Finding value in Australian markets

The past month has delivered little resolution to the key questions plaguing investors as the cycle matures. Can strong global growth be sustained beyond this year, and inflation and wage pressures stay benign, allowing risk markets to grind ever higher? Alternatively, will tightening jobs markets foster an unexpected lift in inflation, or will global growth fail under the weight of a persistent trade war and other geo-political risks?

Despite the ebb and the flow of largely ‘Trump-centric’ trade war headlines, and a new financial crisis in Turkey that seemed to dissipate as fast as it emerged, risk markets have continued to move higher through August. Our decision to shift tactically overweight US equities at the start of July (staying overweight in Europe) has added value. Geo-political risk and benign inflation globally have also continued to keep fixed income markets rangebound.

We have made no changes to our tactical positioning this month, continuing to favour equities over bonds. And within a neutral equities position, we continue to favour US and European equities over Australia (a position that’s benefitted from the Australian dollar’s recent weakness). We continue to monitor developments and increase allocations to alternative uncorrelated assets, cognisant that there is a fragile element to the outlook, which highlights the importance of maintaining an appropriate asset allocation.

Over recent months, we’ve spent some time focusing on global opportunities. This month, we take our focus back to Australia, a core holding in portfolios. We take a look at the pulse of growth and the risks to the outlook for both the economy and markets. We also share first impressions around the impact of the recent political upheaval and the equities reporting season themes.

Australia’s economy continues to expand at a robust pace

At his Parliamentary Testimony earlier this month, Reserve Bank of Australia (RBA) Governor, Dr Philip Lowe, noted that

“the Australian economy has continued to move in the right direction…the economy looks to have grown strongly over the first half of 2018”.

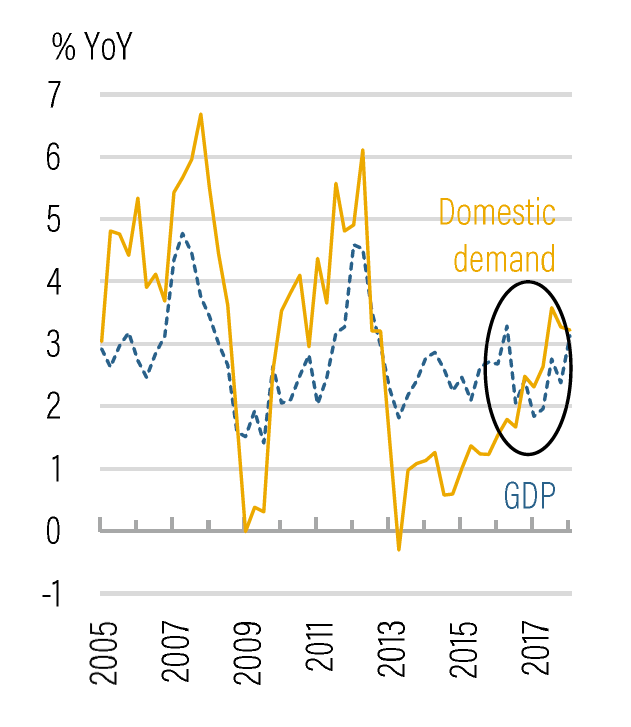

Indeed, Q1 growth in Australia accelerated from last year’s average pace of 2.2% to 3.1% (around its historic trend), and estimates for Q2 growth, due in the first week of September, have been edging higher and are centred on another solid quarterly result near 3%. Despite the negative commentary that often surrounds Australia’s outlook, recent data continue to point to relatively robust growth ahead:

Business conditions remain at relatively high levels, with signs of a pick-up in the previously weak states of Queensland and Western Australia.

Retail sales have beaten expectations for the past several months, with annual growth recovering from 2% to a still relatively moderate 3%.

Export growth has risen almost 5% (by volume) over the past year, helped by synchronised global growth and China’s search for cleaner commodities.

Jobs growth remains very strong at 2.4% (albeit slower than in 2017). This is the equivalent to 342,000 new jobs over the past year.

Public investment remains a key support to growth as governments engage in significant rail and road projects on the east coast.

Australian growth outlook looks robust

Source: Crestone, Austrlian Bureau of Statistics

Of course, Australia also faces a number of headwinds that are likely to constrain growth to around this 3% trend pace. This is in contrast to the above-trend growth rates seen in the US, Japan and Europe:

China growth is slowing which, given it consumes over one-third of Australia’s exports, could present a growth headwind.

Housing activity, while still elevated, is ‘ex-growth’ and unlikely to contribute the same impulse to activity over the coming couple of years.

A drought could directly reduce growth, given much of the east coast is experiencing severe rainfall deficiency.

Credit growth is being constrained mostly to investors, as regulators focus on improving lending standards and system-wide credit risks.

Credit growth is slowing, led by investors

Source: Crestone, Reserve Bank of Australia

Where can we find value in Australian markets?

Australian fixed income markets remain attractive

We remain overweight Australian relative to global fixed income (at 1% underweight versus 4% underweight globally). Markets continue to expect further near-term interest rate increases in the US. Interest rates are also expected to rise through 2019 in Europe and Japan, as global quantitative easing (QE) begins to unwind. In contrast, given ‘at-trend’ growth, a slowing housing and credit cycle, and inflation below the RBA’s target, expectations for any upward hike in Australian rates is focused on late 2019 or even 2020.

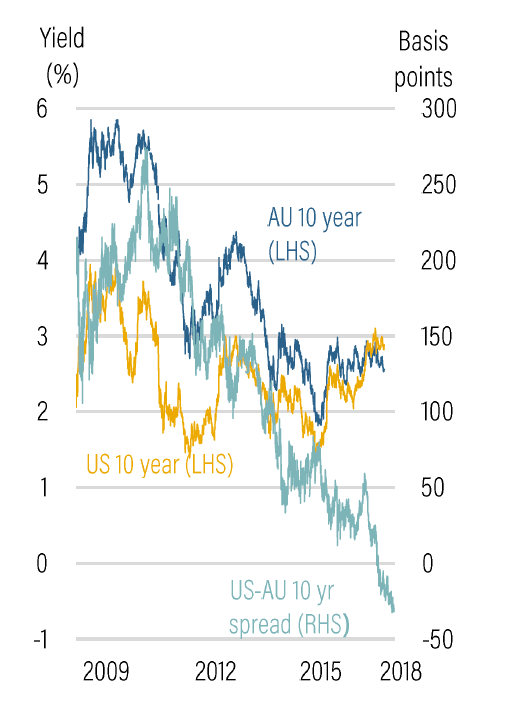

For Australian government bonds, yields are likely to trend higher from here as the global outlook remains favourable and global central banks normalise policy. However, we expect any increase to be more muted than globally. Indeed, Australian 10-year yields have recently traded well below those of the US (see chart below), a trend we expect can continue (and intensify).

For Australian corporate debt, we remain supportive of investment grade, where demand is driven by attractive real yields and strong issuer credit relative to global alternatives. While funding pressures for Australian banks saw senior unsecured spreads widen earlier in the year, the recent rally in bond yields has led to a stabilisation in spreads.

Fixed income markets remain attractive

Source: Crestone, Factset

Australian equity markets remain a modest underweight

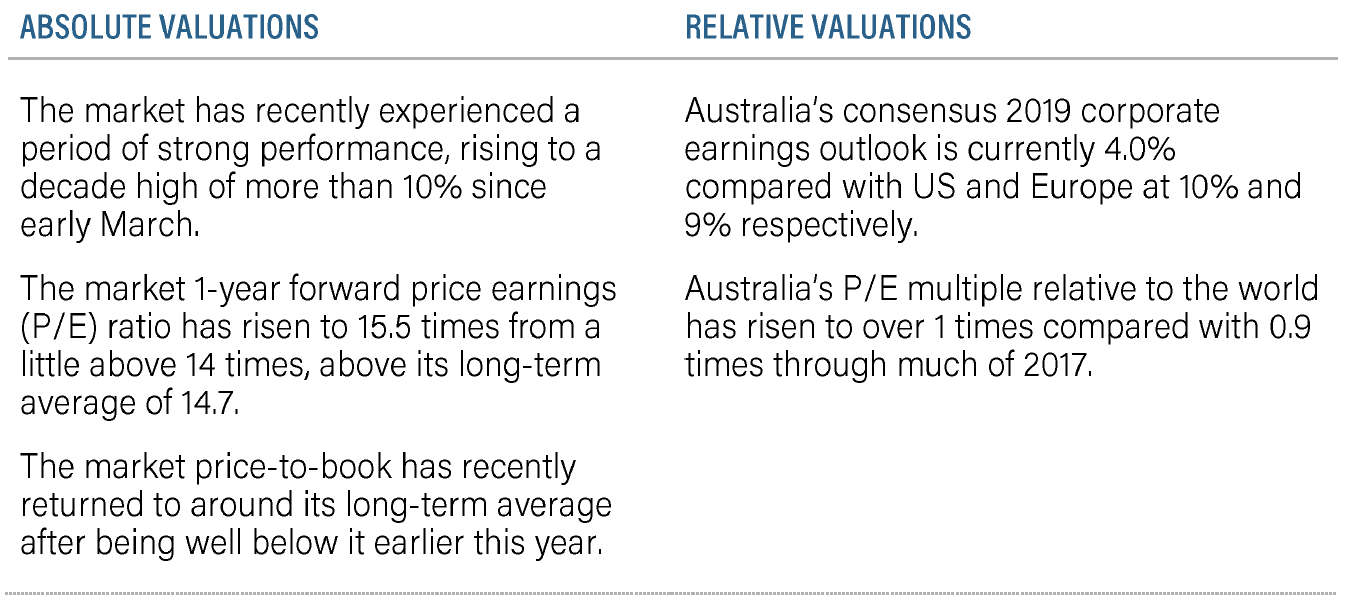

We are not bearish domestic equities. But as we wrote a few months ago, we continue to view international equity markets as warranting a relative overweight. This is in part due to their higher sector weightings in structurally faster-growing sectors, and in part due to expected above-average economic growth. Our end-year target for the Australian dollar of USD 0.72 also supports our preference for unhedged international equity positions, though less so than earlier in the year when the exchange rate was over USD 0.80. Reflecting UBS research, we note the following concerning domestic equities:

Looking at Australia’s recent equity reporting season

The reporting season in Australia looks to have mirrored many aspects of the recent US Q2 reporting season with ‘in-line’ results the norm. More than half of companies produced results that were in keeping with consensus, while ‘beats’ versus ‘misses’ were relatively evenly split. Nonetheless, as always, there were some key trends that are worth noting:

• While 2018 results were typically in line, FY19 guidance proved modestly weaker than expected. According to UBS, “negative FY19 earnings revisions outweighed positive revisions by around two to one”.

• For those companies that did deliver earnings upgrades, they were concentrated outside the top-100 in the S&P/ASX 300 index and driven by higher-than-expected cash flow (not cost out).

• Costs broadly surprised to the upside, suggesting the past few years of aggressive cost out has largely been exhausted. Companies exposed to rising raw material costs were particularly vulnerable.

• Capital management stayed a focus with more positive than negative dividend surprises and significant new on-market buy-backs and extensions of current plans announced.

Otherwise, tariffs and trade war concerns were of little focus. According to UBS, some of the industry-specific themes were around a partial recovery in mining exploration and strong east coast infrastructure that aided mining services and contractors. Additionally, lower electricity prices led to energy retailer downgrades. High quality offshore earners (notably in healthcare) outperformed domestically-exposed stocks. Finally, growth remained in favour, as the market was willing to pay up for high multiple stocks, while punishing premium stocks that missed earnings or guidance.

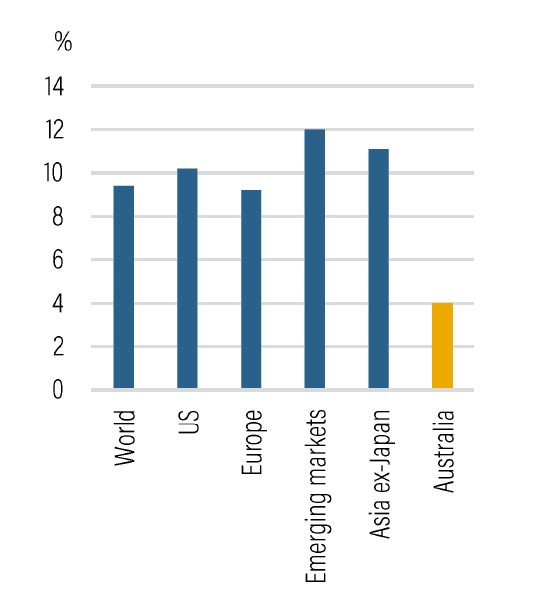

Consensus earnings growth for calendar year 2019

Source: UBS

We continue to favour a number of themes

Looking ahead, with the broader ASX industrials (ex-financials) trading just shy of 22 times forward P/E, higher than the pre-GFC peak, style and sector selection is becoming increasingly important. We favour themes, such as:

1. seeking value in domestic companies with exposure to offshore high-growth markets;

2. being cognisant of the market’s high level of dispersion towards growth and the risk that, at some point, there may be a rotation back to more valueorientated companies; and

3. consistent with the above, investing cautiously in sectors that appear crowded.

Are political risks rising in Australia?

Australia’s ruling Coalition experienced another leadership tussle in August, with the sitting prime minister (PM), Malcolm Turnbull, challenged for the leadership by immigration minister Peter Dutton. This was unsuccessful, with the former treasurer, Scott Morrison, winning the ballot to be the new PM.

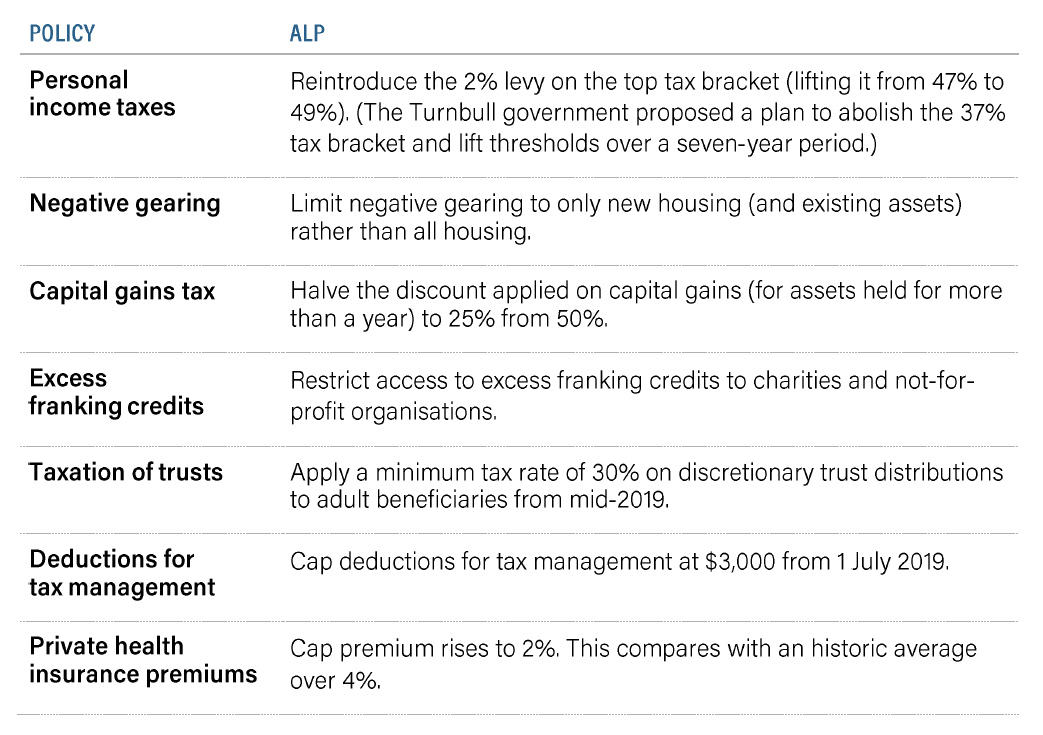

Given the Coalition was already trailing in the opinion polls, the chaos in recent weeks has further damaged their re-election prospects. Although the next federal election is not due for a considerable period of time (on or before 18 May 2019), it is worth highlighting the key policy differences of the Australian Labor Party (ALP) if there were to be a change in government. These are summarised in the table on the next page. New policies would need to pass the upper house (Senate) before becoming law, albeit the ALP would likely garner some support from the (leftleaning) Australian Greens.

Want to learn more?

Crestone Wealth Management provides wealth advice and portfolio management services to high-net-worth clients and family offices, not-for-profit organisations and financial institutions. Find out more

Never miss an update

Enjoy this wire? Hit the ‘like’ button to let us know.

Stay up to date with my current content by

following me below and you’ll be notified every time I post a wire

Scott has more than 20 years’ experience in global financial markets and investment banking, providing extensive economics research and investment strategy across equity and fixed income markets.

Scott has more than 20 years’ experience in global financial markets and investment banking, providing extensive economics research and investment strategy across equity and fixed income markets.

Expertise

Scott has more than 20 years’ experience in global financial markets and investment banking, providing extensive economics research and investment strategy across equity and fixed income markets.

Expertise

Comments

Comments

Sign In or Join Free to comment

most popular

Investment Theme

If 24 LICs ran the Melbourne Cup, which ones would we back?

Affluence Funds Management