Five reasons to consider BlueSky for the portfolio

Blue Sky has just announced a 130% increase in 1H17 NPAT to $10.1m, and a 59% growth in assets under management to $2.7bn over the pcp. This impressive result has been driven by Blue Sky’s unique asset class offerings that include Private Equity, Real Assets (largely water rights and agriculture), Private Real Estate, and Hedge Funds. Importantly, this momentum is forecast to continue with full-year company guidance of an FY17 underlying NPAT of $24-26m and AUM of $3.1-3.3bn. Since listing in 2012, Blue Sky has established an enviable history of regularly beating market expectations. Not surprisingly, investors have been well rewarded with a share price that has risen 100% in the past two years. However, we suggest there is plenty more upside for this business and highlight five reasons why Blue Sky should be seriously considered as a core portfolio investment.

1. Globally proven industry tailwinds – Australian investors (both institutional and retail) have been reluctant to venture far from the ‘traditional’ asset classes of listed equity, bonds, cash and property. However as returns in these assets have become increasingly squeezed due, in the most part, to depressed interest rates, those looking to generate alpha have had no choice but to look ‘outside the box’ to alternative assets. As such, domestic allocations to alternative assets have tripled to around 17% in the past decade, yet this is still well below global allocations of 24%.

2. Impressive track-record – Both at a corporate level and fund level, BLA has provided outstanding results for its clients and shareholders. BLA’s average annual return across its stable of managed funds is in excess of 16% p.a.; the performance of the listed fund (BAF.ASX) is up over 9% p.a.; and the head stock (BLA.ASX) has risen more than 50% p.a. since listing.

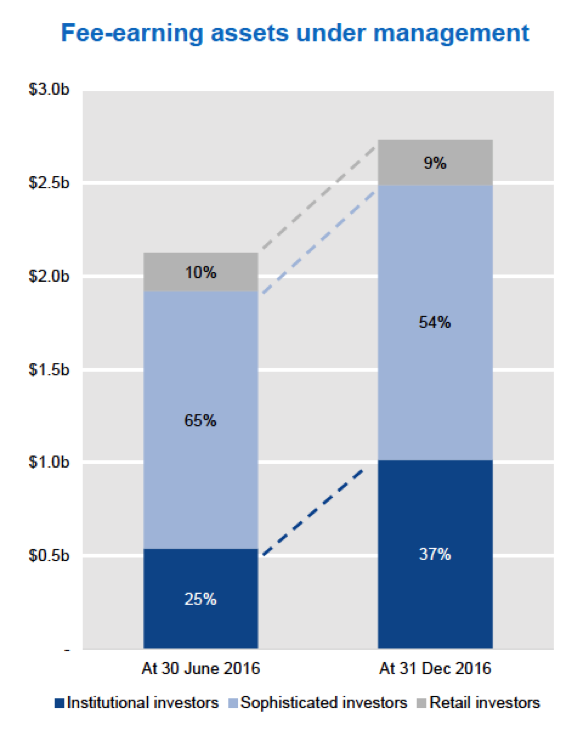

3. Institutional growth – 2016 marked the first year in which BLA made meaningful inroads into the substantial institutional market, winning almost $800m in institutional mandates. It is not unreasonable to expect this trend will continue, significantly accelerating BLA’s overall AUM.

4. Financial transparency – A major attraction of any funds management business is the relative ease in which to predict their financial outcomes. With relatively straightforward management and performance fee models, stable staffing trajectories and, in BLA’s case, a high proportion (80%) of closed-end AUM, earnings predictability can be considered high.

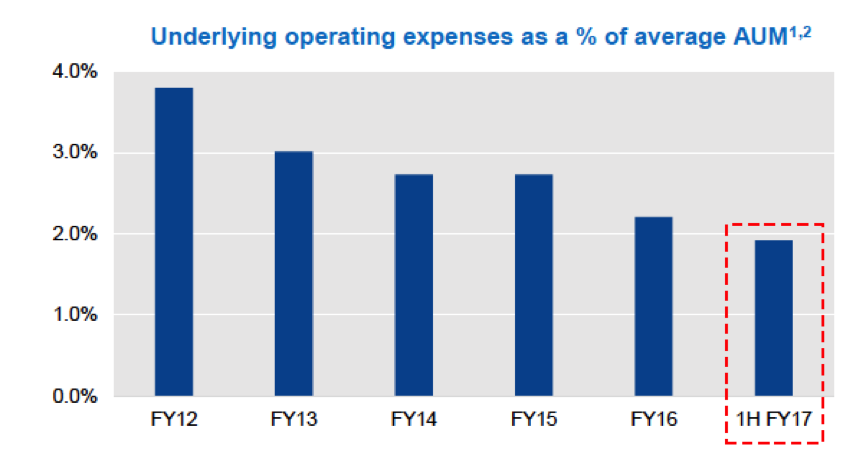

5. Business scalability – last, but certainly not least, is the enormous scalability of any growing funds management business. BLA has, in a global sense, a miniscule level of FUM; Blackstone, for example, has over $250bn of AUM. Despite the modest level of AUM to date, BLA’s operating expense (as a % of AUM) has still managed to decline every year. As BLA’s AUM grows, shareholders can reasonably expect that a growing proportion of these revenues will flow through to company profits and dividends.

Never miss an update

Enjoy this wire? Hit the ‘like’ button to let us know.

Stay up to date with my current content by

following me below and you’ll be notified every time I post a wire

Dean has over 25 years experience in the funds management industry covering all major asset classes. He holds as Master of Applied Finance and is a Graduate of the Australian Institute of Company Directors.

2 topics

1 stock mentioned

Dean has over 25 years experience in the funds management industry covering all major asset classes. He holds as Master of Applied Finance and is a Graduate of the Australian Institute of Company Directors.

Expertise

Dean has over 25 years experience in the funds management industry covering all major asset classes. He holds as Master of Applied Finance and is a Graduate of the Australian Institute of Company Directors.

Expertise

Comments

Comments

Sign In or Join Free to comment