequently at industry events and appears in media interviews, offering perspectives on specific securities, as well as portfolio positioning and the Allan Gray contrarian investment strategy.

........

Past performance is not a reliable indicator of future performance. There are risks involved with investing and the value of your investments, including in the Allan Gray Funds, may fall as well as rise. This article represents Allan Gray's view at a point in time and may provide reasoning or rationale on why we bought or sold a particular security for the Allan Gray Funds or our clients. We may take the opposite view/position from that stated, as our view may change. This article constitutes general advice or information only and not personal financial product, tax, legal, or investment advice. It does not take into account the specific investment objectives, financial situation or individual needs of any particular person and may not be appropriate for you. Before deciding to acquire an interest in any financial product or making any other investment decision, please read the relevant disclosure document. We have tried to ensure that the information in this article is accurate in all material respects, but cannot guarantee that it is.

4 topics

1 stock mentioned

Simon Mawhinney is the Managing Director and Chief Investment Officer of Allan Gray Australia, where he leads the company’s investment strategy and oversees the performance of its Australian equity and multi-asset portfolios. Simon joined Allan...

Expertise

Simon Mawhinney is the Managing Director and Chief Investment Officer of Allan Gray Australia, where he leads the company’s investment strategy and oversees the performance of its Australian equity and multi-asset portfolios. Simon joined Allan...

Expertise

Comments

Comments

Sign In or Join Free to comment