Finding hidden value in intangibles

Charlie Aitken

Aitken Investment Management

2020 has already given investors much to mull over: a (now nearly forgotten) Middle Eastern geo-political scare in the first days of January, the normal ebb-and-flow of reporting season, and the truly out of the blue risk the coronavirus outbreak has introduced to growth assumptions for 2020.

Other than to observe that markets have been fairly resilient in the face of COVID-19 – given a viral outbreak may not respond as readily to central bank stimulus – I don’t believe there is much value in speculating about the near-term trajectory of how a situation this fluid is ultimately resolved. Medical professionals and public health officials the world over are mounting a gargantuan effort to save lives and contain the spread of the virus. To burden them with also satisfying markets’ lofty expectations is a bridge too far.

Instead, I thought it may be worth touching on a topic that speaks to a trend playing out in corporate balance sheets over the last 20-odd years: the increasing investment in intangible assets, and the resulting impact this has on how value is created and what it might mean from a fundamental valuation perspective.

Changing Tides

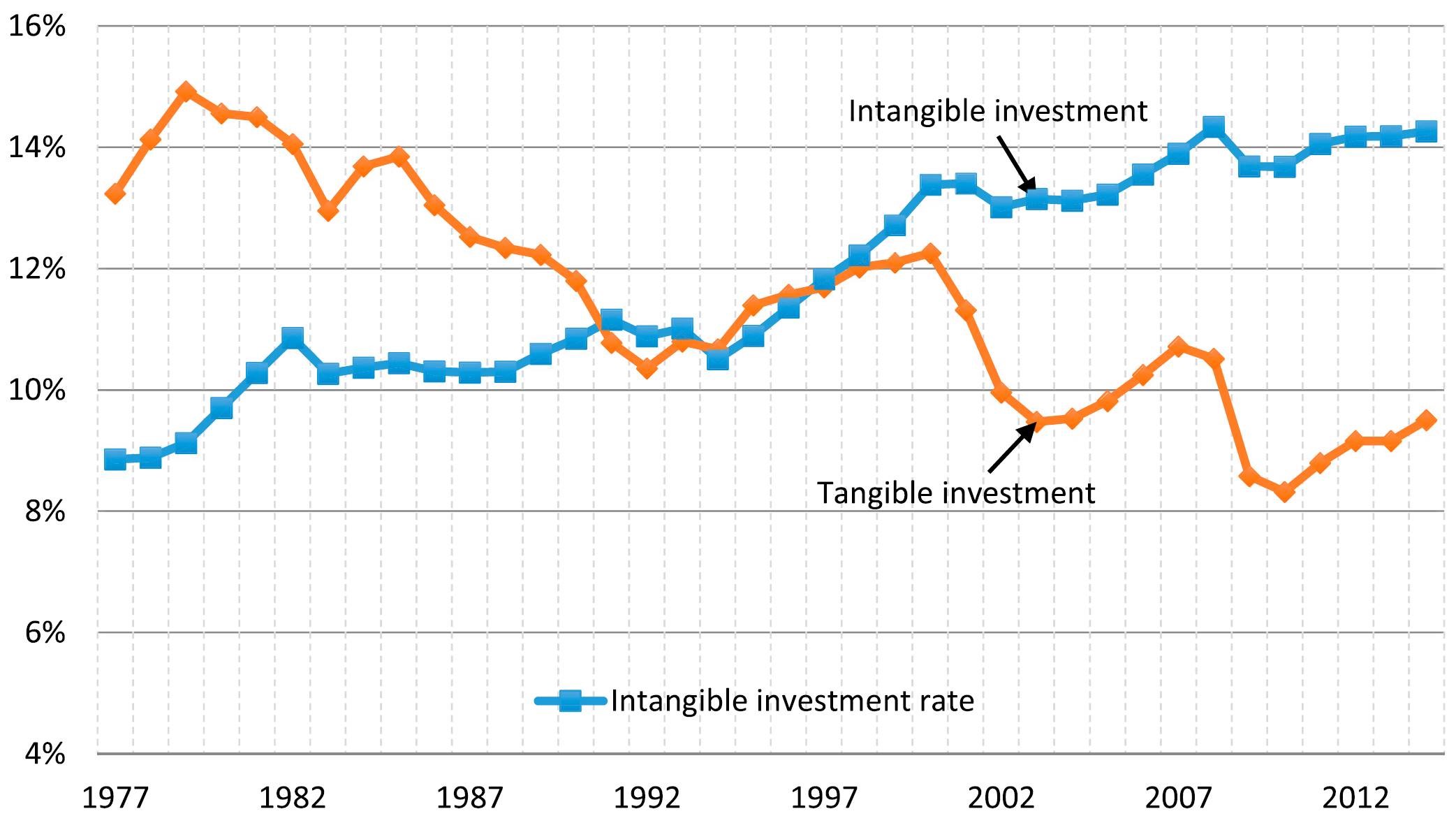

Since the late 1990’s, US private sector investment in intangible assets (such as research and development, brands or businesses processes) has overtaken the investment in tangible assets by quite some margin.1,2

Figure 1: US Private Sector Investment in tangible and intangible capital, 1977 – 2014. Source: Lev, B; Corrado, C; Hulten, C.

This has led to a fairly profound change in how economic value is created. Physical assets (with rare exceptions) are no longer sufficient drivers of differentiation to enable a firm to generate a sustainable competitive advantage. Stores, corporate headquarters, factories, machines, trucks – almost all of these can be bought or leased. There may be substantial start-up capital required, but tangible assets are increasingly commoditised.

Conversely, the amount spent on intangible assets increasingly underpin the moats sought after by investors looking to own companies that can sustainably generate superior cash flow returns on invested capital.

Consider the advertising spend of LVMH to preserve and grow the Louis Vuitton brand, or the ongoing research and development by Alphabet to consistently improve the Google search engine: all these costs are expensed through the income statement (having the immediate impact of lowering profitability), and show up on no balance sheet as an asset (lowering the invested capital base and understating the book value of equity). Yet, given that the benefits of such expenses are likely to be derived over a period of years, it stands to reason that the accounting approach of expensing the full amount in the year it is incurred does not give investors the full picture: should these items not b e seen as assets, equal to its tangible brethren?

The Reasons Behind the Accounting Approach

The reason for expensing most of the spending on intangible assets is grounded in a fundamentally sound point of view: intangible assets generated internally by a business are difficult to measure and value, and therefore fail to meet the criteria for recognition as an asset on the balance sheet. (There are some differences to how this is treated across different international accounting standards).

Ironically, acquired intangibles can show up on the acquirers’ balance sheet, precisely because a value was placed on the asset by third parties during the (arms’ length) acquisition transaction. These different accounting treatments create a contradiction, as NYU Stern School of Business Professor Baruch Lev and University of Buffalo Professor Feng Gu point out:3

What’s the difference between acquiring intangibles directly from other companies (capitalised) or acquiring the services of third parties to develop intangibles (expensed)? There is none, of course. In each case, the company transacts with third parties. Thus, the accounting contrast between internally generated versus acquired intangibles is a distinction without a difference. Both internally generated and acquired intangibles create risky assets, but being subject to risk doesn’t justify ignoring (i.e. expensing) these assets.

The point is that there is no material difference between an acquired intangible and an internally developed one, at least from an economic point of view. However, only the former shows up in financial statements, leading to the slightly odd outcome that a highly acquisitive company may end up looking cheaper on a Price/Book ratio than a company that manages to grow via only internally generated intangibles.

The Economic Difference Between Tangible and Intangible Assets

Acknowledging that intangibles are treated differently from an accounting point of view, it’s also worth considering the difference in how these assets are actually utilised in business.

Intangible assets are unique in that they exhibit certain economic properties to a greater degree than tangible assets.4 Relevant for investors is the trait of ‘scalability’: the idea that an intangible asset (such as a brand or piece of software) can be used in multiple places simultaneously and repeatedly. Indeed, much of the success of many large businesses are built on this exact concept – yet it is virtually absent from the financial accounts. This also creates issues with comparability between companies and across industries when evaluating investment opportunities.

Intangibles are without a doubt difficult to value. In addition to scalability (which is a positive), intangibles also exhibit other, riskier characteristics in greater degrees4: the fact that certain types of intangibles can be reverse-engineered or easily copied, or the concept that certain types of intangible investment represent a sunk cost that can only be valuable in specific contexts. As such, any attempt to place a value on an intangible asset should be simple, specific and (above all) conservative, lest it leads to a cycle of creating value out of thin air based on a layer of assumptions and estimates.

None less than NYU Stern School of Business Professor Aswath Damodaran – essentially the rockstar of valuations – has been preaching for many years that identifiable expenses on internally generated intangible assets that will create value over a longer period of time than the current year should be capitalised and amortised like any other asset.5 This process involves adding back some component of historical and current investment (previously expensed) in intangible assets, then amortising them over an estimated useful life that reflects their economic reality. To remain consistent, any historical non-cash adjustments to intangibles assets – such as a goodwill impairment – should also be added back to the capital base. (If management have made a poor capital allocation decision in the past and impaired it, an investor would certainly want to know about it since it will inform their view on management as stewards of capital going forward).

This approach seeks not to place a market value on an intangible asset – it merely seeks to measure the historical spending (which is factual and quantifiable) and track whether the business is generating an adequate return on this investment.

Making these adjustments has the effect of increasing both the earnings and book value (i.e. equity) of the firm. The purpose of the adjustments is not to inflate earnings. It is to more clearly reflect the economic return of the historic investment in intangibles.

So What?

Financial accounts have many different users, of which investors are only one constituency. Just as providers of credit make certain adjustments to appropriately determine the cost of debt funding, it makes sense for equity investors to do the same to arrive at a set of accounts that reflect the economic reality of a business. In adjusting the reported accounts, I believe one can calculate a ‘cleaner’ version of the cash flow return on invested capital, leading to a much-improved method for comparing returns across various industries. Evaluating growth without taking into account the investment required to generate that growth is overlooking a key component in the economic value creation process.

In addition, it’s worth noting that by having intangible assets not appear on balance sheets, reported Price/Book ratios for companies (mainly software, internet platform and brand driven consumer-facing businesses) that are heavily reliant on intangible assets to underpin their sustainable competitive advantage do not readily reflect whether they are cheap or expensive.

Notes

- Lev, B. (2018), The Deteriorating Usefulness of Financial Report Information and how to Reverse it. Accounting and Business Research. 48. 465-493. 10.1080/00014788.2018.1470138.

- Corrado, C., Hulten, C. and Sichel, D. (2009), Intangible Capital and US Economic Growth. Review of Income and Wealth, 55: 661-685. doi:10.1111/j.1475-4991.2009.00343.x

- Lev, B., Gu, F. (2016), The End of Accounting and the Path Forward for Investors and Managers. Wiley.

- Haskel, J., Westlake, S. (2018), Capitalism without Capital. Princeton University Press.

- Damodaran, A. Invisible Value? Valuing Companies with Intangible Assets (2009). New York University.

Invest with conviction

Aitken Investment Management is an independent global fund manager that aims to capture long-term secular trends by investing in high quality businesses that can compound in value.

To find out more hit the 'CONTACT' button below.

Never miss an update

Enjoy this wire? Hit the ‘like’ button to let us know.

Stay up to date with my current content by

following me below and you’ll be notified every time I post a wire