18 Easter treats for income investors

Leigh Winton

FIIG

Over the years, we’ve presented a range of sample portfolios to new and existing clients on the types of fixed income investments available. Our Australian dollar investment grade portfolio was developed by our Portfolio Strategy and Research teams to show an example portfolio and the associated yields on offer.

Investment grade means that a ratings agency has assessed the issuers and that the minimum rating is BBB- or equivalent. Please see a glossary at the end of the note for an explanation of some of the terms.

We use a mix of bond types in our portfolio – fixed, floating and inflation linked, in line with the Portfolio Strategy (PSS) recommendation. Currently, PSS suggest that investors allocate roughly equal percentages to the three different types of bonds – fixed, floating and inflation linked securities. As a reminder, fixed rate bonds have the same regular interest (or coupon) payments whereas floating rate securities have adjustable interest as they are linked to the Bank Bill Swap Rate (BBSW).

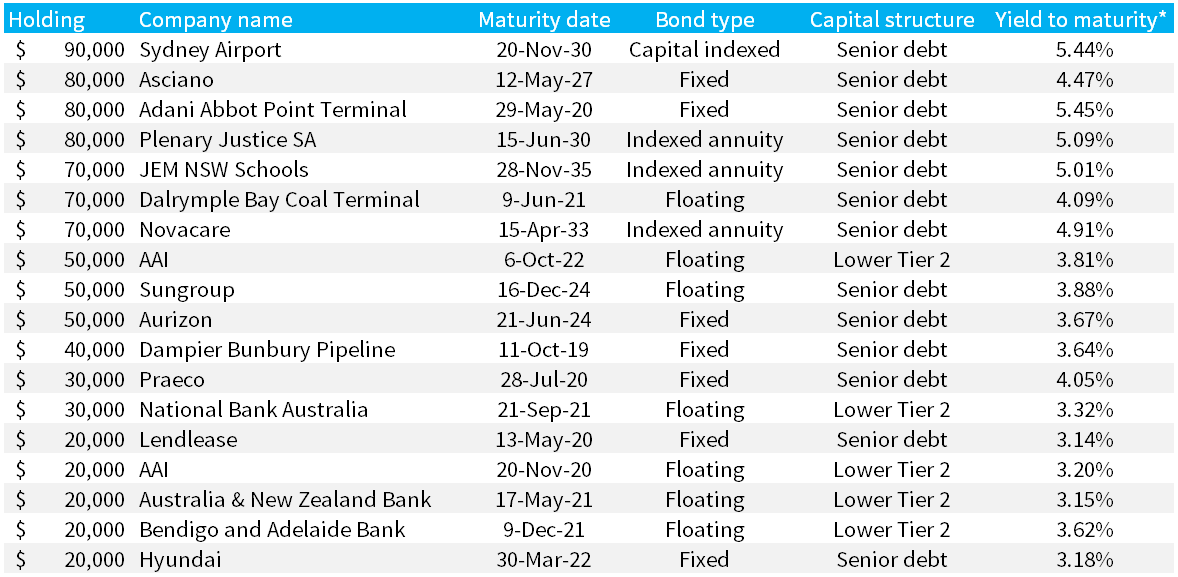

Sample investment grade portfolio

Source: FIIG Securities, prices accurate as of 27 March 2018

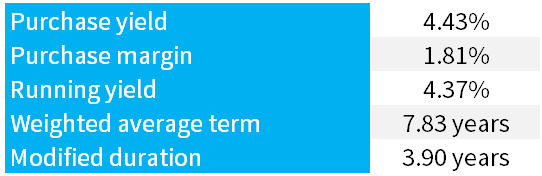

Source: FIIG Securities

Please see the glossary at the end for the definition of each term.

The purchase yield or yield to maturity (YTM) is 4.43%, which we believe offers a very strong return for a low risk portfolio.

We prefer the YTM as a return as this takes into account all the expected cashflows from the underlying bonds. This is different to shares where investors often focus on the income or dividend return without taking into account any movement in the share price. This is where a bond portfolio has a huge advantage over shares as it offers greater certainty with the protection of a maturity date which allows us to model of a final return value, but which shares can never do as they rely on investors making the decision to sell to recoup capital.

The investment grade portfolio has a high allocation to senior debt, ordinarily above 65%. The Portfolio Strategy team chooses these bonds as legally, if the company goes into a wind-up or liquidation, any funds available for debt and equity will be repaid to senior investors first. Senior debt comprises both senior secured and unsecured obligations.

The investment grade portfolio only contains Australian dollar denominated bonds and has a high allocation to bonds linked to infrastructure. Although we practise sector diversification, we are typically comfortable with larger allocations to this sector as it is typically a stable sector which exhibits low volatility. Sydney Airport is a common used security in this sector, as is Sungroup, which is the finance subsidiary of a Transurban-led consortium managing a network of Queensland toll roads.

In general terms, we look to have at least ten bonds in smaller portfolios and at least fifteen to twenty bonds in larger portfolios. This is to reduce concentration risk in terms of limiting exposure to any one particular name. In our opinion any security with a 10% or greater allocation needs to have a very firm conviction by an investor. Thus essential infrastructure asset Sydney Airport is the only security with an exposure of more than 10%. .

The projected cashflows for these bonds are shown on the second page of the linked portfolio. As inflation linked bonds pay returns linked to the CPI rate, we use the RBA mid-point target of 2.5%, although inflation has been lower than this of late.

Similarly, with floating rate notes, we need to use a projected rate for future cash flows, accepting that these rates will change as expected future interest rate levels change. The market uses an interest rate swaps curve to help estimate the future income/ returns of floating rate bonds.

FIIG is Australia’s leading fixed income specialist. To learn more about our fixed income offerings please click here

Glossary

Coupon

The rate of interest paid on a fixed income investment or bond. Coupons can be paid annually, semi-annually or quarterly or as agreed in the terms of the security.

The coupon rate can be fixed or floating for the term of the security. If it is a floating rate then it is likely that it will be linked to a benchmark such as the 90 day bank bill rate. The coupon rate is set by the issuer based on a number of factors including prevailing market interest rates and its credit rating.

Fixed rate bond

A fixed rate bond is a security that pays a fixed pre-determined distribution or coupon. The coupon of a fixed rate bond will be set at the time of issue and not change during the life of the bond. The Commonwealth Government, state governments, banks and corporates all issuefixed rate bonds in Australia.

Floating rate bond

A floating rate note (FRN) or bond is a security that pays a coupon linked to a variable benchmark.

In Australia, most FRNs pay a coupon set as a margin above the bank bill swap rate (BBSW) which is the market benchmark three month interbank rate. The actual coupon for an interest period will be determined at the start of that period by applying the margin to the three month BBSW rate on the first day of the coupon period. The three month BBSW rate will rise and fall over time based on prevailing interest rates. The margin is fixed and will be set at the time of issue.

Inflation linked bond

A bond whose base payment rises and falls with the Consumer Price Index (CPI).

Credit rating

Is a measure of credit quality assigned to anissuer and also to particular securities by a professional rating agency. Securities are broadly divided into investment grade (those rated above BBB- by S&P and Fitch, or Baa3 by Moody's) and sub investment grade or speculative (everything below). Due to ASIC regulations, credit ratings in Australia can only be disclosed to "wholesale" investors.

Modified duration

Modified duration (sometimes called Macaulay duration) is a measure of the price sensitivity of a bond to interest rate movements. Typically, modified duration provides an estimate of how a bond will change in price for a 100 basis point (bps) or a 1% movement in interest rates.

Purchase yield

See Yield to maturity.

Running yield

The interest rate on an investment expressed as a percentage of the capital invested. It takes no account of the capital accumulated. It is used to describe the income investors receive from their portfolio as a percentage of market value of the securities.

Yield to maturity

The return an investor will receive if they buy a bond and hold the bond to maturity. It refers to the interest or dividends received from a security andare usually expressed annually or semi-annually as a percentage based on the investment's cost, its current market value or its face value. Bond yields may be quoted either as an absolute rate or as a margin to the interest rate swap rate for the same maturity.

It is a very useful indicator of value because it allows for direct comparison between different types of securities with various maturities and credit risk.

Note that the yield and coupon are different.

Weighted average term

The weighted average term to maturity measures the average time until maturity across all positions within a bond portfolio. To calculate the weighted average term, you must add together the percentage value of each position within the portfolio and then multiply this percentage by the number of years (and months) until maturity.

Never miss an update

Enjoy this wire? Hit the ‘like’ button to let us know.

Stay up to date with my current content by

following me below and you’ll be notified every time I post a wire

Leigh has over 30 years’ experience within Financial markets across Fixed Income, Foreign-Exchange, Derivatives and Commodities. He has a background in Structuring, Product development and sales. Explaining financial products in simple terms continues to be a key part of his roles.

2 topics

Leigh Winton

Head of Portfolio Strategies

FIIG

Leigh has over 30 years’ experience within Financial markets across Fixed Income, Foreign-Exchange, Derivatives and Commodities. He has a background in Structuring, Product development and sales. Explaining financial products in simple terms...

Expertise

Leigh Winton

Head of Portfolio Strategies

FIIG

Leigh has over 30 years’ experience within Financial markets across Fixed Income, Foreign-Exchange, Derivatives and Commodities. He has a background in Structuring, Product development and sales. Explaining financial products in simple terms...

Expertise

Comments

Comments

Sign In or Join Free to comment