Fear and panic will not see us through; reason and rationality will

Charlie Aitken

Aitken Investment Management

The last seven days have been historic times in markets. The eleven-year bull market that started on 9 March 2009 finally ended eleven years and two days later, amidst some of the most volatile conditions seen on exchanges around the world for many years.

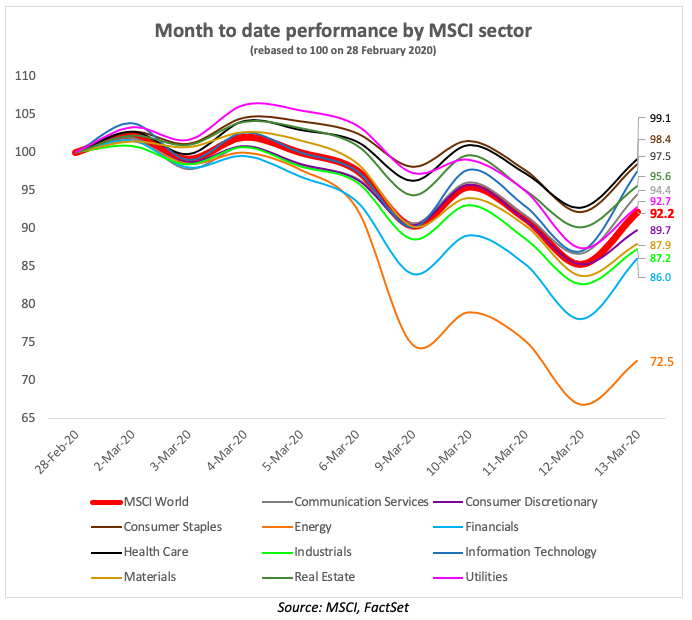

The move in global equity indices have been sudden, but they hide an even starker contrast when discerning between different sectors of the market. The chart below shows the performance of the MSCI World index in Australian dollars, as well as the underlying sector indices that comprise it, from the end of February to 13 March.

Recent Developments

The past week has been a perfect storm of bad news. The initial collapse in oil prices was keenly felt by stocks in the energy sector. However, given that many of these businesses – particularly US shale producers – have material quantities of debt, the market immediately became concerned about the possibility of default and the knock-on effect on banks… which, in turn, could have substantial impacts on the health of bank balance sheets and potentially the banking system.

Coupled with the rapidly worsening COVID-19 outbreak in many countries – revealing cases of substantial community spread in places such as Italy, Spain, France and the USA, among others – equity markets went into free-fall. While the selling has been widespread and brutal, there were some signs of discrimination emerging over the last days, with businesses that have strong balance sheets generally faring better.

Monetary support

On Wednesday, there was substantial strain in the plumbing of the financial system. Ongoing selling pressure – likely from a wide variety of leveraged investors, ETFs and other forced sellers – saw even the highly liquid US treasury market behave erratically on the day.

On Thursday, the Federal Reserve announced an injection of $1.5 trillion – spread over several days - to stabilise the US repo market. The ECB – after initially disappointing markets – also indicated they stand ready to step up their efforts to do the same. The RBA provided liquidity to the local repo market on Friday with an $8.8 billion injection, with the Bank of Japan taking similar actions.

This morning, the US Federal Reserve cut interest rates to zero, announced effectively $700 billion of quantitative easing, as well as combined actions with the central banks of Canada, England, Europe, Japan and Switzerland to increase US dollar liquidity around the world. We expect more monetary support in the next days and weeks, whether in the form of rate cuts or further QE.

To be clear, the governors and chairs of central banks around the world realise that monetary stimulus cannot fix the problem we currently face. They are merely buying time for the coordinated healthcare and fiscal response to address the public health crisis and the fundamental economic disruption fighting COVID-19 will cause. The last thing the world can afford at present is a financial crisis on top of the supply (oil oversupply combined with a supply chain disruption) and demand (consumer spending dropping as a result of enforcing social distancing policies) shocks already building.

Locally, we expect the RBA will likely cut interest rates to 25 basis points soon. With their stated position of not wanting central bank rates to enter negative territory, the only tool left will be quantitative easing. We struggle to see the Australian dollar strengthening against this backdrop.

Fiscal support

From a fiscal standpoint, the US House of Representatives and the White House has agreed in principal on a bill to support small businesses and workers impacted by the virus; markets believe this will be ratified by the Senate soon.

Germany has – finally, some might say – committed to spend materially to combat the effects of coronavirus. Given the strict balanced budget policy followed in Germany, this is a material development. In the UK, the government announced a series of targeted measures totalling to £30 billion to support the economy and healthcare system.

Locally, the Australian government has also announced a $17.6 billion package to support the economy. The wisdom of ‘going hard, going early and going to households’ remains front of mind, and rightly so, given the dimension of the demand shock we face.

Outlook

At a bare minimum, growth numbers across the board need to come down, and substantially so. Whether the world avoids a recession in 2020 is largely dependent on how long the disruption caused by COVID-19 lasts. It is virtually impossible to determine this with any certainty, but the current thinking is that the worst of the outbreak should be under control towards the third quarter of the year.

Expect a substantial drop in demand over the remainder of the first quarter and most of the second quarter of 2020. Given the complexity of the global economy and all the moving parts at play, trying to quantify this is very close to pure speculation. The amount of assumptions one is required to make means forecasting anything but the broadest range of outcomes is likely an exercise in false precision.

Instead, it may be better to invert the problem: not focusing on how bad things can get but rather trying to understand how bad things can be for a business before they run into distress. This means focusing on balance sheet quality.

To be clear, there are many fuzzy definitions of quality in investment. I take a fairly simple view of the issue: is the business in a sound balance sheet position? Does it have surplus cash and the ability to withstand a shock to its income for a reasonable period of time? If not, what is the debt level, maturity profile and ability to flex its cash outflows to cover any fixed payments?

The vast amount of above-average pain felt in equity markets over the last week have been in businesses with stretched balance sheets. Spreads demanded in credit markets have widened, meaning businesses forced to refinance will have to do so at higher rates – a problem in an environment with demand declining rapidly. In addition, the build-up of low quality ‘investment grade’ debt on corporate balance sheets over the last decade means these businesses are very exposed to potential default on their credit.

Practically, this means that the bond market may end up dictating the direction of equity markets for the foreseeable future.

A conservatively financed business is in a much better position to come out of this disruption relatively unscathed. In business – as in investing – the trick is to ensure you don’t get knocked out of the game before an upturn in economic conditions. Leverage is ultimately a magnifier, but it works both ways, and excessive leverage during the disruption we now face can be ruinous.

Portfolio construction considerations

One may be tempted to aggressively reposition a portfolio knowing that growth expectations need to come down, but I don’t think the answer is quite as simple.

Firstly, long-term investors own part share of a business with a view on their ability to grow and compound over a multi-year horizon. Near-term growth in revenues, profits and cash flow will be materially below initial forecasts – and as explained above, the actual quantum is virtually impossible to estimate with a high degree of certainty right now. My approach is therefore not to try and guess about the impact on earnings growth for the next two or three quarters and hope to avoid proverbial land mines. Chasing ‘outbreak-proof’ stocks – if there is such a thing – is taking a very short-term view.

I operate from the assumption that the impact on growth and cash flows will be contained to 2020 – or in a worst case scenario, some part of 2021 – and that all of our investments will find their long term operating environment, competitive advantage and growth drivers mostly unchanged.

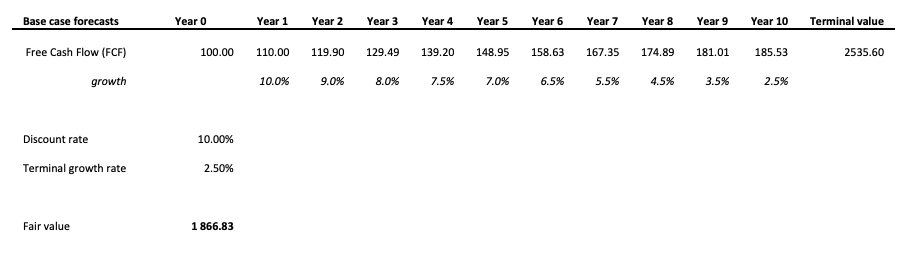

Consider the illustrative discounted cash flow valuations below:

In the simplified example above, the stream of cash flows grows fairly robustly over the first five years, fading to the long-term growth rate by year ten. A terminal value beyond year ten is calculated by capitalising the forecast year eleven cash flow, and then all these cash flows are discounted to a present value using a discount rate of 10%.

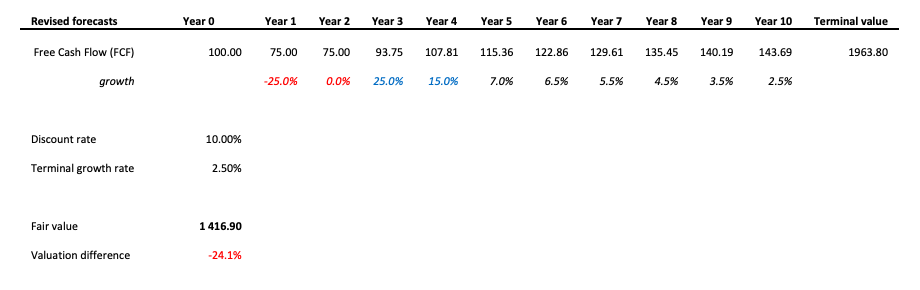

In the second example, the growth in years one and two are materially reduced, followed by a strong rebound in years three and four, and a return to historical growth rates thereafter. This has a substantial impact on the valuation – roughly 24% lower than the initial forecast in this example. However, given that markets have already seen a material sell-off, further weakness will at some point mean investors are being compensated to add to risk assets, although the appropriate level will vary on a company by company basis.

Combined with very accommodative monetary and fiscal policy settings we will have when exiting this period, I believe patient investors will be rewarded.

The above examples illustrate why I believe the focus on balance sheets right now are of paramount importance. High-quality businesses will ultimately come out the other end and the world will continue turning, but having the financial strength to endure the disruption that is coming will be key.

As a practical example, consider Apple. There is no doubt that Apple will see substantially reduced sales in China for the current calendar quarter, and lower than initially anticipated sales for the rest of the year. Apple announced in the last week that all its retail stores in China have re-opened, though they are seeing activity ramp only slowly. Over the weekend, Apple announced that it is closing all its retail stores outside of China for the next two weeks, meaning there is going to be a reduction in sales outside of China as well. Online sales will also slow as consumers prefer to delay purchases of higher ticket items.

The disruption to Apple’s supply chain was material, but the capacity is slowly ramping back up to normal levels. Chinese authorities are being very cautious about the pace of normalisation of their economy to avoid secondary outbreaks of the virus – a prudent decision.

However, with COVID-19 likely to cause consumer spending in other economies to materially deteriorate over the short term, Apple is faced with a supply chain that can again manufacture devices for consumers who are at present not inclined to purchase said devices. All around, it’s a very ugly situation, as this will impact Apple and its suppliers, plus employees at all levels.

However, I believe that:

a) Apple has the balance sheet to weather this disruption, given that the company has nearly $100 billion of net cash on its balance sheet;

b) when all this is past us, people will still be using their smartphones and other connected devices, and will ultimately need to replace them; and

c) the Apple ecosystem and brand remains incredibly powerful to its loyal customer base. Using these assumptions, I do not believe Apple will see its competitive advantage materially impaired over the long term.

Visa and MasterCard are two other stocks that are currently seeing reduced cross-border card payment volumes due to the drop-off in global travel. On the other hand, people staying at or working from home and requiring some form of online payment for delivery will ultimately accelerate the shift from physical cash to card-based payments for many. Even in physical retail settings, the desire to avoid cash (which is a potential vector for infection) may see increased card adoption going forward.

To us, these are the two key questions to ask about every stock: does it have the balance sheet to survive the disruption, and will it still have the same competitive position that made the businesses an attractive cash flow generator in the first place? If the answer is yes to both, then selling in a panic after a substantial market drop is the wrong choice.

This is why I don’t believe drastically reshaping equity portfolios at present is the wisest thing, given that valuations have already adjusted downwards. Markets will continue to be very volatile, but businesses with high quality balance sheets will be able to weather the storm.

A final word

While all our commentary above has been written from the perspective of a market participant, it is worth stepping back and reminding ourselves there is a real human cost to all the current turmoil as well.

While governments and monetary authorities are beginning to mount their response to the issues before us, there can be no doubt that the next few weeks or months will be difficult. Friends or family may become ill. Many will feel the all-too-real threat of economic hardship while the crisis is managed within our own borders and abroad. We extend our sympathies to anyone impacted.

The world has never faced a challenge quite like the one we are dealing with now. Front-line healthcare workers are doing heroic work to save lives, and things will likely get worse before they get better. However, I believe humans are incredibly adaptive and resilient, and here in Australia we have always faced challenges with a spirit of optimism, camaraderie and hard work. Fear and panic will not see us through; reason, rationality – and in this case, good hygiene – will.

What we are facing now shall pass, in time. Until then, I wish you and your families good health and prosperity.

Invest with conviction

Aitken Investment Management is an independent global fund manager that aims to capture long-term secular trends by investing in high quality businesses that can compound in value.

To find out more hit the 'CONTACT' button below.

Never miss an update

Enjoy this wire? Hit the ‘like’ button to let us know.

Stay up to date with my current content by

following me below and you’ll be notified every time I post a wire

4 topics

Charlie Aitken

Aitken Investment Management

Expertise

Charlie Aitken

Aitken Investment Management

Expertise

Comments

Comments

Sign In or Join Free to comment